Loading Market Data

Real prices, in two lines. Pull US stocks with yfinance and read a CSV, then look before you leap with head() and info().

- ·Reading a CSV

- ·Fetching with yfinance

- ·head, tail, info

- ·describe()

- ·Setting an index

- ·Saving to CSV

You know what a DataFrame is and what to do with one. The obvious next question: where do they come from? In practice, two places - a live download (we've been using yfinance) and a file on disk, almost always a CSV. Loading data is the very first line of every analysis, so this short, practical chapter makes sure you can always get a table in - and save one back out - whatever the source.

Fetching with yfinance, and saving a CSV

You've already fetched data with yfinance; here we add the other half - writing it to a CSV so you never have to download it again. We'll use an Indian stock this time:

import yfinance as yf

# ".NS" is Yahoo Finance's suffix for NSE-listed Indian stocks.

df = yf.Ticker("RELIANCE.NS").history(period="6mo")[["Open", "High", "Low", "Close", "Volume"]]

df = df.round(2).dropna() # drop incomplete rows (Yahoo leaves today's bar empty)

df.index = df.index.date

df.index.name = "Date"

# Save the whole table to a CSV file - just one line.

df.to_csv("reliance_6mo.csv")

print("Saved", len(df), "rows to reliance_6mo.csv")

print(df.tail(3))Saved 124 rows to reliance_6mo.csv

Open High Low Close Volume

Date

2026-06-22 1316.7 1344.9 1314.1 1326.5 12931213

2026-06-23 1328.9 1333.0 1304.0 1309.5 15400184

2026-06-24 1305.7 1322.0 1297.5 1313.6 11030917Two India-specific notes. First, Yahoo's code for an NSE stock is the symbol plus .NS (so RELIANCE.NS) - we'll map symbols across sources properly in Chapter 34. Second, .dropna(): Yahoo often leaves the current day's bar empty until the close, so we drop incomplete rows - a small but important habit with Indian data, and the heart of the next chapter. Then df.to_csv("reliance_6mo.csv") writes the whole table to disk in one line.

Reading a CSV back

To load that file - or any CSV someone hands you - use pd.read_csv. Two arguments earn their keep with time-series data:

import pandas as pd

# Read the CSV back into a DataFrame, using the Date column as the index.

df = pd.read_csv("reliance_6mo.csv", index_col="Date", parse_dates=True)

print("Shape :", df.shape)

print("Columns :", list(df.columns))

print()

print("Most recent rows:")

print(df.tail(3))

print()

print("Close-price summary:")

print(df["Close"].describe().round(2))Shape : (124, 5)

Columns : ['Open', 'High', 'Low', 'Close', 'Volume']

Most recent rows:

Open High Low Close Volume

Date

2026-06-22 1316.7 1344.9 1314.1 1326.5 12931213

2026-06-23 1328.9 1333.0 1304.0 1309.5 15400184

2026-06-24 1305.7 1322.0 1297.5 1313.6 11030917

Close-price summary:

count 124.00

mean 1388.35

std 69.07

min 1258.80

25% 1338.58

50% 1384.30

75% 1428.84

max 1584.97

Name: Close, dtype: float64index_col="Date" tells pandas to use the Date column as the row index (instead of a plain 0,1,2 counter), and parse_dates=True turns those date strings into real datetime objects you can do time maths on. With those two, your loaded table behaves exactly like a freshly downloaded one.

df.to_csv("file.csv") saves a table to disk; pd.read_csv("file.csv") loads it back. For time series, pass index_col="Date" and parse_dates=True so the dates become a proper datetime index.

describe(): the thirty-second X-ray

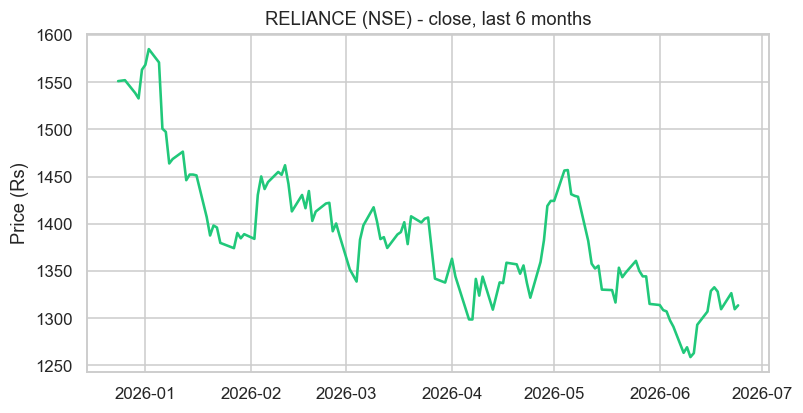

Notice the last line of that example: df["Close"].describe(). It returns a whole statistical summary at once - count, mean, standard deviation, min, max, and the quartiles. For our Reliance data it instantly reveals the six-month range (a low near 1259, a high near 1585) and the typical level (~1388). Run describe() on any new dataset before anything else; it's the fastest way to understand what you're holding and to spot anything odd.

From file to chart

Once a CSV is saved, you never need the internet again - load and chart entirely offline:

from pathlib import Path

import matplotlib

matplotlib.use("Agg")

import matplotlib.pyplot as plt

import pandas as pd

import seaborn as sns

# Load straight from the CSV - no internet needed once it is saved.

df = pd.read_csv("reliance_6mo.csv", index_col="Date", parse_dates=True)

sns.set_theme(style="whitegrid")

fig, ax = plt.subplots(figsize=(8, 4))

ax.plot(df.index, df["Close"], color="#21c87a", lw=1.7)

ax.set_title("RELIANCE (NSE) - close, last 6 months")

ax.set_ylabel("Price (Rs)")

out = Path(__file__).with_suffix(".png")

plt.savefig(out, dpi=110, bbox_inches="tight")

print("Charted", len(df), "rows loaded from the CSV")Charted 124 rows loaded from the CSV

Load, then plot - the whole pipeline from a file to a finished chart of six months of Reliance, in a dozen lines. This load-analyse-visualise loop is the daily rhythm of working with market data.

The humble CSV is older than the personal computer. Comma-separated values date back to the early 1970s - they predate the PC, the spreadsheet, and pandas itself by decades, and weren't even formally standardised until 2005 (in a document called RFC 4180). Plain, unglamorous, and utterly universal, CSV has outlived countless flashier formats. When a fifty-year-old idea is still the default way the world swaps data, that's a feature, not an accident.

Try it yourself

- Download a US stock with

yf.Ticker("MSFT").history(period="1y"), save it withto_csv("msft.csv"), then read it back withread_csv. - Open your saved

reliance_6mo.csvin a plain text editor (or Excel). Confirm it really is just commas and numbers - nothing magic. - Run

df.describe()on the whole Reliance DataFrame (not just Close). Which column has the largest numbers, and why?

Recap

- Get a DataFrame from a download (yfinance) or a file (CSV) - the two everyday sources.

df.to_csv("file.csv")saves;pd.read_csv("file.csv")loads - addindex_col="Date"andparse_dates=Truefor time series.- For Indian stocks on Yahoo, use the

.NSsuffix and.dropna()to drop incomplete bars. describe()gives an instant statistical summary - run it on every new dataset first.

We've quietly slipped a .dropna() into the last two chapters without dwelling on it. That's because real data is messy - missing values, wrong types, duplicates - and cleaning it is half the job. The next chapter tackles that head-on: data cleaning, with the genuine quirks of the data you just downloaded.