Margin and Collateral for F&O

Selling options and trading futures blocks margin, but you do not always need cash. Learn how the margin is built from SPAN and exposure, how the OpenAlgo margin calculator shows it, and which assets you can pledge as collateral instead of cash.

- ·Why selling needs margin

- ·SPAN and exposure margin

- ·The OpenAlgo margin calculator

- ·Pledging collateral instead of cash

- ·What counts as F&O collateral

- ·Haircuts and the cash component

Every strategy in this course costs something to put on. A debit spread costs the premium you pay. A credit strategy looks like it pays you, yet it quietly demands something larger in the background: margin. Sell a strangle, run an iron condor, or hold a futures leg in a synthetic, and the exchange blocks a sum of money for as long as the position is open. For a beginner this is often the biggest surprise of the whole subject. You collected Rs 10,000 of credit, so why is more than a lakh suddenly frozen in your account? This chapter answers that, and then shows you the part most new traders never discover: you do not always have to freeze cash at all. You can pledge things you already own.

Why a short position blocks margin

A buyer of an option pays a premium and is then finished. The most they can lose is already paid, so the exchange needs no further security from them. A seller is the opposite. They collect a small premium but take on a large, sometimes open-ended obligation, so the exchange demands a deposit, the margin, as security that the seller can actually pay if the trade goes wrong. The same is true of every futures leg.

That margin is not a single arbitrary figure. It is built from two parts.

- SPAN margin is the core. SPAN is the exchange's risk model, and this is the amount it calculates to cover a worst-case one-day move in your exact position. A short strangle, which can lose on a big move either way, draws a large SPAN number. A defined-risk iron condor, where bought wings cap the loss, draws a much smaller one.

- Exposure margin is an extra buffer the exchange adds on top of SPAN, a second cushion for an unusually violent day.

Add the two and you have the total margin required, the sum that must sit blocked in your account before the order goes through and stays blocked until you close.

A short or futures position blocks margin equal to SPAN plus exposure. It has nothing to do with the small credit you collect. It reflects the risk you are carrying, which is why a naked short strangle ties up far more than a defined-risk condor of the same underlying.

OpenAlgo includes a margin calculator so none of this is guesswork. You give it the legs of your strategy, the side of each, and the quantity, and it returns the SPAN margin, the exposure margin, and the total required. Checking it before you place a multi-leg order tells you in seconds whether the position fits your account, and it also reveals a pleasant fact about defined-risk structures: because the exchange can see your bought wings, it charges you far less margin for a condor or a butterfly than for the naked short that sits inside it. Defined risk is cheaper to hold, not just safer.

Run the margin calculator on the whole strategy, not leg by leg. The exchange margins the combined position, so a hedged structure like an iron condor is charged on its true, capped risk. Pricing it as separate legs would badly overstate what you actually need to set aside.

The cash-drag problem

Here is the practical pain. Suppose a short strangle on an index needs about Rs 1,50,000 of margin. If you had to keep Rs 1,50,000 in idle cash for the whole month the position runs, that cash earns you nothing while it sits there as security. For an active trader running several positions, lakhs of rupees can end up frozen and unproductive. That is cash drag, and it is a real cost even though no money has been lost.

The system has a sensible answer. Most traders already own assets, shares, funds, bonds, that are doing nothing but sitting in a demat account. Why not let those assets stand as the security instead of idle cash? That is exactly what pledging allows.

