Synthetics and the Covered Call

Options can copy a future, and pair with one. Learn the long and short synthetic future (a call plus a put that mimics a future) and the covered call (a holding plus a sold call for income).

- ·The long synthetic future

- ·The short synthetic future

- ·Why they equal a future

- ·The covered call

- ·Earning income on a holding

- ·The cap on the upside

There is a quiet piece of options arithmetic that surprises every beginner the first time they see it. A bought call and a sold put, struck at the same price, add up to something that is not curved at all. They make a straight line that rises and falls exactly like a futures position. This relationship, that options can be assembled into a future and a future can be taken apart into options, is one of the most useful ideas in the whole subject. In this chapter we put the long synthetic future and the short synthetic future side by side, then use the same building-block thinking to construct the covered call, the income trade that sits on top of a holding you already own. All figures use real NIFTY option data captured on 26 June 2026, spot 24,056, ATM strike 24,050, lot 65, expiry 28 July 2026.

The one-line idea

A synthetic future is a long future rebuilt from two options at the same strike. Buy the call and sell the put and you own all of a future's upside and all of its downside, glued into a single straight diagonal line. Sell the call and buy the put and you have built the mirror, a short future. The view is the same blunt directional bet a future expresses, but assembled from the options you already understand.

A long call and a short put at the same strike make a long future. A short call and a long put at the same strike make a short future. This is the parity relationship at the heart of options: a future is just a call and a put bolted together, and any one of the three can be rebuilt from the other two. Recognising these straight-line shapes inside more complex structures is one of the most powerful reading skills you can develop.

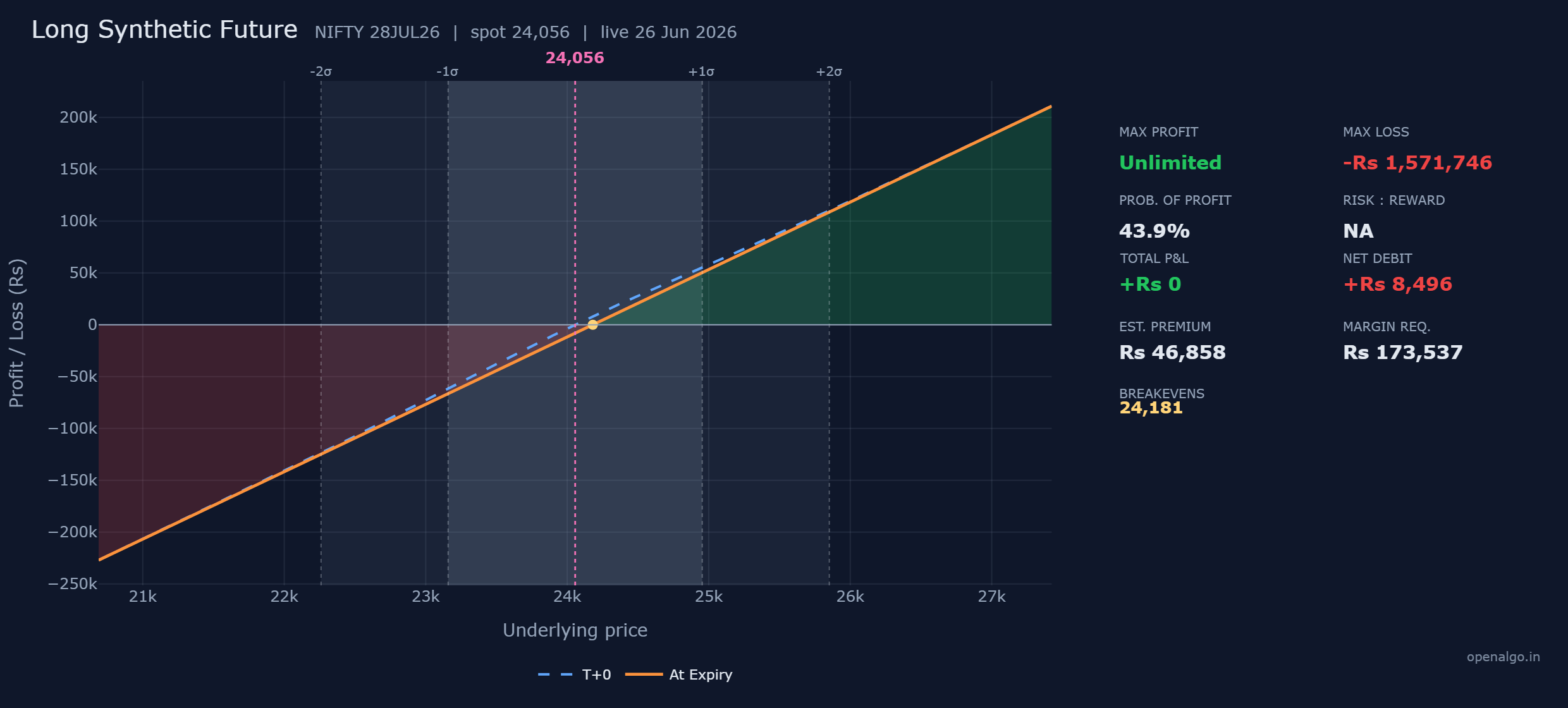

The long synthetic future, rupee by rupee

You met this shape briefly among the bullish strategies. Here is what it is made of, one bought call and one sold put, both at the at-the-money strike.

