Advance Tax and the Dates You Cannot Miss

Tax is not a once-a-year job. Learn advance tax (paying as you earn), the quarterly dates, the filing deadlines for AY 2026-27, and why missing the due date quietly costs you your right to carry losses forward.

- ·What advance tax is

- ·The four advance-tax dates

- ·Interest if you underpay

- ·Filing due dates for AY 2026-27

- ·Audit vs non-audit deadlines

- ·Why on-time filing protects you

Most people imagine tax as one big payment, made once a year, after the year is over. For a salaried person that is roughly how it feels, because the employer quietly deducts a slice every month. But traders and investors are often on their own, and the tax department does not actually wait until the year ends to collect. It wants its share through the year, in instalments, as you earn. This system is called advance tax, and missing it is one of the most common and most avoidable ways traders end up paying extra.

The idea behind advance tax is fair when you think about it. The government runs all year, so it asks you to pay tax all year too, roughly in step with when you earn the income. If you wait and dump the whole amount at the end, you have effectively held on to money that was due earlier, and the law charges interest for that delay. Understanding the four dates, and one filing deadline, is enough to stay completely clear of this trap.

When advance tax applies to you

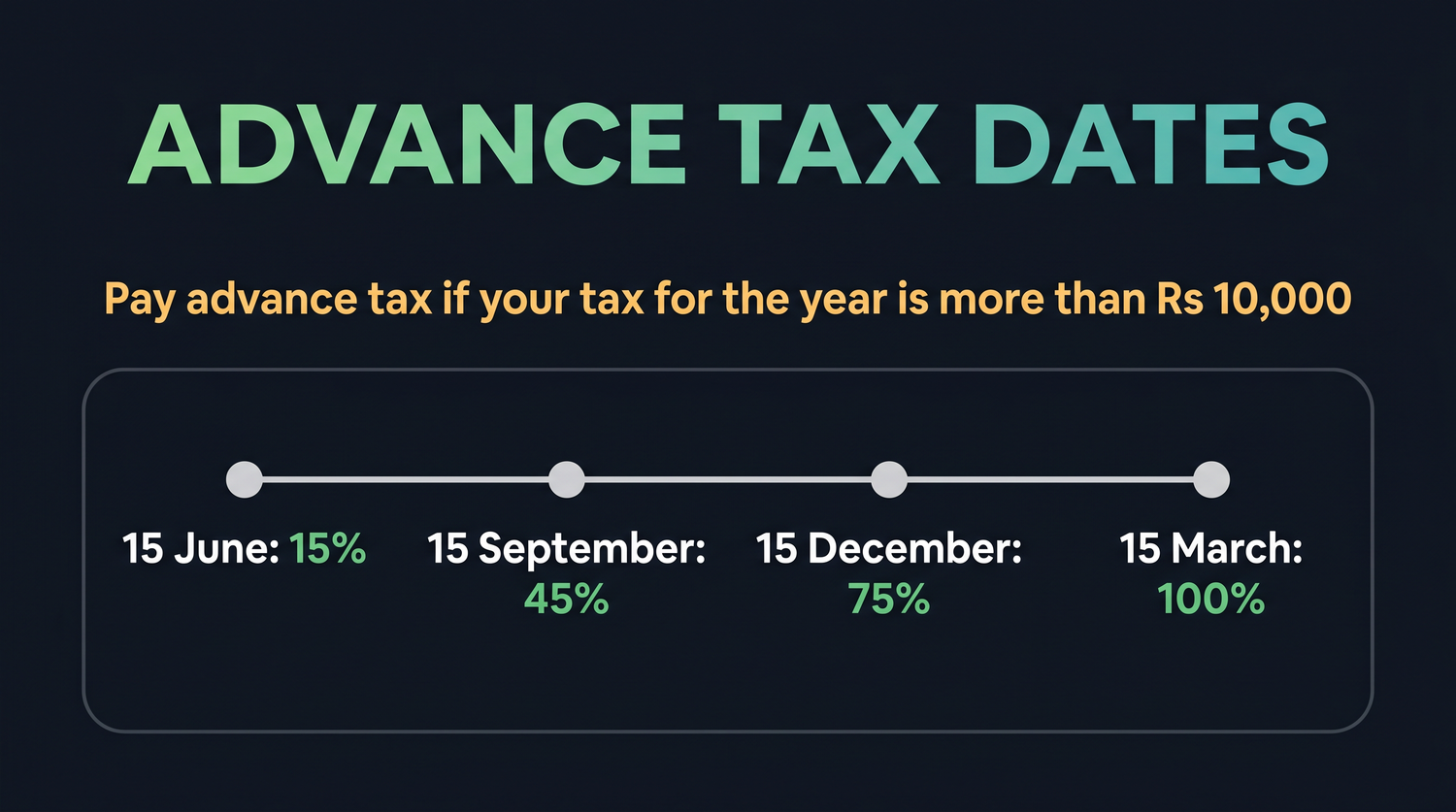

The rule that decides whether you need to bother with advance tax at all is refreshingly simple. If your total tax for the year, after subtracting any tax already deducted at source, is more than Rs 10,000, you are expected to pay it in advance instalments through the year.

For a pure salaried person this rarely bites, because the employer already deducts tax each month. But a trader's profits usually arrive with no tax taken out. A good year in futures and options, intraday, or capital gains can easily push your tax past Rs 10,000, and the moment it does, advance tax becomes your responsibility.

