Bearish Butterfly and Bearish Condor

Defined-risk ways to target a specific downside zone. Learn the bearish butterfly and bearish condor, all-put structures that pay the most if NIFTY drifts down to a chosen level.

- ·A targeted bearish view

- ·The bearish butterfly

- ·The bearish condor

- ·Cheap, high reward to risk

- ·Why the POP is low

- ·Reading the real payoffs

Every bearish trade so far has rewarded a fall, and the bigger the fall the better. This chapter teaches the opposite instinct. What if you do not merely think NIFTY will drop, but think it will drop to a particular place and stop, settling into a narrow band a little below where it sits now? When your view is that precise, you can buy a structure that costs almost nothing and pays many times its cost if the index lands exactly where you guessed. These are the bearish butterfly and the bearish condor, built entirely from puts, sitting just below the money. They are cheap, they are defined-risk, and they offer a dazzling reward against a tiny outlay. The honest catch, which this chapter will not hide, is that the odds of winning are low, because the price has to thread a needle.

The one-line idea

A bearish butterfly and a bearish condor are both range bets placed below the current spot. You assemble four put legs so the structure is worth almost nothing outside a narrow zone and worth a lot if NIFTY drifts down into it. You pay a tiny net debit to get in, and that debit is the most you can lose. The reward, several thousand rupees against a few hundred, looks spectacular, and the probability of collecting it is the part you must keep honest.

A bearish butterfly and condor are cheap, defined-risk bets that NIFTY will ease down to a specific level and stall there. The tiny debit you pay is your maximum loss, the payoff is many times that debit, and the probability of profit is only about one in ten. They are precise, low-odds tickets on a landing spot, not bets on a big move.