| Leg | Action | Strike | Premium per share | Cash flow per lot of 65 |

|---|---|---|---|---|

| 1 | Buy call | 24,050 | 425.8 paid | Rs 27,677 out |

| 2 | Sell put | 24,050 | 295.1 received | plus Rs 19,182 in |

| Net debit | about Rs 8,496 out |

The bought call hands you all of a future's upside. The sold put hands you all of a future's downside. Glue them together and the curves cancel into a single diagonal line that tracks NIFTY point for point in both directions. The call costs 425.8 and the put pays you 295.1, so you part with the difference, 130.7 points per share, which is a net debit of about Rs 8,496 per lot.

The three numbers, and where they come from

Breakeven is 24,181. At any closing price, the call's intrinsic value minus the put's intrinsic value is simply NIFTY minus the 24,050 strike. You paid 130.7 points to hold that, so you turn profitable once NIFTY clears 24,050 plus 130.7, which is 24,181.

Maximum profit is Unlimited. Above the breakeven the line rises point for point with no ceiling, just like a long future.

Maximum loss is Rs 1,571,746. Below the breakeven the line falls rupee for rupee. The floor is not really a floor, it is just that NIFTY cannot drop below zero, and if it fell all the way the loss would reach about Rs 1,571,746.

| Number | How it is built | This trade |

|---|---|---|

| Breakeven | strike plus the net debit in points | 24,050 plus 130.7 equals 24,181 |

| Max profit | rises point for point, no ceiling | Unlimited |

| Max loss | full fall to zero, finite but huge | Rs 1,571,746 |

Walking the outcomes at expiry

Settle the long synthetic at five closing prices, per lot of 65. The bought call is worth its intrinsic value, the sold put is a liability worth its intrinsic value, and the straight line is plain in the final column.

| NIFTY at expiry | 24,050 call you bought | 24,050 put you sold | Net profit or loss |

|---|---|---|---|

| 22,000 | expires worthless | worth 2,050 against you | minus Rs 141,746 |

| 24,050 | expires worthless | expires worthless | minus Rs 8,496 (the debit) |

| 24,181 | worth 131 | expires worthless | about Rs 0 (breakeven) |

| 25,000 | worth 950 | expires worthless | plus Rs 53,255 |

| 26,000 | worth 1,950 | expires worthless | plus Rs 118,255 |

There is nothing to interpret beyond the straight line, and that is the point. Above 24,181 you gain point for point with no ceiling. Below it you lose point for point, and a deep fall toward zero is what builds the Rs 1,571,746 worst case. The blue T+0 line sits almost on top of the orange one, because a synthetic future holds almost no time value to decay away, so time barely moves this position. Its probability of profit is about 44 percent, the market's read on NIFTY clearing the 24,181 breakeven by expiry.

The long synthetic future behaves exactly like a long NIFTY future, so its risk is two-sided and very large. The maximum loss is about Rs 1,571,746 if NIFTY collapses toward zero, the sold put is a naked short leg, and the exchange blocks a heavy margin of about Rs 173,537. There is no protective floor anywhere in this structure. Treat it with the same respect you would give a futures position, never as a gentler options trade.

The short synthetic future

Flip both legs and you get the mirror image. Sell the call, buy the put, and you have built a short future from two options.

| Leg | Action | Strike | Premium per share | Cash flow per lot of 65 |

|---|---|---|---|---|

| 1 | Sell call | 24,050 | 425.8 received | plus Rs 27,677 in |

| 2 | Buy put | 24,050 | 295.1 paid | Rs 19,182 out |

| Net credit | about Rs 8,496 in |

| Metric | Value |

|---|---|

| Max profit | Rs 1,571,746 |

| Max loss | Unlimited |

| Breakeven | 24,181 |

| Probability of profit | about 56 percent |

| Risk to reward | NA |

| Net credit | about Rs 8,496 |

| Margin required | Rs 169,046 |

| Total P&L now | about Rs 0 |

Read the short synthetic as the long synthetic flipped top to bottom. Below the breakeven of 24,181 the line falls into profit, which on the downside is large but finite, because NIFTY cannot drop below zero, hence the maximum profit of Rs 1,571,746. Above the breakeven the line rises into loss with no limit at all. Run the same five closing prices as the long synthetic and simply reverse the sign of every net figure: where the long version loses Rs 141,746 at 22,000, the short version gains it, and where the long version gains Rs 118,255 at 26,000, the short version loses it without any ceiling.

