Options Adjustments: Defending a Tested Trade

A strategy is rarely left untouched until expiry. Learn how to adjust a position when price tests it: rolling a strike up, down or out in time, converting a spread, adding a hedge leg, and the OpenAlgo workflow for closing and re-entering legs.

- ·Why adjust at all

- ·Rolling out in time

- ·Rolling a strike up or down

- ·Converting to a wider structure

- ·Adding a defensive leg

- ·When to adjust vs exit

Up to now every strategy in this course has been a thing you put on and hold to expiry. You chose a shape, you knew your maximum profit and loss the moment you entered, and you waited. But real markets rarely sit still while you wait. A short strangle that was comfortably out of the money on Monday can have NIFTY pressing against one of its strikes by Thursday. A bull put spread can watch the index drift toward its sold strike. When that happens you have a third choice beyond holding and panicking: you can adjust. Adjusting means changing the position while it is open, to defend it, to buy it time, or to re-center it on a new view. This chapter teaches the main adjustment moves and, just as important, when not to use them. No new numbers here, only the craft of managing a trade once it is live.

Why adjust at all

There are only three honest reasons to touch a position that is already on.

- To cut a loss into something smaller or more defined. A tested short leg might be turned into a defined-risk spread, so a runaway loss becomes a capped one.

- To buy time. If your view is still right but the move has not happened yet, you can push the trade into a later expiry and give it more room to work.

- To re-center on a new view. If NIFTY has moved and your read on it has genuinely changed, you can shift the structure to sit around the new price.

Notice what is not on that list: adjusting to avoid admitting you were wrong, or adding fresh risk in the hope of clawing back a loss. Those are the two ways adjustments destroy accounts. Every move below is useful only when it serves one of the three real reasons.

An adjustment is not a magic eraser. Every change you make has its own cost, its own new risk, and its own effect on the margin blocked. The goal of a good adjustment is to improve your position relative to your honest current view, not to refuse to take a loss. If the only reason you are adjusting is that you cannot bear to close a losing trade, the right move is almost always to close it.

Rolling out in time

The first move is the roll out, and it is the gentlest. You close the leg or the whole position in the near expiry and reopen the same structure in a later expiry. Because the further-dated options carry more time value, selling them usually brings in more credit than you spent buying back the near ones, so a roll out can often be done for a further net credit.

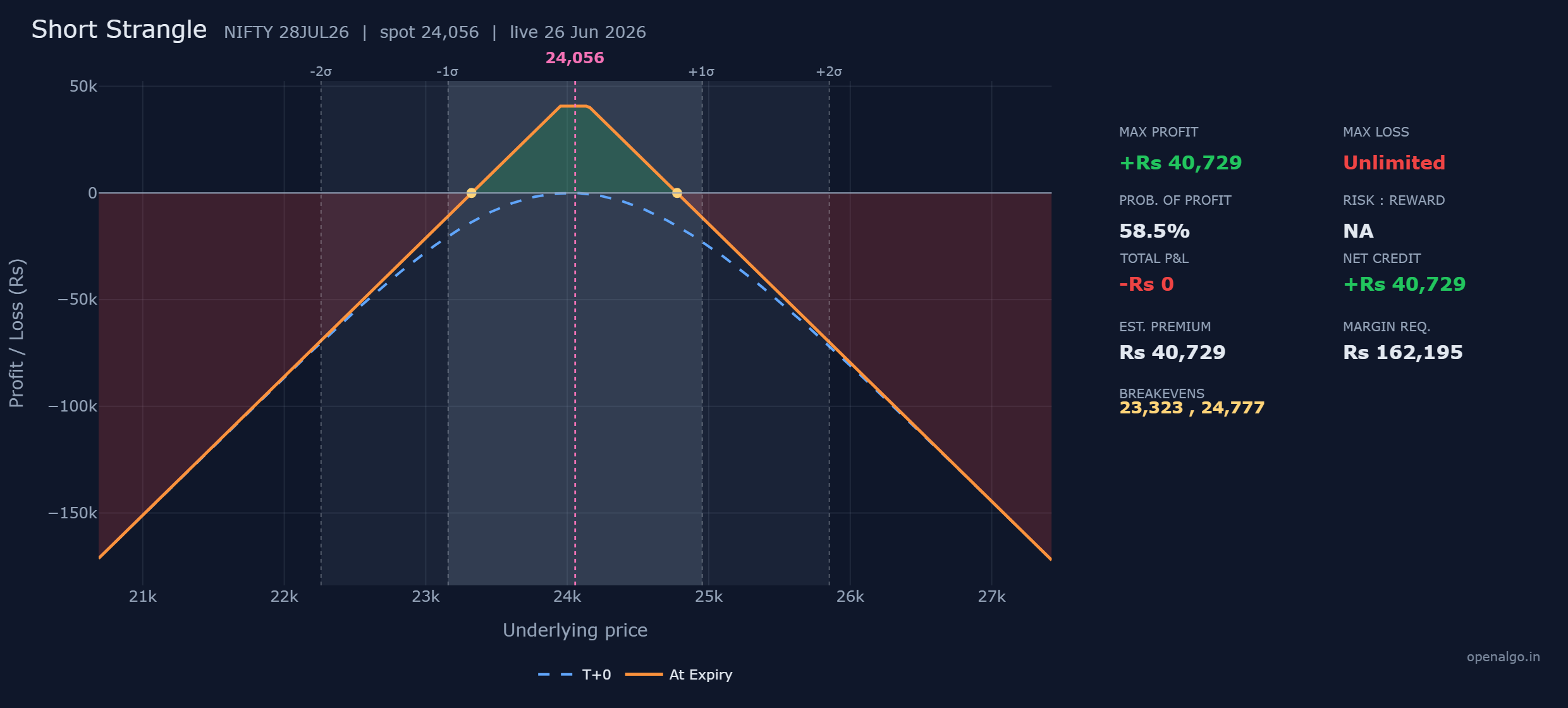

Take the short strangle above. Suppose NIFTY has spent two weeks drifting and is now leaning on the upper strike with little time left for the premium to decay. Rolling out means buying back both near-month legs and selling the same strangle in the next expiry. You give the trade another month for the market to settle back into the range, and you typically collect more premium for the privilege. The risk you are buying time against does not vanish, but you have refused to be forced into a loss simply because the calendar ran out.