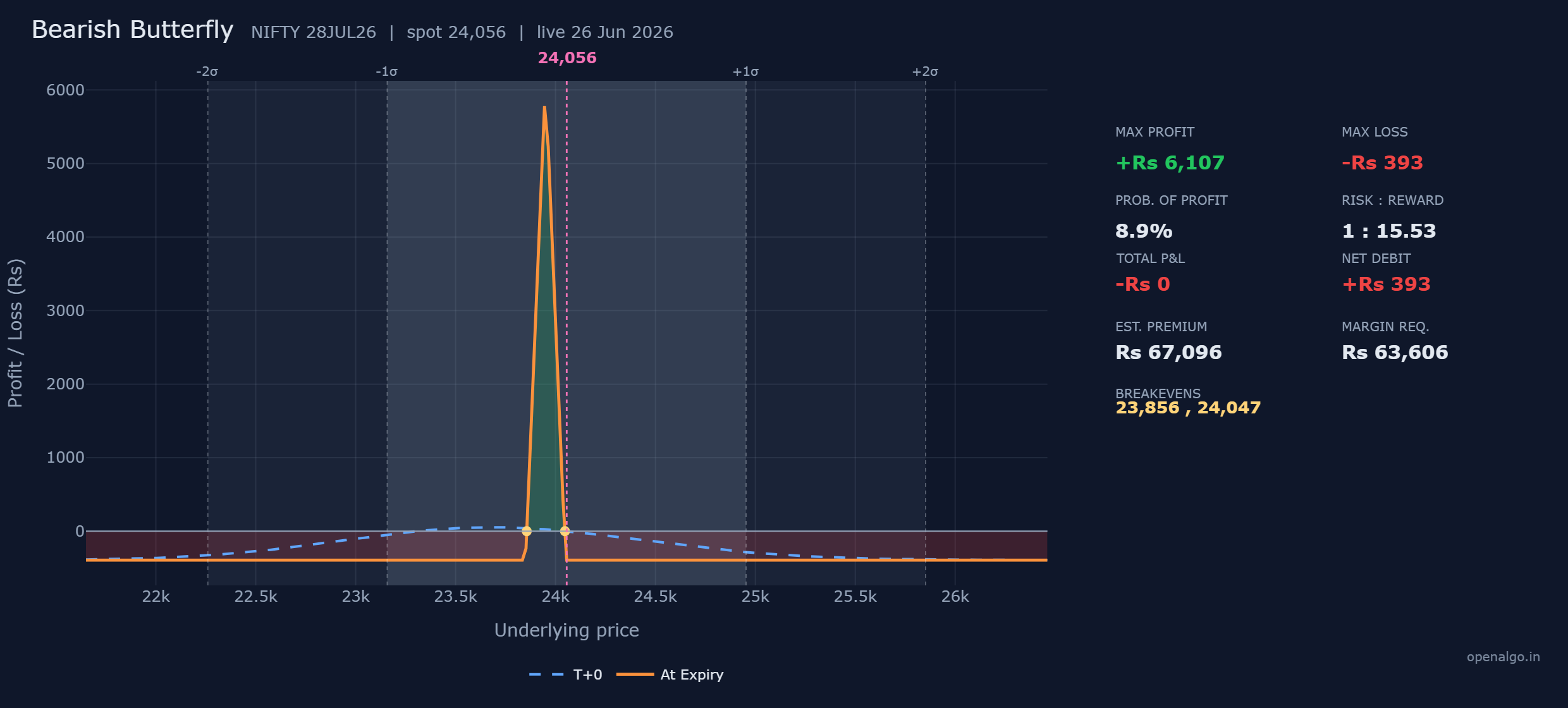

The bearish butterfly

A butterfly has three strikes and four legs. You buy one put above, sell two in the middle, and buy one below, so the two bought wings fence in the two sold puts at the body. Placed below the spot, the whole structure peaks if NIFTY drifts down to the middle strike.

| Leg | Action | Strike | Premium per share | Cash flow per lot of 65 |

|---|---|---|---|---|

| 1 | Buy put | 24,050 | 295.1 paid | Rs 19,182 out |

| 2 | Sell put (x2) | 23,950 | 256.6 each, received | plus Rs 33,358 in |

| 3 | Buy put | 23,850 | 224.1 paid | Rs 14,567 out |

| Net debit | about Rs 393 out |

The two sold puts at the body bring in most of the premium, and the two bought wings cost a little more, leaving a tiny net debit of about Rs 393 for the whole lot. That debit is your maximum loss.

| Number | How it is built | This trade |

|---|---|---|

| Max loss | the net debit, lost outside the wings | Rs 393 |

| Max profit | wing width Rs 6,500 minus the debit, at the body strike | Rs 6,500 minus Rs 393 = Rs 6,107 |

| Breakevens | a few points inside each wing | 23,856 and 24,047 |

Walk the trade across five closing levels and the tent draws itself. A put is worth max(strike minus NIFTY, 0) at expiry.

| NIFTY at expiry | 24,050 PE bought | 23,950 PE sold (each) | 23,850 PE bought | Net profit or loss |

|---|---|---|---|---|

| 23,800 | worth 250 | worth 150 | worth 50 | minus Rs 393 (max loss) |

| 23,856 | worth 194 | worth 94 | worth 0 | Rs 0 (breakeven) |

| 23,950 | worth 100 | worth 0 | worth 0 | plus Rs 6,107 (max profit) |

| 24,000 | worth 50 | worth 0 | worth 0 | plus Rs 2,857 |

| 24,100 | worth 0 | worth 0 | worth 0 | minus Rs 393 (max loss) |

Below 23,850 and above 24,050 the four legs cancel and you sit on the small Rs 393 loss. Between the breakevens of 23,856 and 24,047 the structure pokes above zero, climbing to its full Rs 6,107 peak only if NIFTY pins the 23,950 body exactly. Slip even fifty points either way and the reward shrinks fast. That sharpness is the butterfly's nature: a single point pays the most.