The short synthetic future has UNLIMITED risk to the upside. The sold call is a naked short leg, and if NIFTY rallies hard the loss grows without any ceiling, which is why the builder prints the maximum loss as Unlimited and the exchange blocks about Rs 169,046 of margin. A small credit of Rs 8,496 in no way reflects the danger you are carrying. This is a short future in disguise and must be managed as one.

The covered call

The covered call is not a template in the strategy builder, because one of its legs is something you already hold rather than an option you add. But it is built from the same parts thinking, so it belongs here. Picture a trader holding a long NIFTY position, say through a future, who is content with a steady, sideways to mildly higher market. To earn income from that holding, they sell a call above the current price, here the 24,150 call, and pocket the premium of 370.1 per share, about Rs 24,057 for the lot.

The two pieces work like this.

- The long NIFTY future gives the usual point-for-point exposure, gaining as NIFTY rises and losing as it falls.

- The sold 24,150 call brings in premium straight away. As long as NIFTY finishes below 24,150 by expiry, that call expires worthless and the premium is pure income on top of the holding.

The result is a position that earns a little extra every month the market stays calm, in exchange for one clear concession: your upside is capped. If NIFTY rallies past 24,150, every further point your future gains is matched by a point the sold call loses, so above the strike your profit stops growing. Your best case is the move up to 24,150 plus the premium you collected.

Look closely at the covered call's payoff and you will recognise it. A long future plus a short call produces the very same bent line as a short put: limited, capped profit on the upside and a long, sloping loss on the downside. The covered call is a synthetic short put. This is the parity idea again, and it explains why a covered call is an income trade and not a growth trade. You are selling away your upside in return for premium today.

The covered call suits an investor who wants to keep a holding and squeeze a yield from it during quiet stretches, not a trader chasing a big rally. The premium also gives a small cushion on the way down, because the income you collected offsets the first part of any fall. But that cushion is thin.

A covered call does not protect your downside. Your long NIFTY future can still lose heavily if the market falls, and all the sold call gives you is the small premium as a first cushion. Selling a call to earn income on a holding you would not otherwise want to keep is a mistake, because you have capped the only good outcome while leaving the bad one almost fully open. Use the covered call only on a position you are genuinely happy to hold, and size it for a real fall, not for the calm you are hoping for.

Three ways to hold a directional view

| Position | Built from | Shape | Risk |

|---|---|---|---|

| Long synthetic future | Long call, short put | Straight line up | Large two-sided, naked put |

| Short synthetic future | Short call, long put | Straight line down | Unlimited upside, naked call |

| Covered call | Long holding, short call | Capped upside, full downside | Full downside on the holding |

The synthetics are the purest expression of a directional view, a straight line, no time decay to fight, and the full risk of a future. The covered call is the gentlest: it gives up the open-ended upside in return for a steady premium, and it makes sense only when you already own and want the underlying. None of the three is defined-risk in the way a spread is, so for a beginner they sit a clear step beyond the bounded structures of earlier chapters. Build the long synthetic beside a short straddle in the strategy builder and watch both block well over a lakh and a half of margin: the straight-line synthetic is not a shortcut around the risk of a future, it is that risk, rebuilt from two options. Rehearse any of these in sandbox trading (analyzer mode in OpenAlgo) before you commit real money.

You have now seen how options reassemble into futures and how a sold call turns a holding into an income trade. These are the structures with real, futures-grade risk, the opposite end of the spectrum from the defined-risk spreads. In the chapters ahead we turn from building positions to defending them, starting with the question every trader eventually faces, what do you do when a trade goes against you.

Key takeaways

- A synthetic future rebuilds a future from two options: a long call plus a short put is a long future, a short call plus a long put is a short future.

- The long synthetic costs a net debit of about Rs 8,496, breaks even at 24,181, rises without limit above it, and falls toward a Rs 1,571,746 loss below it.

- The short synthetic is its mirror, a small credit with a finite Rs 1,571,746 best case on the downside and an unlimited loss on a rally.

- Both carry futures-grade, two-sided risk, block well over Rs 1.6 lakh of margin, and hold almost no time value, so the T+0 and expiry lines overlap.

- The covered call is a long holding plus a sold higher call: steady premium income, a capped upside, and a still-large downside, which makes it a synthetic short put.

- None of these are defined-risk, so they sit a step beyond spreads for a beginner and must be sized for a real adverse move, never for the calm you hope for.