Bullish Butterfly and Bullish Condor

Defined-risk ways to target a specific upside zone. Learn the bullish butterfly and bullish condor, all-call structures that pay the most if NIFTY drifts up to a chosen level, with the metrics.

- ·A targeted bullish view

- ·The bullish butterfly

- ·The bullish condor

- ·Cheap, high reward to risk

- ·Why the POP is low

- ·Reading the real payoffs

Every trade so far has asked NIFTY for a broad favour: please rise, please do not crash, please stay roughly here. The two structures in this chapter ask for something far more precise. The bullish butterfly and the bullish condor are tiny, surgical bets that NIFTY drifts up to a specific landing spot and sits there at expiry. They cost almost nothing, barely a hundred rupees of risk, and they can pay many times that back. The catch, stated honestly up front, is that they win only about one time in ten, because the index has to finish inside a narrow window. This chapter builds both on real NIFTY data captured on 26 June 2026, spot 24,056, lot 65, expiry 28 July 2026, and teaches them as exactly what they are: cheap tickets on a precise view, never a steady way to earn.

The one-line idea

Both structures are built entirely from call options, and both stack a set of bought and sold strikes so the wings fence in your risk on each side. A bullish butterfly buys one lower call, sells two middle calls, and buys one higher call, with the body nudged just above the money so it pays best at a single target. A bullish condor spreads that body into two separate sold strikes, trading a lower peak for a small landing zone instead of a single point. In both, the premiums you collect from the sold calls almost exactly pay for the calls you buy, so you walk in for a tiny net debit, and that tiny debit is the whole of your risk.

A bullish butterfly and a bullish condor are cheap, defined-risk bets that NIFTY climbs to a precise target by expiry and stops there. You pay a tiny debit, that debit is the most you can lose, and the wings cap the trade on both sides. The reward to risk is spectacular, but the odds of landing in the window are low. These are targeted long shots, not core positions.