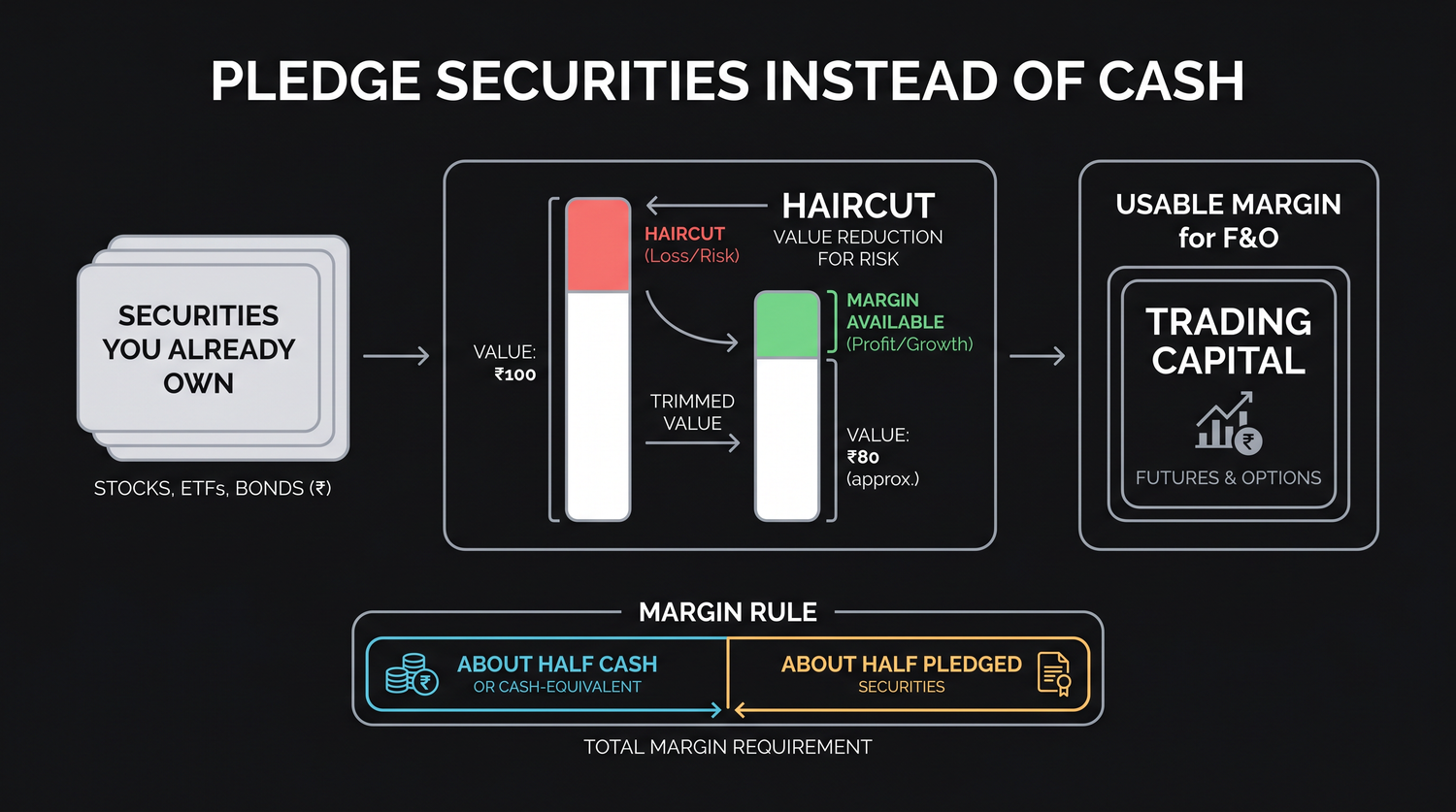

Pledging collateral instead of cash

When you pledge a security, you tell your depository to mark it as collateral for trading. The asset never leaves your demat account, you still receive its dividends or interest, and you still own it. It is simply flagged as security, and in return its value is added to your trading margin. You can then use that margin to sell options or hold futures without parking the equivalent cash.

There is one catch, and it is fair. The exchange will not give you full value for a pledged security, because the security itself can fall in price. It applies a haircut, a discount to the market value, and only the post-haircut amount counts as margin. A steady, liquid asset gets a small haircut. A volatile stock gets a large one.

A simple example makes it concrete. Pledge Rs 1,00,000 of a large stock and, after a haircut of perhaps twenty to twenty-five percent, you might receive about Rs 75,000 to Rs 80,000 of usable margin. Pledge Rs 1,00,000 of a government bond or a liquid fund and the haircut is tiny, so you receive close to Rs 95,000 or more. The safer the collateral, the more margin it gives.

