Margins and Margin Penalties

The exchange checks your margin at random moments through the day, and a shortfall costs you a penalty. Learn the minimum margin rule, the peak-margin checks, the penalty slabs, and the everyday situations that quietly trigger them.

- ·The minimum margin rule

- ·Peak margin and the random checks

- ·The penalty slabs

- ·Upfront vs non-upfront shortfalls

- ·Why a short or unhedge raises margin

- ·Keeping a margin buffer

You now know how much margin a position blocks and how to fund it by pledging. The last piece of the margin story is what happens when you fall short. The exchange does not just check your margin once and forget about it. It checks repeatedly, at random, through the day, and every time you are short of the required minimum it charges a penalty. Understanding exactly how those checks work, and the everyday situations that trigger them, is what separates a trader who keeps their returns from one who quietly bleeds them away in fines. This chapter is about staying on the right side of the margin rules.

The minimum margin you must always hold

Because a leveraged position can lose more than the cash in your account, regulators require your broker to collect a minimum margin on every such trade, and that minimum is not optional. The amount is defined by the exchange, not the broker.

- For equity, the minimum is called VAR plus ELM (value at risk plus an extreme loss margin).

- For F&O, it is the SPAN plus exposure you already know.

Since the peak-margin rules came in, this minimum is uniform across the whole industry. A broker can no longer offer extra intraday leverage as a selling point. Whatever you trade, the same minimum margin applies, and you are expected to have it in your account.

The minimum margin is set by the exchange and is the same everywhere. For F&O it is SPAN plus exposure, for equity it is VAR plus ELM. You must hold at least this amount against any leveraged position, and there is no longer any legal way for a broker to let you hold less.

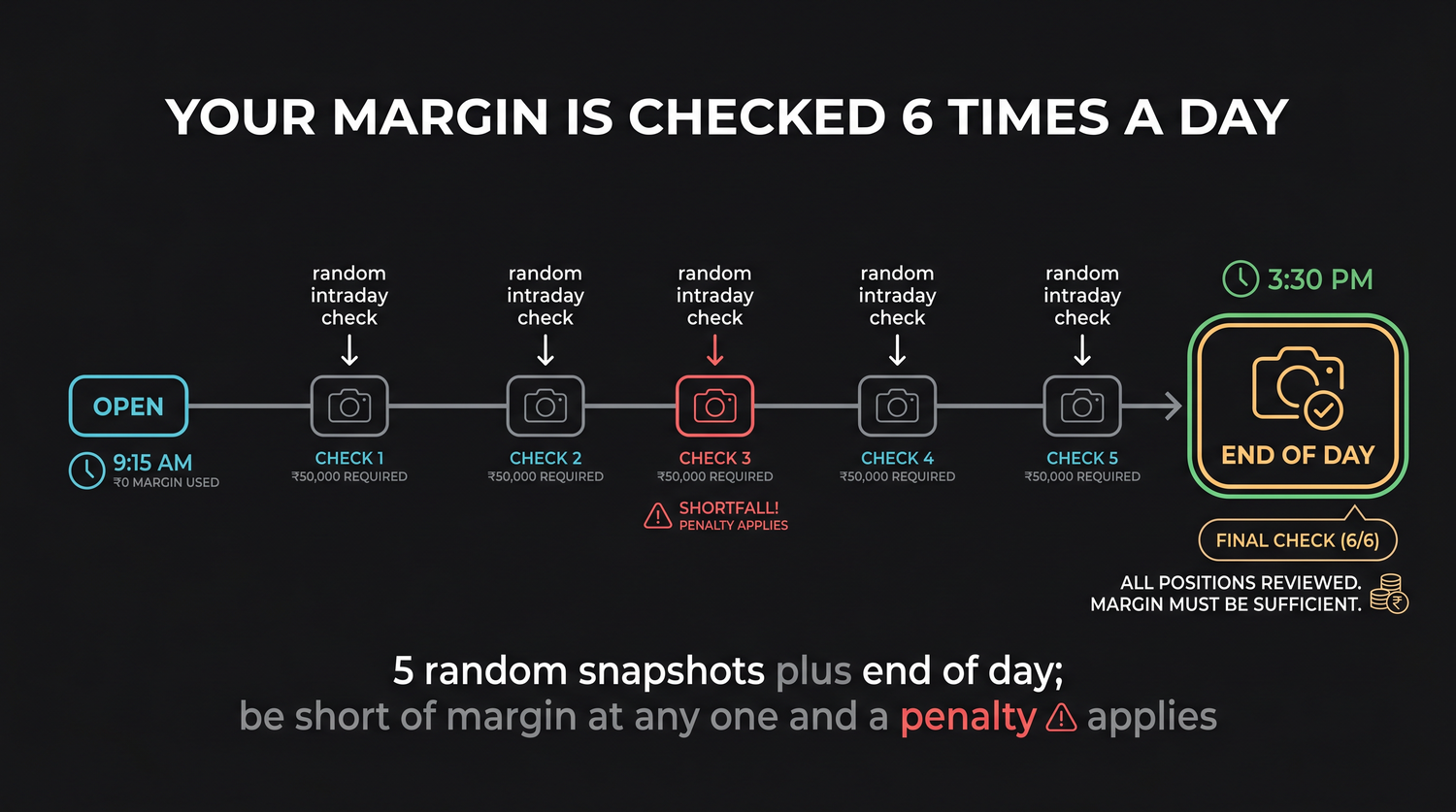

Peak margin, the random checks

Here is the part that surprises most beginners. The exchange does not only check your margin at the end of the day. Under the peak-margin system, the clearing corporation takes multiple random snapshots of every trader's positions and margins during the trading day, plus a check at the end of the day. You do not know when the intraday snapshots will fall, and the exact number is set by the exchange rather than fixed forever.