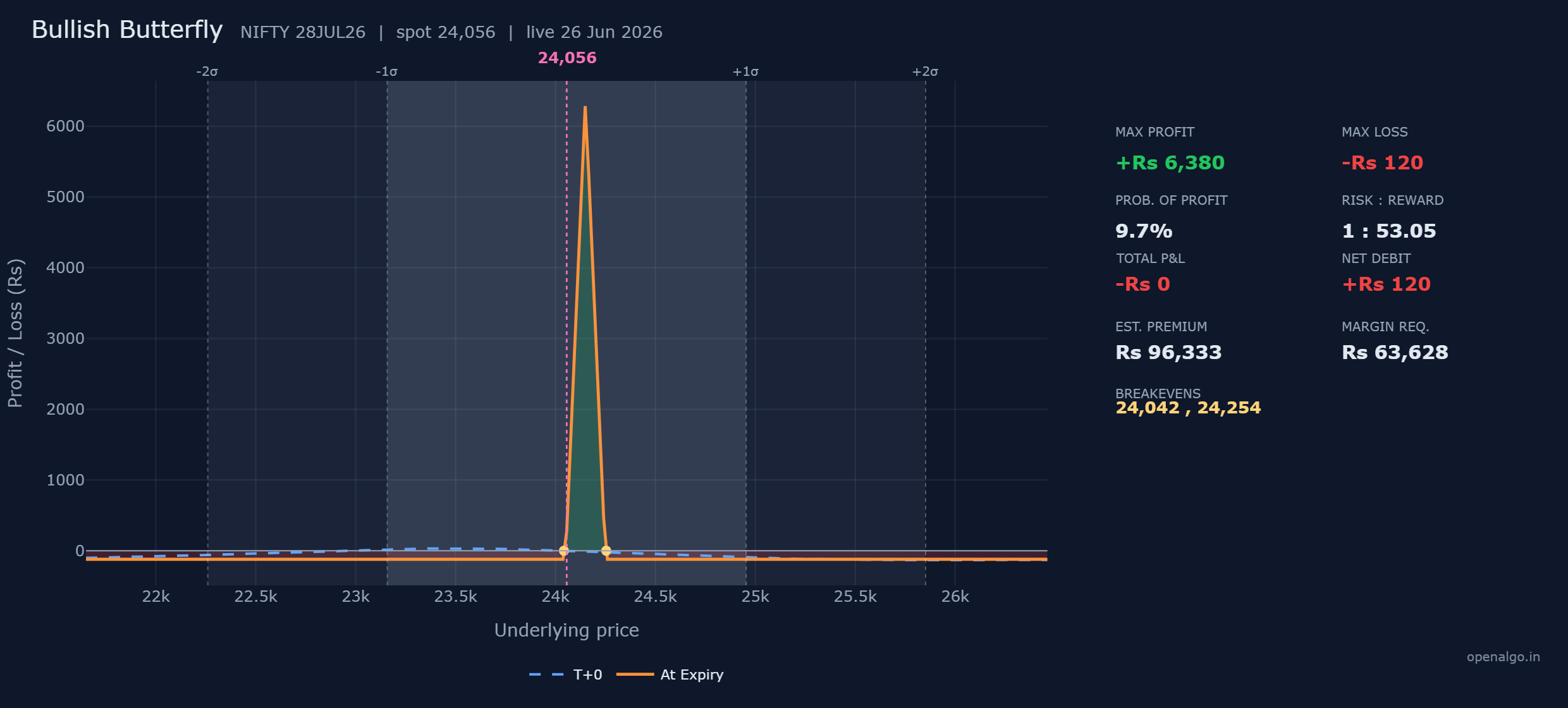

The bullish butterfly, rupee by rupee

Here is the butterfly on real NIFTY prices, three strikes and four legs, the body sold twice at 24,150 and the wings bought at 24,050 and 24,250.

| Leg | Action | Strike | Premium per share | Cash flow per lot of 65 |

|---|---|---|---|---|

| 1 | Buy call | 24,050 | 425.8 paid | Rs 27,677 out |

| 2 | Sell two calls | 24,150 | 740.2 received | plus Rs 48,113 in |

| 3 | Buy call | 24,250 | 316.1 paid | Rs 20,547 out |

| Net debit | about Rs 120 out |

Add the two bought wings together and they cost Rs 48,224. The two sold body calls bring back Rs 48,113. The gap between them is just Rs 120, and that is the entire price of the trade. Because the wings box the structure in above and below, you can never be asked for a rupee more, so this Rs 120 is also the maximum loss.

The three numbers, and where they come from

Each number falls straight out of the trade. The peak sits at the body strike, the floor is the debit, and the breakevens hug the wings.

Maximum profit is Rs 6,380. If NIFTY finishes exactly at the body strike of 24,150, your bought 24,050 call is 100 points in the money while the two sold calls and the upper wing are all worthless. That intrinsic value is 100 times 65, which is Rs 6,500, and after subtracting the Rs 120 you paid you keep Rs 6,380. That is the single sharp tip of the tent.

Maximum loss is Rs 120, the net debit. Anywhere the structure expires outside the wings, every call either cancels or is worthless, and all you forfeit is the tiny amount you paid to enter.

The breakevens sit at about 24,042 and 24,254, essentially the outer wings. The debit is so small, under two points a share, that it barely shifts the points where the tent crosses zero, so they land right at the wings.

| Number | How it is built | This trade |

|---|---|---|

| Max profit | gap from wing to body, times the lot, minus the debit | 100 points times 65, which is Rs 6,500, minus Rs 120, equals Rs 6,380 |

| Max loss | the net debit you paid | Rs 120 |

| Breakevens | the outer wings, barely moved by the tiny debit | about 24,042 and 24,254 |

Walking the outcomes at expiry

Settle the butterfly at five NIFTY levels and the tent draws itself. Each call is worth its intrinsic value at expiry, a call being worth whatever NIFTY finishes above its strike, and the doubled body leg owes you twice that.

