Pledging for Margin, Smartly

Pledging lets you trade on assets you already own without selling them. Learn how the haircut decides how much margin you get, why liquid collateral beats volatile stock, the interest cost of breaching the cash component, the covered-call trick, and the margin-call risk.

- ·How pledging works

- ·Haircuts and how much margin you get

- ·Cash vs non-cash collateral

- ·The cash-component interest cost

- ·Trick one: prefer liquid collateral

- ·Trick two: the covered call

- ·Margin-call and forced-selling risk

Last chapter you learned that selling options and holding futures block margin, and that you can meet that margin by pledging assets you already own instead of freezing cash. This chapter makes that practical. Pledging is one of the most useful and most misunderstood tools a trader has. Used well, it lets your long-term portfolio quietly fund your trading without selling a single share. Used carelessly, it can turn a falling market into a forced sale of the very holdings you wanted to keep. Let us learn to use it the smart way, with the haircut maths, the hidden interest cost, two genuinely useful tricks, and an honest look at the risk.

What pledging actually does

Pledging is you saying to your broker, here, hold my shares as security, and in return give me extra margin to trade. The shares never leave your demat account. You still own them, you still receive their dividends and bonuses, they are simply flagged as collateral. In return, their value, after a reduction we will meet in a moment, is added to your trading margin.

A simple picture. Suppose you own shares worth about Rs 2,00,000 sitting idle in your demat account. Rather than sell them to raise trading funds, you pledge them and receive roughly Rs 1,70,000 of usable margin. That margin can support buying more shares, an F&O position, or an intraday trade. You scaled up without putting in fresh cash and without selling what you hold. That is the whole appeal.

Two things are worth knowing up front. First, only approved securities can be pledged, not every stock qualifies. Beyond shares you can also pledge liquid ETFs, liquid funds, equity ETFs and mutual funds. The approved list lives on your broker's platform and on the exchange website. Second, pledging is not free of formalities, but it is quick. You request it, approve it with an authentication step at the depository, and the margin is usually credited the same day.

When you pledge, the asset stays yours and stays in your demat account, just marked as collateral. You keep the dividends and bonuses and you can unpledge any time, with no lock-in. Pledging gives you trading margin without selling, which is its single biggest benefit.

The haircut decides how much you get

You never receive the full market value of a pledged security as margin. The exchange applies a haircut, a percentage reduction to the market value, and only the amount left after the haircut becomes usable margin. The haircut is a safety buffer for the lender against the collateral itself falling in price.

An example makes it concrete. Pledge a security worth Rs 10,000 with a 20 percent haircut, and you receive Rs 8,000 as usable margin. The other Rs 2,000 is held back as the buffer. The haircut is not the same for every asset. Stable, liquid instruments carry small haircuts, while risky, volatile stocks carry large ones, because a volatile stock can fall further before the broker can sell it.

So the margin you actually get depends not just on the value of the asset but on its haircut, and those haircuts can change over time. A stable large stock might carry a haircut near 9 percent, while a jumpier one might carry close to 18 percent or more, so the same Rs 2,00,000 of holdings can hand you very different margin depending on which stock it is.

Cash collateral versus non-cash collateral

Pledged assets fall into two buckets, and the difference matters for both how much you can do and what it costs.

- Cash and cash-equivalent collateral: liquid ETFs, liquid funds, government securities, sovereign gold bonds and treasury bills. The system treats these almost like cash.

- Non-cash or equity collateral: ordinary stocks, equity ETFs and equity mutual funds.

Here is the rule that links them. When you use pledged margin for F&O, at least half of the total margin must be met in cash or cash-equivalents, and the other half may be non-cash. This is the same cash-component rule from the last chapter, and pledging is where its cost becomes visible.

If you fall short on the cash half and fund it with non-cash collateral for an overnight position, the exchange charges interest on that shortfall, currently about 0.035 percent per day, which works out to roughly 12.775 percent a year. Lean entirely on pledged stocks with no cash leg and you are quietly paying interest every single day the position is open.

A quick number. Say a position needs Rs 1,00,000 of margin and you hold Rs 1,00,000 of pledged stocks but no liquid collateral at all. The cash requirement of Rs 50,000 is missing, so it is funded by your stocks, and the interest on that Rs 50,000 shortfall is about Rs 17.5 a day. Small per day, but it runs for as long as the position is open, and it is pure drag on your return.