At each of those moments, you must have the full required margin in your account. If you are short at even one snapshot, the shortfall at that moment is recorded, whether or not you had enough margin for the rest of the day.

This is why a trader cannot simply top up before the close and assume they are safe. The random snapshots mean the only reliable way to avoid a shortfall is to hold the full margin throughout the day, not just at convenient moments.

The penalty slabs

When a shortfall is found, at any snapshot or at the end of the day, a penalty is charged on the amount you were short by. The rates are tiered.

| Shortfall on the day | Penalty on the shortfall |

|---|---|

| Less than Rs 1 lakh | 0.5 percent |

| Rs 1 lakh or more | 1 percent |

| More than three times in a month | up to 5 percent |

So a shortfall of Rs 50,000 attracts a penalty of Rs 250, while a shortfall of Rs 2,00,000 attracts Rs 2,000. Fall short repeatedly, more than three times in a single month, and the rate can climb to as much as 5 percent. These penalties are collected by the exchange and deposited into a core settlement guarantee fund. They are not a fee your broker invents, they are a regulatory charge, and they come straight out of your returns.

A margin penalty is charged on the shortfall, not on your whole position, but it adds up fast. Repeated small shortfalls quietly erode a trading account, and crossing three instances in a month pushes the rate higher. The cheapest penalty is the one you never trigger by always holding a margin buffer.

Upfront versus non-upfront shortfalls

Not all shortfalls are treated the same way, and the difference decides who pays.

- An upfront shortfall is not having enough margin at the moment you enter a position, or having the required margin rise above what you hold after you are already in. Upfront penalties cannot be passed on to you by the broker, so the broker bears them. The flip side is that brokers will not let you enter a trade without the upfront margin in place.

- A non-upfront shortfall is a margin that becomes due after you have entered. The clearest example is a mark-to-market loss on a futures position, where you have until the next day, T plus one, to bring in the funds. Expiry-week delivery margins and other ad-hoc margins on stock derivatives also fall here. Non-upfront penalties can be passed on to you.

The practical takeaway is not to memorise which bucket a penalty falls in, but to realise that a margin shortfall is always your problem to avoid. Whether the broker bears the fine or passes it on, a shortfall means your positions are under-margined and at risk of being closed for you.

The everyday situations that trip traders

Penalties are rarely the result of reckless over-leveraging. They usually come from ordinary situations where the required margin quietly rises after you are already in a trade. Three are worth knowing.

- A short option moving against you. When you sell an option, there is no daily mark-to-market settlement like futures. Instead, as the position moves against you, the margin required simply goes up. If you do not have the extra margin, that is treated as an upfront shortfall. This is why a short seller must always keep spare margin, not just the amount needed on day one.

- Closing a hedge leg. A hedged position needs far less margin than a naked one, because the exchange can see the risk is capped. Picture a futures position protected by a bought put, which together might need only a small margin. Close the put and the futures position is suddenly naked, so its margin jumps back up immediately. If you do not have that larger amount, you are in shortfall the instant the hedge is gone.

- A jump in volatility. When markets turn volatile, the exchange can raise SPAN and exposure margins across the board. A position that was fully margined yesterday can be short today through no action of your own.

Always remove the risk-reducing leg of a strategy last, never first. If you unwind an iron condor or a hedged future by closing the protective leg before the risky one, the margin on what remains spikes and you can land in a shortfall in the gap between the two orders. Close the naked risk first, the protection last.

Staying penalty-free

None of this is hard to avoid, it just takes a habit of leaving room. The traders who never pay penalties are simply the ones who never trade right up to their last rupee of margin.

- Keep a margin buffer. Run the OpenAlgo margin calculator before you trade and confirm you hold comfortably more than the requirement, so an intraday increase does not tip you into shortfall.

- Fund futures mark-to-market losses by the next day, before the T plus one deadline.

- When you are short options, watch the rising margin as the position moves against you, and keep spare funds for it.

- Unwind multi-leg strategies in the safe order, naked leg first, hedge last.

Margin penalties are almost entirely avoidable. They are not punishment for trading, they are the cost of being under-margined when one of the random checks lands. Hold a buffer, fund futures losses on time, and unwind hedges in the right order, and you will simply never meet them.

You now understand margin from every side, what it is, how to fund it through collateral and pledging, and how to stay clear of penalties. That completes the practical machinery behind every strategy in this course. In the final chapter we step back from the mechanics and answer the question all of it was for, faced with a real view and a real account, which strategy do you actually choose, and how do you manage it once it is on.