This catches many first-time traders by surprise. They picture tax as a single event in July, after the year has closed, and are startled to learn that the law expected money from them back in June, September, and December of the previous year. Nobody sends you a bill or a reminder for advance tax. The responsibility to estimate and pay sits entirely with you. That is why the four dates are worth committing to memory, because the only person watching the calendar is you.

The trigger is Rs 10,000. If your net tax for the year, after any tax already deducted at source, is expected to exceed Rs 10,000, you must pay it through the year in advance instalments rather than all at once at the end.

The four dates and how much by each

Advance tax is not one payment. It is spread across four points in the financial year, and each date carries a target. The target is cumulative, meaning it is the total you should have paid by that point, not an extra amount each time. For the financial year 2025-26, which is assessment year 2026-27, the dates and the cumulative share of your total tax are as follows.

| Pay by | Cumulative advance tax due |

|---|---|

| 15 June 2025 | 15% of your total tax |

| 15 September 2025 | 45% of your total tax |

| 15 December 2025 | 75% of your total tax |

| 15 March 2026 | 100% of your total tax |

Read the percentages as a running total. By 15 June you should have paid 15%. By 15 September the cumulative figure rises to 45%, so the second instalment is whatever takes you from 15% up to 45%. By 15 December you should be at 75%, and by 15 March the full 100% should be paid. Each instalment simply tops you up to the new cumulative mark.

The percentages are cumulative, not four equal slices. By 15 September the target is 45% in total, which means the September instalment is 45% minus the 15% you already paid in June, that is 30% of your total tax.

A worked example with real rupees

Numbers make this far clearer than words. Carry forward Meera from the regime chapter, whose tax for the year worked out to Rs 1,20,000 before cess. To keep this clean, let us say her total tax for the year is Rs 1,20,000 and none of it was deducted at source, so the whole amount is hers to pay in advance.

Apply the four cumulative targets to her Rs 1,20,000.

| Pay by | Cumulative target | Cumulative amount | Instalment that date |

|---|---|---|---|

| 15 June 2025 | 15% | Rs 18,000 | Rs 18,000 |

| 15 September 2025 | 45% | Rs 54,000 | Rs 36,000 |

| 15 December 2025 | 75% | Rs 90,000 | Rs 36,000 |

| 15 March 2026 | 100% | Rs 1,20,000 | Rs 30,000 |

Walk through it. By 15 June she pays 15% of 1,20,000, which is Rs 18,000. By 15 September her cumulative target is 45%, that is Rs 54,000, so she tops up by 54,000 minus 18,000, which is Rs 36,000. By 15 December the target is 75%, that is Rs 90,000, so she adds 90,000 minus 54,000, which is another Rs 36,000. By 15 March she must reach the full Rs 1,20,000, so she pays the final 1,20,000 minus 90,000, which is Rs 30,000. Pay on these dates and she owes no interest for delay.

Meera's total tax for the year is Rs 1,20,000, none deducted at source. Her advance tax instalments are Rs 18,000 by 15 June, Rs 36,000 by 15 September, Rs 36,000 by 15 December, and Rs 30,000 by 15 March, which add back to Rs 1,20,000. Paying on time on each date keeps her completely clear of interest for late payment.

The honest difficulty for traders is that profits are unpredictable. You cannot know in June what December will bring. The practical answer is to estimate as best you can each quarter using your broker's profit and loss report, pay advance tax on the income earned so far, and adjust at the next date. A reasonable estimate, revised each quarter, is far better than ignoring the dates entirely.

You do not need a perfect forecast. Pull your broker's profit and loss figure before each due date, estimate the tax on what you have earned so far, and pay that. Adjust up or down at the next date. Paying a fair estimate on time beats paying nothing and owing interest later.

On-time filing protects your losses

Advance tax handles money owed during the year. A second deadline, the date for filing your return, protects something just as valuable, your right to carry losses forward.

Recall from earlier chapters that a futures and options loss, once reported, can be carried forward for up to eight assessment years to set off against future business income. There is a strict condition attached. You only keep that carry-forward right if you file your return by the original due date. For most non-audit individuals this due date falls on 31 July following the financial year, so 31 July 2026 for assessment year 2026-27, though dates can be extended, so confirm the latest each year.

File even one day late and you can still report the loss, but you forfeit the right to carry it forward. The loss is then wasted. After a tough trading year, that carry-forward is often the only silver lining, and it would be a shame to throw it away by missing a date.

A late return keeps you from carrying losses forward. You may report the loss, but you lose the right to set it off against future profits. After a losing year, filing by the due date is what preserves the one benefit that loss can still give you.

So two clocks run through a trader's year. One is advance tax, paid in four instalments by 15 June, 15 September, 15 December, and 15 March, which keeps interest off your back. The other is the return filing deadline, which protects your loss carry-forward. Keep both in view and the mechanical side of tax becomes routine rather than stressful. Set calendar reminders for the four advance tax dates and the filing date, and you have removed most of the penalties that catch traders off guard.

In short, two deadlines define a trader's tax year. The four advance tax dates protect you from interest, and the return filing date protects your loss carry-forward. Both are easy to meet once they are sitting in your calendar, and expensive to miss when they are not. Treat them as fixed appointments, the way you would a loan instalment, and the penalty side of tax stops being a worry.

This chapter is for educational purposes only and is not tax advice. Due dates and thresholds can change from year to year, so please confirm the current dates and your own position with a qualified chartered accountant before you file.