A haircut is the gap between what a security is worth and what it is allowed to count for as margin. It protects the exchange against the collateral falling in value before it can be sold. The more stable the asset, the smaller the haircut, which is why a G-Sec stretches further as collateral than a single stock does.

The cash-component rule

Pledged securities are powerful, but they cannot do the whole job. The exchange requires that at least half of your total margin be met in cash or cash-equivalents, with the rest allowed in non-cash collateral such as stocks and equity funds. This is the cash-component rule, and it exists so that if a position moves against you, there is genuine cash on hand to settle the daily loss, not just pledged shares that themselves might be falling.

Cash-equivalents are the near-cash items the exchange treats almost like cash for this purpose, which conveniently includes some of the very assets you can pledge, such as government securities, sovereign gold bonds and liquid funds. So a sensible collateral mix might be a layer of pledged stocks for the non-cash half and a layer of liquid funds or G-Secs for the cash-equivalent half. If you lean too heavily on non-cash collateral and fall short on the cash component, the broker charges interest on the shortfall, which quietly eats your returns.

Never fund a position entirely with pledged stocks. At least half the margin must be cash or cash-equivalents, and the daily mark-to-market losses are always debited in cash. A book full of non-cash collateral with no cash buffer is exactly the account that gets a forced exit on a violent day.