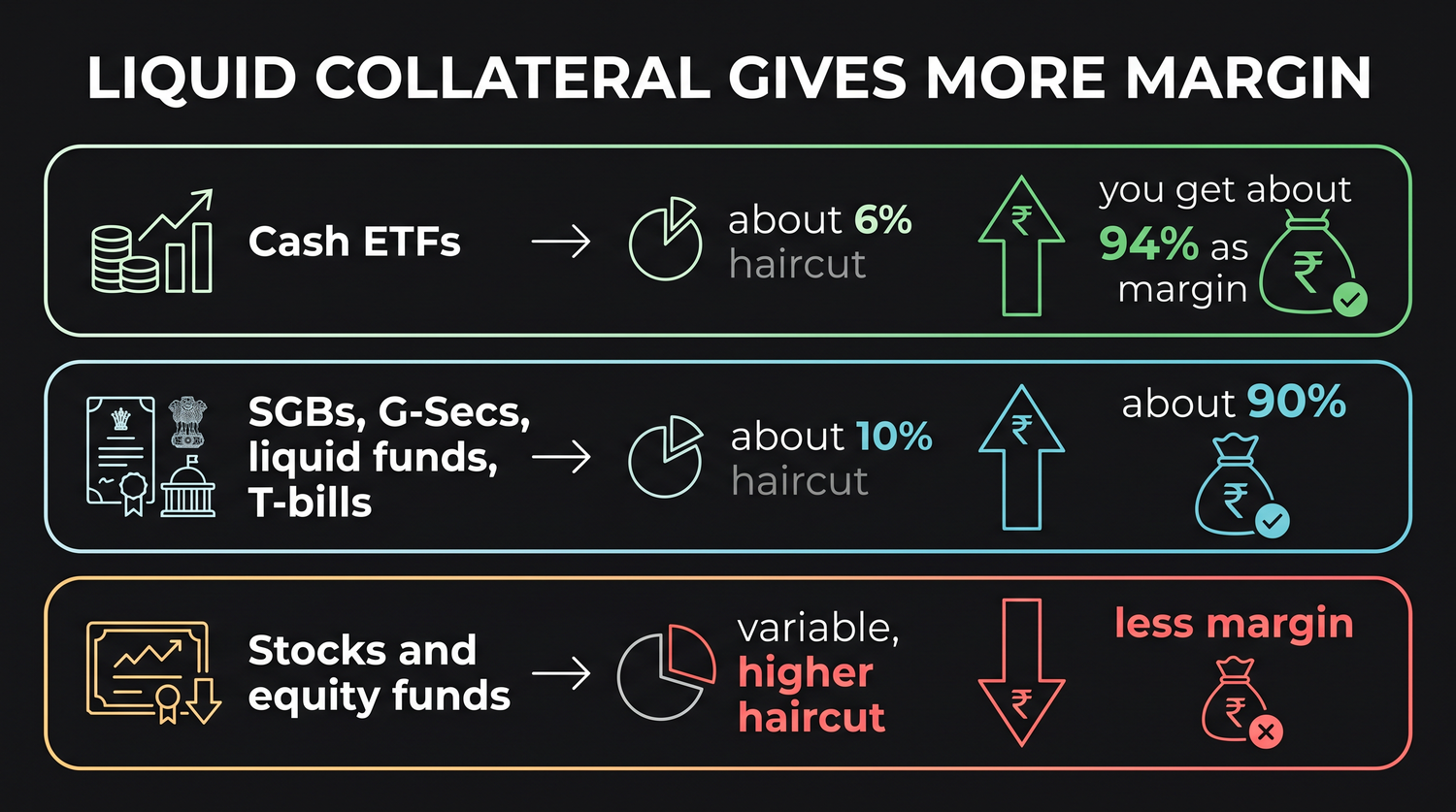

Trick one, prefer liquid collateral

The first smart habit is to pledge liquid, cash-equivalent collateral wherever you can, rather than leaning on volatile stock. There are two clear reasons.