| NIFTY at expiry | 24,050 call (bought) | 24,150 calls (sold, two) | 24,250 call (bought) | Net profit or loss |

|---|---|---|---|---|

| 23,900 | worth 0 | worth 0 | worth 0 | minus Rs 120 (max loss) |

| 24,050 | worth 0 | worth 0 | worth 0 | minus Rs 120 (the floor) |

| 24,150 | worth 100 | worth 0 | worth 0 | plus Rs 6,380 (max profit) |

| 24,250 | worth 200 | 2 times 100 owed | worth 0 | minus Rs 120 (back to floor) |

| 24,400 | worth 350 | 2 times 250 owed | worth 150 | minus Rs 120 (max loss) |

Read it down the page. Far to the left and far to the right the line lies flat at a loss of Rs 120, so small it almost touches zero. Only around 24,150 does it spike into a tall, thin peak. Notice the top row at 24,400: the bought 24,250 wing comes alive and exactly offsets what the two sold calls owe, which is precisely why the loss never grows past Rs 120 no matter how far NIFTY runs.

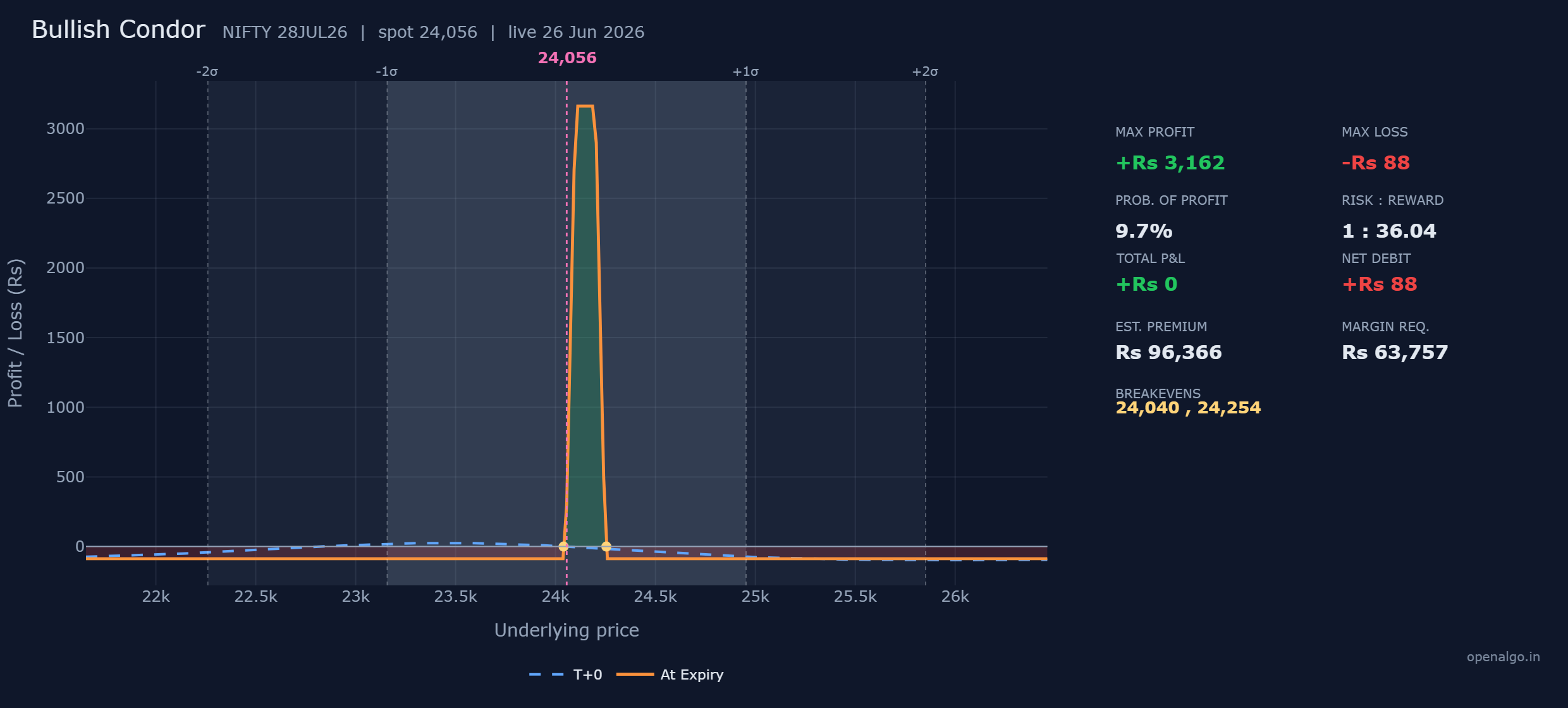

The bullish condor, rupee by rupee

The condor takes the same idea and stretches the peak into a plateau. Instead of selling one strike twice, you sell two different middle strikes, 24,100 and 24,200, so the top of the tent becomes a small flat shelf rather than a single point.

| Leg | Action | Strike | Premium per share | Cash flow per lot of 65 |

|---|---|---|---|---|

| 1 | Buy call | 24,050 | 425.8 paid | Rs 27,677 out |

| 2 | Sell call | 24,100 | 397.6 received | plus Rs 25,844 in |

| 3 | Sell call | 24,200 | 342.9 received | plus Rs 22,289 in |

| 4 | Buy call | 24,250 | 316.1 paid | Rs 20,547 out |

| Net debit | about Rs 88 out |