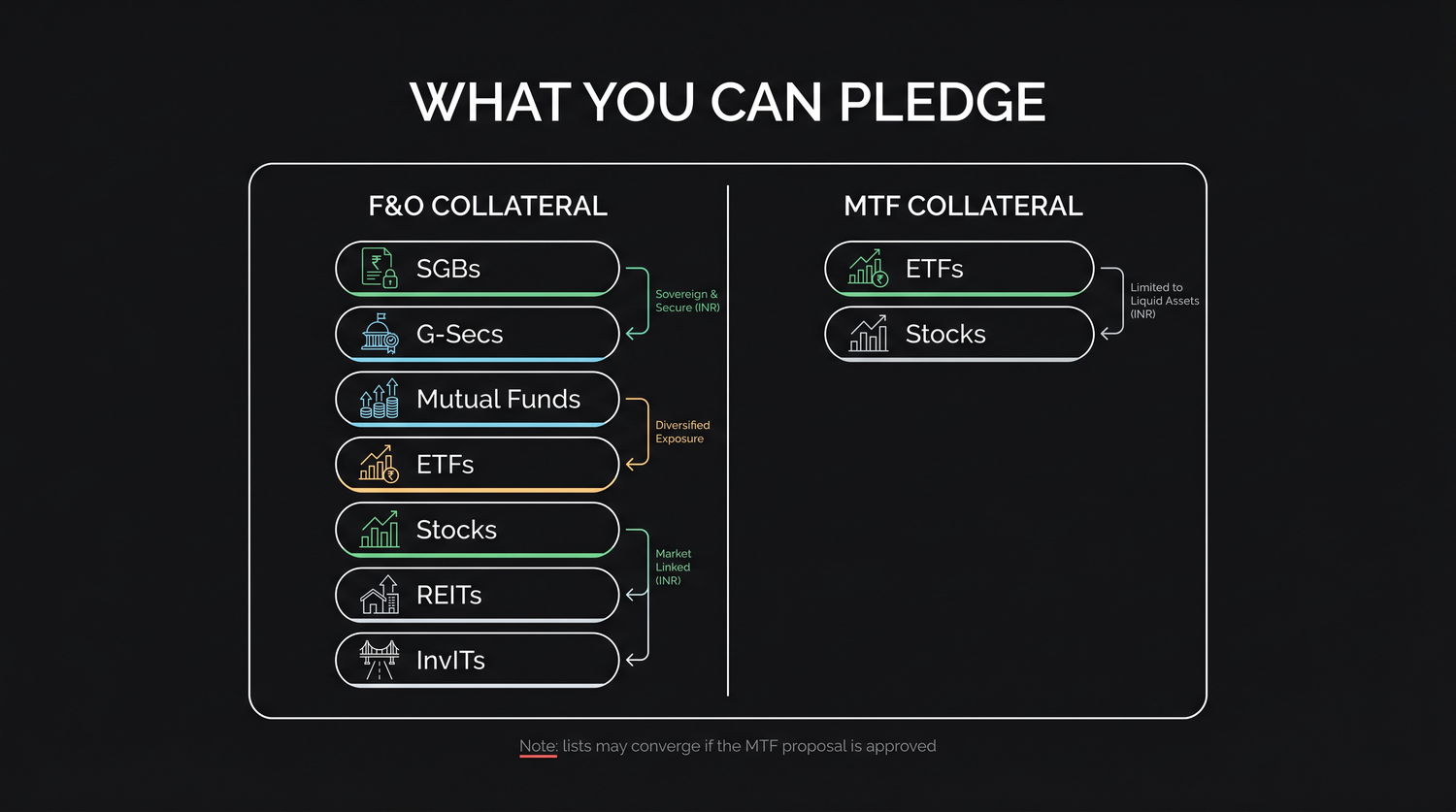

What counts as collateral for F&O

The list of assets you are allowed to pledge for futures and options is wide, which is part of what makes F&O margin so flexible. Approved collateral for F&O exposure includes:

- Sovereign Gold Bonds (SGBs)

- Government Securities (G-Secs)

- Mutual Funds

- ETFs

- Stocks (approved, liquid ones)

- REITs (real estate investment trusts)

- InvITs (infrastructure investment trusts)

A useful way to read that list is by haircut. The government-backed and fund instruments at the top, the SGBs, G-Secs and liquid funds, are stable and often count toward your cash-equivalent component with small haircuts. The market-priced instruments lower down, the stocks, REITs and InvITs, carry larger haircuts and sit on the non-cash side. Mixing the two lets you meet both the total margin and the cash-component rule from assets you already hold.

You want to run a defined-risk position that needs about Rs 1,50,000 of margin. Instead of freezing that in cash, you pledge roughly Rs 1,00,000 of a liquid fund, which is a cash-equivalent and gives close to its full value, covering the cash half, and you pledge about Rs 1,00,000 of stock, which after haircut adds roughly Rs 75,000 of non-cash margin. Between them the position is funded, your cash component is satisfied, and your idle assets are finally working for you.

A different list: MTF collateral

It is worth knowing one neighbouring rule, because beginners often confuse the two. The margin trading facility (MTF) is a separate thing from F&O. MTF lets you buy shares in the cash market with part-borrowed money, and it has its own, narrower list of acceptable collateral. For MTF exposure, only ETFs and Stocks are currently accepted.

So the same stock can be pledged in either world, but the broad menu of SGBs, G-Secs, mutual funds, REITs and InvITs that F&O accepts does not all carry over to MTF today.

This may not stay the case. A SEBI consultation paper on the margin trading facility has proposed changes, and if its provisions are approved in their current form, the collateral accepted for MTF could widen to match the F&O list, making the two effectively identical. Rules in this area evolve, so treat the exact lists as current practice rather than permanent law, and confirm the latest position before you pledge.

The practical takeaway

Collateral is the quiet efficiency that separates a thoughtful options trader from one who leaves money idle. The margin a short or futures position demands is real and is set by SPAN plus exposure, which the OpenAlgo margin calculator will show you before you trade. But you do not have to meet that margin with frozen cash. Pledge the assets you already own, respect the haircut and the cash-component rule, and the same capital can support your portfolio and your strategies at once. Used carelessly, leverage and thin cash buffers are how accounts blow up. Used with a sensible collateral mix and an honest eye on the cash half, margin becomes a tool you manage rather than a surprise that manages you. The next chapter takes pledging from idea to practice, with the haircut maths, two tricks to get the most from it, and the margin-call risk to respect.