The first is simple efficiency. Liquid collateral has a smaller haircut, so it hands you more margin per rupee pledged. Cash ETFs may carry a haircut of only about 6 percent, giving you roughly 94 percent as margin. Sovereign gold bonds, government securities, liquid funds and treasury bills sit around a 10 percent haircut, giving about 90 percent. Stocks and equity funds, with their larger and variable haircuts, give you less and an uncertain amount.

The second reason is safety. When you pledge stable cash collateral, its value barely moves, so your margin stays put and you are not exposed to a margin call from the collateral side. Pledge a volatile stock instead, and if the market falls, the value of your collateral falls too. Your margin shrinks, and your broker may ask you to top up. Pledge Rs 1,00,000 of a liquid instrument at a 6 percent haircut and you hold a steady Rs 94,000 of margin. Pledge Rs 1,00,000 of a volatile stock at a 20 percent haircut and you start with Rs 80,000, but a 20 percent fall in the stock drops its value to Rs 80,000, and the haircut on that lower value leaves you only about Rs 64,000. That shortfall can trigger a margin call on collateral you only pledged, never even traded.

If you have a choice, pledge liquid collateral for the cash half of your margin and keep volatile stock as a smaller, non-cash top-up. You get more margin, you avoid paying the cash-shortfall interest, and you remove the risk of your own collateral triggering a margin call.

Trick two, the covered call

What if your portfolio is all equity and you hold no liquid instruments at all? You can still put pledged stock to work through a covered call, the strategy you met earlier. The idea is to earn income from shares you are holding anyway.

Suppose you own 500 RELIANCE shares near Rs 1,318, a holding worth about Rs 6,59,000. You pledge them, and after a haircut of roughly 9 percent you receive about Rs 6,00,000 of margin. Against that margin you sell one lot of a higher RELIANCE call, say the 1360 strike for about Rs 16 a share, which puts roughly Rs 8,000 of premium into your account up front. If RELIANCE finishes above 1360, your shares have gained and that gain offsets the sold call. If it finishes below 1360, the call expires worthless and you simply keep the premium as income on shares you were holding regardless. Remember the cash-component cost though, since if the F&O margin has no cash leg behind it, the interest on the shortfall still applies for as long as the short call is open.

A covered call is the natural way to make an all-equity portfolio earn while pledged. You are not taking a new directional bet, you are renting out the upside above a strike you would be happy to sell at anyway, and collecting premium for it.

How you pledge, and the real risk

The mechanics are straightforward. On your broker's platform you go to your holdings, choose the stocks and quantities to pledge, and submit the request. After an approval step at the depository the margin is credited the same day, usually within minutes. Unpledging follows the same path and is free, and if you simply sell a pledged stock it is unpledged automatically as part of the sale. The exact screens differ by broker, but the shape is the same everywhere.