Once again the two sold calls nearly pay for the two bought wings, leaving a net debit of just Rs 88, which is the whole maximum loss. The two sold strikes mark the edges of a flat profit plateau between them.

Its three numbers are built the same way. The maximum profit is Rs 3,162: anywhere on the plateau the bought 24,050 call sits 50 points ahead of the first sold strike, worth 50 times 65, which is Rs 3,250, and after the Rs 88 debit you keep Rs 3,162. The maximum loss is Rs 88, the debit. The breakevens sit at about 24,040 and 24,254, again essentially the outer edges of the structure. Now walk it across five levels.

| NIFTY at expiry | 24,050 call (bought) | 24,100 call (sold) | 24,200 call (sold) | 24,250 call (bought) | Net profit or loss |

|---|---|---|---|---|---|

| 23,950 | worth 0 | worth 0 | worth 0 | worth 0 | minus Rs 88 (max loss) |

| 24,100 | worth 50 | worth 0 | worth 0 | worth 0 | plus Rs 3,162 (max profit) |

| 24,150 | worth 100 | 50 owed | worth 0 | worth 0 | plus Rs 3,162 (max profit) |

| 24,200 | worth 150 | 100 owed | worth 0 | worth 0 | plus Rs 3,162 (max profit) |

| 24,350 | worth 300 | 250 owed | 150 owed | worth 100 | minus Rs 88 (max loss) |

The three middle rows tell the story: anywhere from 24,100 to 24,200 the trade pays the same Rs 3,162, a flat shelf rather than the butterfly's single spike. You traded peak height, Rs 3,162 against the butterfly's Rs 6,380, for a wider place to land.

The only real difference between these two is the width of the bullseye. The butterfly pays the most but only at one exact strike, 24,150. The condor pays less but across a small band of strikes, 24,100 to 24,200. Choose the condor when you have a rough target zone, the butterfly when your conviction about the precise landing point is strong.