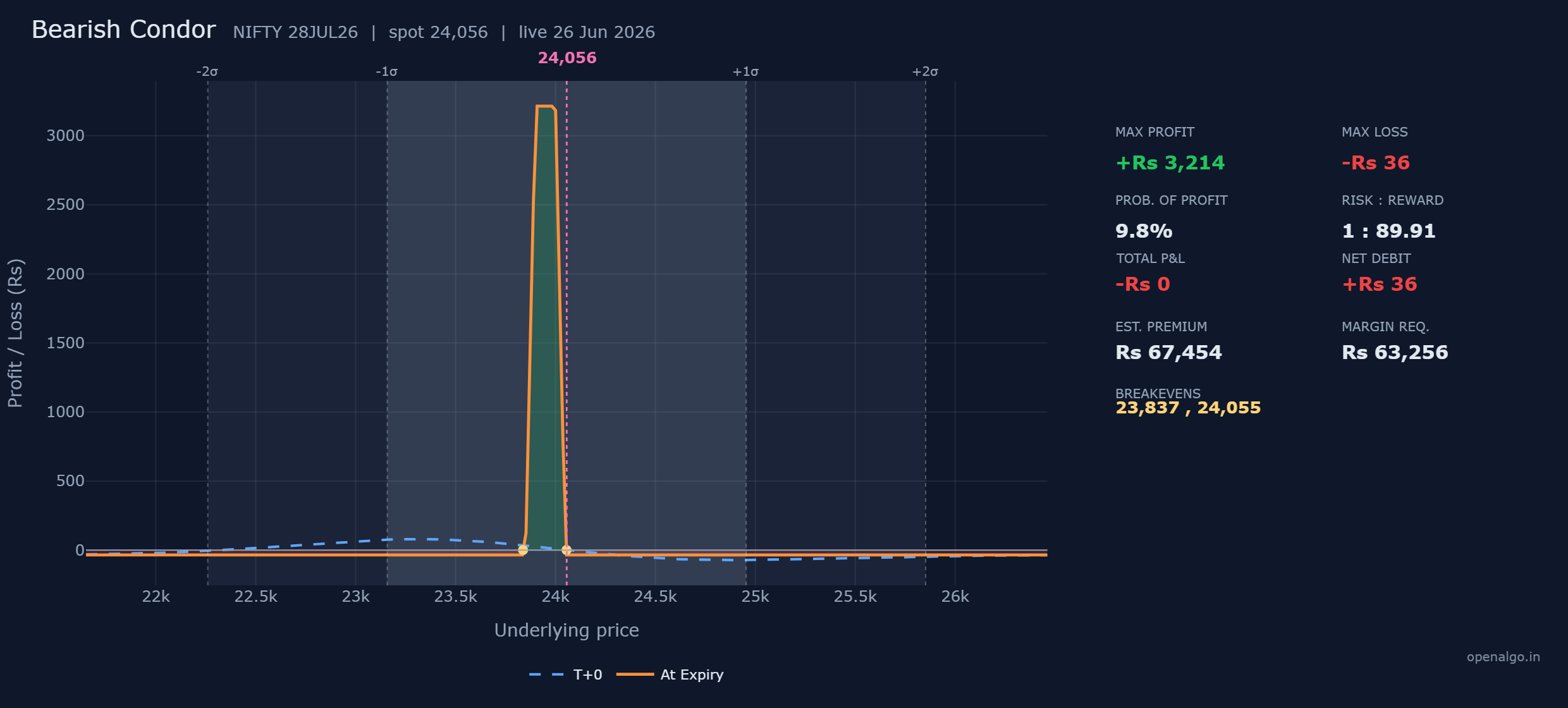

The bearish condor

The condor is a butterfly with its peak stretched into a plateau. Instead of selling two puts at one body strike, you sell them at two adjacent strikes, which spreads the maximum profit across a small range rather than a single point. It is a little more forgiving about exactly where NIFTY lands, at the cost of a lower peak.

| Leg | Action | Strike | Premium per share | Cash flow per lot of 65 |

|---|---|---|---|---|

| 1 | Buy put | 24,050 | 295.1 paid | Rs 19,182 out |

| 2 | Sell put | 24,000 | 277.1 received | plus Rs 18,012 in |

| 3 | Sell put | 23,900 | 241.6 received | plus Rs 15,704 in |

| 4 | Buy put | 23,850 | 224.1 paid | Rs 14,567 out |

| Net debit | about Rs 36 out |

The two sold inner puts again bring in most of the premium, leaving a net debit of just about Rs 36 for the lot, the cheapest entry in this entire course. That Rs 36 is the maximum loss.

| Number | How it is built | This trade |

|---|---|---|

| Max loss | the net debit, lost outside the wings | Rs 36 |

| Max profit | the 50-point upper spread (Rs 3,250) minus the debit, across the plateau | Rs 3,250 minus Rs 36 = Rs 3,214 |

| Breakevens | a hair inside each outer wing | about 23,851 and 24,049 |

Here is the condor settled at five levels of NIFTY, per lot.

| NIFTY at expiry | 24,050 PE bought | 24,000 PE sold | 23,900 PE sold | 23,850 PE bought | Net profit or loss |

|---|---|---|---|---|---|

| 24,100 | worth 0 | worth 0 | worth 0 | worth 0 | minus Rs 36 (max loss) |

| 24,000 | worth 50 | worth 0 | worth 0 | worth 0 | plus Rs 3,214 (max profit) |

| 23,900 | worth 150 | worth 100 | worth 0 | worth 0 | plus Rs 3,214 (max profit) |

| 23,851 | worth 199 | worth 149 | worth 49 | worth 0 | Rs 0 (breakeven) |

| 23,800 | worth 250 | worth 200 | worth 100 | worth 50 | minus Rs 36 (max loss) |

The orange line runs flat across the plateau between the two inner strikes, paying the same Rs 3,214 anywhere from 23,900 to 24,000, then falls away to the Rs 36 loss outside the wings. Compared with the butterfly, the tent has become a tabletop: a lower ceiling of Rs 3,214 instead of Rs 6,107, but earned over a wider landing zone instead of a single point.

Your odds, told honestly

The dazzling reward against a tiny cost makes both structures look almost too good. The catch is geometry. To win, NIFTY must finish inside a band only a couple of hundred points wide, and to win the most it must finish in an even narrower slice. With about 32 days to expiry and the sigma bands on the chart showing how far NIFTY could roam, the chance of it settling into that exact pocket below the money is genuinely small. That is what the 9 percent probability on the butterfly and the 10 percent on the condor are measuring.