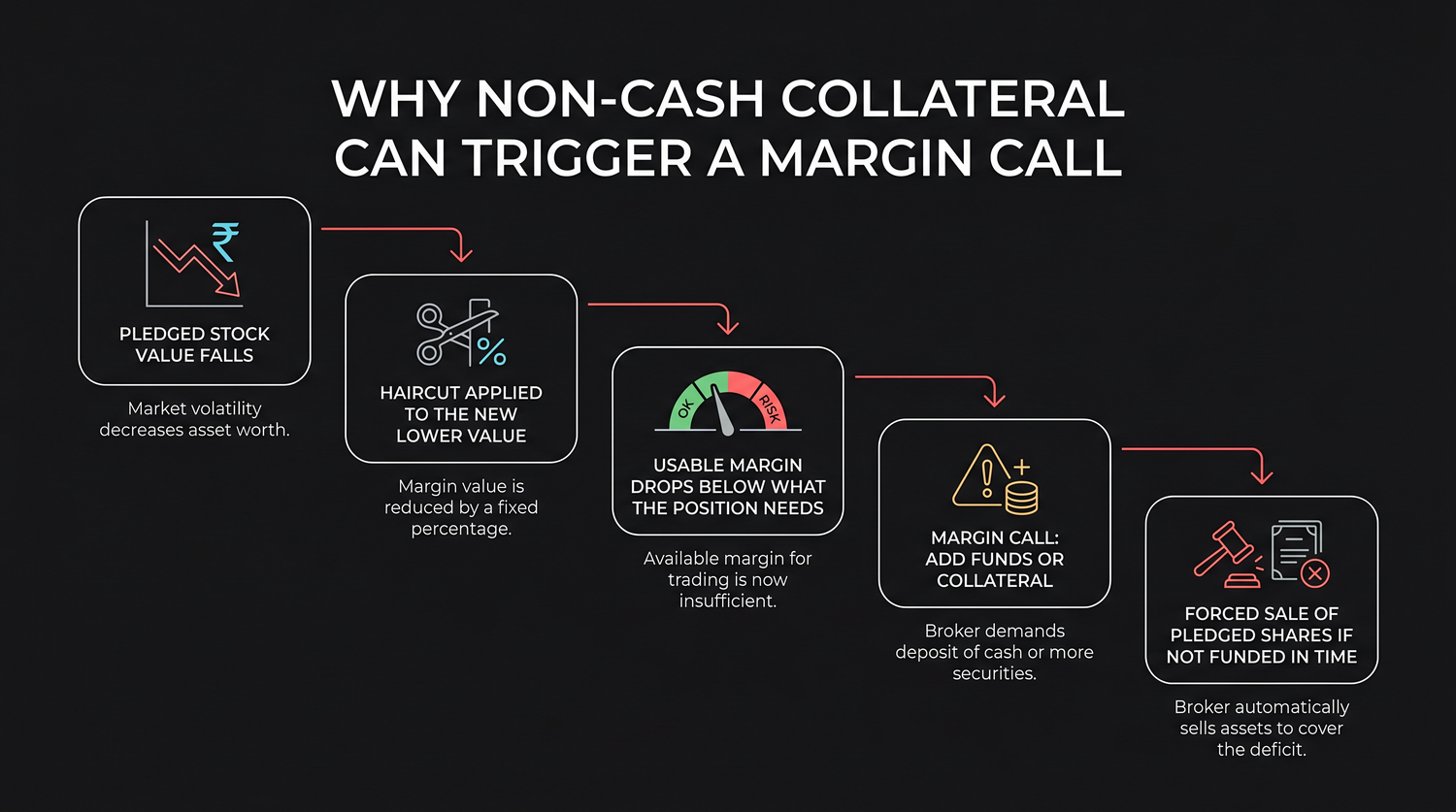

Now the risk, because pledging cuts both ways. The danger lives entirely in pledging volatile, non-cash collateral and then trading against it.

Walk one example through. You pledge RELIANCE shares worth Rs 2,00,000 and, after a 9 percent haircut, receive about Rs 1,82,000 of margin, which you use for an F&O position. Then RELIANCE falls 10 percent, so your collateral is now worth Rs 1,80,000, and the 9 percent haircut on that leaves only about Rs 1,63,800 of margin. You now have a shortfall of roughly Rs 18,200. The broker issues a margin call, asking you to add that amount in cash or pledge more collateral. If you cannot, the broker will sell enough of your pledged RELIANCE shares at the current market price to recover the gap. That forced sale locks in a loss on the shares and shrinks your long-term holding. So a bad day can cost you twice, once on the trade and once on the portfolio you never meant to sell.

Pledging volatile stock and trading against it doubles your risk. A falling market can both hurt your F&O position and shrink your pledged collateral, and if you cannot meet the resulting margin call the broker sells your shares for you at a bad price. The forced sale is the real danger of pledging, not the haircut.

So should you pledge?

Pledging is genuinely powerful, but it is not for everyone or every situation. Three honest tests decide it.

- Pledging gives you extra buying power, but it also magnifies your risk. If you are not prepared to manage that, it is better to skip it.

- For an active trader chasing short-term opportunities, pledging is a useful tool. For a long-term investor who simply wants to hold, it adds a risk they do not need.

- Pledging only makes sense alongside strict stop-losses and disciplined position sizing. Without those, it turns small mistakes into large ones.

Used inside a clear risk plan, pledging unlocks liquidity from assets you already own and lets your portfolio and your strategies work at the same time. Used without one, it can quietly convert a routine market dip into a permanent loss of your holdings. With the funding side now understood, the next chapter turns to what happens when your margin falls short of the minimum, the world of margin penalties.