Rolling a short position out in time keeps the open-ended risk alive for longer. The short strangle still has no ceiling on its loss above and a floor only at zero below, and pushing it into a later expiry means you are exposed to that risk for an extra month. Roll out only when your view that NIFTY stays in the range is genuinely intact, never as a reflex to delay a loss that the market is telling you is real.

Rolling a strike up or down

The second move keeps the same expiry but moves a tested strike away from the price. If NIFTY is pushing up against your sold 24,150 call, you can buy that call back and sell a new call at a higher strike, say one or two steps further out. The tested leg is now further from the action, so it is under less immediate pressure.

This buys breathing room, but it is rarely free. Selling a strike that is further from the money brings in less premium than the one you bought back, so rolling a strike up or down usually costs you part of your original credit, and it can widen the position's risk if you are not careful. The honest way to think about it: you are paying a little, in credit given back, to move your line of defence further from the price. When you do this, change one side at a time and re-read the whole payoff before you touch the other. Moving the tested call up while leaving the untested put in place often re-centers a strangle nicely, whereas moving both at once, in a hurry, is how a calm defensive adjustment quietly turns into a brand new, larger position you never meant to hold.

Reshaping the structure

The third family of moves changes the shape of the trade itself, usually to convert open risk into defined risk.

- Widen a spread. A bull put spread that is being tested can be rolled down to a lower pair of strikes, giving the index more room to fall before the spread is fully in the money. The structure stays defined-risk throughout.

- Add the opposite side to make an iron condor. If you are running a single credit spread and the market has moved in your favour on one side, you can sell a spread on the other side too. A bull put spread plus a bear call spread is an iron condor, and adding the second spread brings in more credit and widens your profitable zone. Do this only when the new side is genuinely far from the price, so you are collecting premium for risk you are comfortable taking, not doubling your exposure.

The thread running through all of these is that you are trying to keep, or restore, defined risk. Widening a spread keeps it bounded. Turning a spread into an iron condor keeps both sides bounded. These are the adjustments a beginner can make safely, because the worst case stays a known number at every step.

Capping a runaway short

The most important defensive move of all is turning an open-ended risk into a closed one. If you are short a naked leg, a sold call or a sold put with no protection, and the market is running against it, you can add a long leg further out to cap the loss. Buy a call above your sold call, or a put below your sold put, and the naked short becomes a credit spread with a known maximum loss.

This is the one adjustment that genuinely reduces risk rather than merely shifting it. You give back some of your credit to buy the protective wing, but in exchange the unlimited tail is gone, replaced by a defined number you can actually survive.

Capping a runaway short by buying a protective wing is the right move. Adding more naked short legs to collect extra premium and average down your loss is the wrong one, and it is the single most common way beginners turn a manageable loss into an account-ending one. The rule is simple: an adjustment may reduce your risk or hold it steady, but it must never increase the open-ended risk of a position that is already losing. Do not add risk to rescue a loser.

Adjusting honestly in OpenAlgo

OpenAlgo's strategy builder lets you model every one of these moves before you commit a rupee, so you can see exactly what the adjustment does to your nine numbers. The workflow is deliberately honest.

- Mark the closed leg with an exit price. When you buy back a tested short or close a near-month leg, record the price you paid to close it. That locks in the realised gain or loss on that leg.

- Add the new leg. Sell the rolled strike, open the later expiry, or buy the protective wing as a fresh leg in the structure.

- Re-check the metrics and the margin. Read the new maximum profit, the new maximum loss, the new breakevens, and above all the new margin requirement. An adjustment that fixes your risk but doubles your blocked margin may not be one your account can carry.

The reason to re-check the margin every time is that adjustments often change it sharply. Capping a naked short with a protective wing usually cuts the margin, because the exchange now sees a defined-risk spread instead of an open obligation. Rolling a short out in time, or adding a second short side, usually raises it. Always confirm the new margin fits comfortably inside your account before you place the adjusting orders, and rehearse the whole sequence in sandbox trading (analyzer mode in OpenAlgo) first.

Adjust or simply exit

The hardest judgement is knowing when to defend a trade and when to close it and move on. The cleanest test is to ask one question: is the thesis still valid?

- If your original reason for the trade still holds, the move against you is just noise, and the position is still defined-risk or can be made so, then adjust. You are managing a good trade through a rough patch.

- If the reason you entered has broken, the market has clearly chosen a direction against you, or defending the trade would mean adding risk you cannot afford, then exit. Take the loss while it is small and keep your capital for the next setup.

Two tested short strangles, two different answers. In the first, NIFTY has wandered toward your call strike on thin, directionless trading, your view that it stays range-bound is intact, and you have plenty of margin: roll the tested call up and out, collect a little more credit, and give it room. In the second, a strong trend has set in, NIFTY has broken cleanly above your strike with conviction, and the only way to defend is to keep selling into the move: there is nothing to defend. Close it, accept the defined loss, and stop trading against the trend.

Adjusting well is what separates a trader who survives a bad month from one who does not. Hold to your three honest reasons, keep every move inside defined risk, re-check the margin each time, and never add danger to a position that is already losing. With that discipline, the strategies in this course become not just shapes you put on, but trades you can steer.