Look at the reward to risk. The butterfly reads 1 to 16 and the condor an astonishing 1 to 90, because the Rs 36 debit is so small against the Rs 3,214 it can earn. These look like the best trades in the course. The number that keeps you honest is the probability of profit, only 9 to 10 percent. A 1 to 90 payoff that wins one time in ten is a lottery ticket, not an edge.

The low odds are not a flaw in the trade. They are the price of the huge payoff. The market does not hand out 1 to 90 odds on likely events. So the cheapness is a feature and a trap at once, and the next section is where that trap bites.

Margin and what you actually risk

Both structures show a margin of about Rs 63,000, around Rs 63,606 for the butterfly and Rs 63,256 for the condor. That figure reflects the four separate legs the exchange must track, not your real exposure. Your actual cash at risk is only the tiny net debit, Rs 393 or Rs 36, because the bought wings cap every outcome. The return-on-margin lens that suited the simple spreads does not fit here, since the margin is large for bookkeeping reasons while the true risk is a rounding error.

A near-zero cost is not a near-zero risk once you size up. Ten lots of the bearish condor risk Rs 360 and ten lots of the butterfly risk Rs 3,930, and you will lose that full amount roughly nine or ten times out of ten, because the probability of profit is only about 10 percent. The temptation to treat a few-hundred-rupee ticket as free money and stack many lots is exactly how a low-odds bet turns into a real loss. Size these as small, deliberate bets, not as cheap lottery strips to load up on.

Time decay and why to place these late

These are net-debit structures, but their relationship with time is unusual. A butterfly or condor only reaches its full tent at expiry, when every option settles to pure intrinsic value. Right now the blue T+0 line is far flatter than the orange at-expiry line, because the sold body puts still carry time premium that has not yet drained. The structure earns its shape as the clock runs down, but only if NIFTY is sitting in the pocket when that happens.

Place these closer to expiry, not far from it. A butterfly or condor pinned weeks early gives NIFTY too much time to wander out of the narrow band, and the tent has barely formed. The same structure put on in the final week, when the sigma bands have shrunk and you have a strong read on where the index will settle, has a far better chance of landing in the pocket and paying its full peak.

Butterfly or condor

Used with clear eyes, both have a real role. They are the right tool when you hold a specific, time-bound view that NIFTY will ease down to a particular level and stall there, perhaps into a known support or ahead of an event you expect to pin the index. You are paying a few hundred rupees for a defined-risk ticket on that precise outcome, and if you are right the payoff dwarfs the cost.

- Choose the butterfly when your view of the landing spot is sharp and you want the highest payoff for pinning the 23,950 body exactly. It pays Rs 6,107 at its peak.

- Choose the condor when you want a little more room, accepting a lower ceiling of Rs 3,214 in exchange for a plateau that pays anywhere from 23,900 to 24,000.

Both keep your worst case printed on the ticket, Rs 393 or Rs 36, which is exactly the discipline this course keeps pressing.

The estimated premium on these trades is a turnover figure across all four legs and looks large, but it is not your risk. Your risk is the small net debit, Rs 393 or Rs 36, because the bought wings cap every outcome. Never read the gross premium as the amount you can lose. Read the net debit, which the builder reports as the maximum loss.

You can construct both in sandbox trading (analyzer mode in OpenAlgo), adding the legs one at a time and watching the sharp tent of the butterfly soften into the tabletop of the condor as you split the body into two strikes. Slide the modelled price across the chart and see how rarely it lands in the profit band, and how richly it pays on the few occasions it does. That feel, cheap and brilliant but seldom right, is exactly the honest lesson of the directional butterfly and condor. With this chapter the bearish family is complete, and next we turn to the trades that do not care about direction at all, betting instead on how far NIFTY moves.

Key takeaways

- A bearish butterfly buys a put above, sells two at the body, and buys a put below, all under the spot. The tiny Rs 393 debit is the max loss, the max profit is Rs 6,107 at the 23,950 body, and the breakevens are 23,856 and 24,047.

- A bearish condor splits the body into two sold strikes, giving a flat Rs 3,214 plateau between 23,900 and 24,000 for a max loss of only Rs 36.

- Both show breathtaking reward to risk, 1 to 16 and 1 to 90, but the probability of profit is only 9 to 10 percent, because NIFTY must land in a narrow pocket.

- The large Rs 63,000 margin reflects four legs of bookkeeping, not real exposure. Your true risk is the small net debit, and the bought wings cap every outcome.

- Time builds the tent as expiry nears, so these work best placed late in the cycle, when the expected range has shrunk and your read on the landing spot is strong.

- Treat them as small, deliberate, low-odds bets on a precise landing, never as cheap money to stack across many lots.