Your odds

This is where honesty matters most. Both structures show a dazzling reward to risk, the butterfly 1 to 53 and the condor 1 to 36, but the probability of profit on each is only about 10 percent. That figure comes from the option market itself: using the volatility priced into NIFTY, about 12.7 percent, and the 32 days left, the market implies only a one in ten chance that the index drifts into your narrow window and stays there. Look at the chart and the reason is plain. The faint sigma bands show the range NIFTY is expected to travel in a month, and the profitable zone is a thin sliver inside it. About nine times in ten NIFTY finishes outside the window and you lose your tiny debit. About one time in ten it lands in the zone and you collect a multiple of that.

Never read the 1 to 53 reward to risk on its own. Always pair it with the 10 percent probability of profit sitting right beside it. The most likely single outcome, by far, is the small loss. These trades are cheap precisely because they rarely pay, and the cheapness is the market telling you the odds.

Margin, and what you really tie up

Here is the honest wrinkle that the tiny debit hides. Although the cash you can lose is only Rs 88 to Rs 120, the margin the exchange blocks is far larger, about Rs 63,628 for the butterfly and Rs 63,757 for the condor, because each structure contains sold call legs that are margined on exposure. So your real risk is trivial, but you still tie up meaningful capital to hold the position.

That gap reshapes how you judge the return. The butterfly's best case, Rs 6,380 against Rs 63,628 of blocked capital, is a return on margin of about 10 percent if it lands perfectly, and the condor's Rs 3,162 against Rs 63,757 is about 5 percent. Those are fine returns, but remember they arrive only one time in ten, which is why these belong in a small corner of an account, never as a core holding for a small or fully invested one.

Time decay

Look at the blue dashed T+0 line against the solid orange at-expiry line. Today the blue line is a gentle, rounded hump; only at expiry does the orange line sharpen into the tall tent. That difference is time value, and for these structures time is a quiet ally in one specific way. If NIFTY is already sitting near your target as expiry approaches, the sold body calls bleed their remaining time value and the position firms up toward its peak. If NIFTY is nowhere near the target, time simply lets the small debit expire, which costs you almost nothing. The decay works for you only when price is camped on the bullseye.

Butterfly or condor, and when to use either

These are the same tool set to two different widths, so the choice is about how sure you are of the landing spot.

| Bullish butterfly | Bullish condor | |

|---|---|---|

| Net debit and max loss | Rs 120 | Rs 88 |

| Max profit | Rs 6,380 | Rs 3,162 |

| Reward to risk | 1 to 53 | 1 to 36 |

| Probability of profit | about 10 percent | about 10 percent |

| Best when | you have a single precise target | you have a small target zone |

Reach for either only when you hold a clear target price and a clear expiry, for example you expect NIFTY to grind up to about 24,150 and stall by month end. Place the body at that target, keep the stake small because the odds are against you, and treat the rare big payoff as a bonus rather than a plan. If you have no precise target, a defined-risk spread from the earlier chapters is the better and far more reliable bullish tool.

Do not be seduced by the 1 to 53 reward to risk in isolation. The probability of profit is only about 10 percent, so the most likely outcome by a wide margin is that NIFTY misses the window and you lose the small debit. These bets are cheap because they rarely pay. Treat them as occasional, low-stake punts on a precise view, never as a reliable way to make money, and size them so a string of small losses never matters.

Key takeaways

- A bullish butterfly buys one lower call, sells two body calls, and buys one higher call, all for a tiny net debit of about Rs 120, which is the entire maximum loss.

- A bullish condor spreads the body into two sold strikes for a net debit of about Rs 88, turning the single peak into a small plateau.

- Max profit lands at the body or across the plateau, Rs 6,380 for the butterfly and Rs 3,162 for the condor, giving a spectacular reward to risk of 1 to 53 and 1 to 36.

- The probability of profit is only about 10 percent on each, because NIFTY must finish inside a narrow window; the cheapness is the market pricing those long odds.

- Although the cash loss is tiny, the margin blocked is about Rs 63,000 on each because of the sold legs, so these tie up real capital for a one in ten payoff.

- Use them when you have a precise target and a clear expiry, keep the stake small, and never mistake a cheap long shot for an income strategy.