Old Regime or New: Which Tax Slabs Apply

The new tax regime is now the default. Learn the AY 2026-27 slab rates in plain numbers, the rebate that can make income up to a point tax-free, when the old regime still wins, and the form you must not forget if you switch.

- ·The new regime is the default

- ·AY 2026-27 slab rates

- ·The Section 87A rebate

- ·Surcharge and cess

- ·When to keep the old regime

- ·Form 10-IEA, the easy miss

Two traders earn exactly the same income this year, yet one pays more tax than the other. Nothing about their trading was different. The only difference was a choice they made, often without realising it, about which tax regime they sat under. India now runs two parallel systems for taxing your income, an older one and a newer one, and the rules for picking between them quietly decide how much you keep.

The good news is that for most people the decision has become simpler than it used to be. The new regime is now the default. If you do nothing, you are in it. For a great many traders and investors, that default is also the better deal, because the new regime offers wider slabs and a generous rebate. Still, you should understand both, because a few situations make the old regime worth a second look, and switching has its own rule book.

The new regime is the default

Start with the most important fact. For the financial year 2025-26, which is assessment year 2026-27, the new tax regime applies automatically unless you actively choose otherwise. You do not opt in. You are already in.

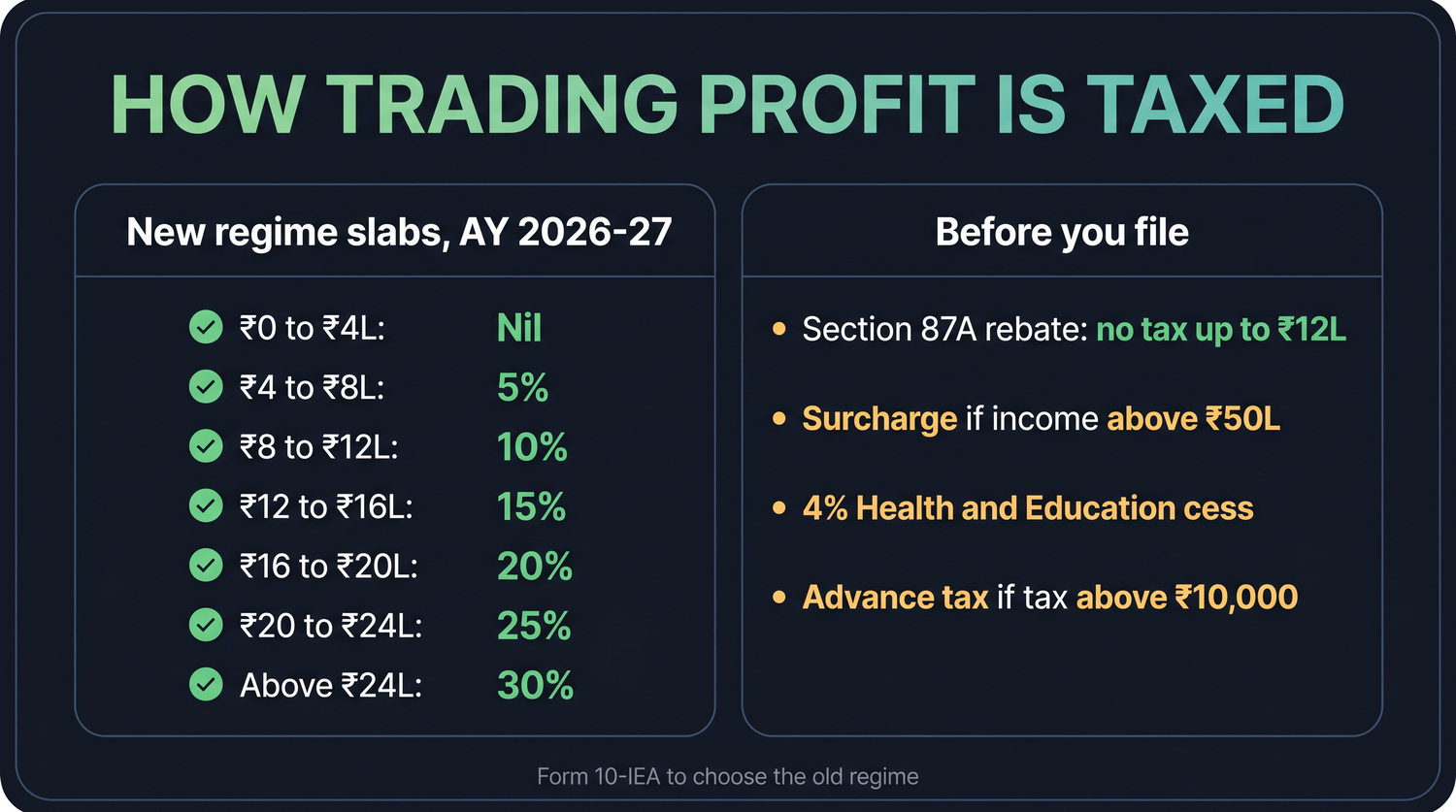

The new regime keeps your tax simple by spreading income across several slabs, each taxed at a rising rate. You pay nothing on the first slab, a low rate on the next, and so on, so only the portion of income inside each band is taxed at that band's rate. Here is the full slab table as things stand for assessment year 2026-27.

| Taxable income | Tax rate |

|---|---|

| Up to Rs 4 lakh | Nil |

| Rs 4 lakh to 8 lakh | 5% |

| Rs 8 lakh to 12 lakh | 10% |

| Rs 12 lakh to 16 lakh | 15% |

| Rs 16 lakh to 20 lakh | 20% |

| Rs 20 lakh to 24 lakh | 25% |

| Above Rs 24 lakh | 30% |

Notice how the slabs work. If your income is Rs 10 lakh, you do not pay 10% on the whole amount. You pay nil on the first 4 lakh, 5% on the next 4 lakh, and 10% only on the 2 lakh that sits in the third band. This step by step design is why your average tax rate is always gentler than the top slab you reach.

For assessment year 2026-27 the new regime is automatic. You are taxed slab by slab, so only the portion of income falling inside each band is charged at that band's rate. The headline 30% applies only to income above Rs 24 lakh, not to your whole income.

The rebate that wipes out tax up to Rs 12 lakh

Here is the part that delights most small and mid-sized earners. The new regime carries a rebate under Section 87A of up to Rs 60,000. A rebate is a direct reduction of the tax you owe, applied after the slabs are calculated. Because of it, a taxpayer with taxable income up to Rs 12 lakh effectively pays no tax at all.

Watch how that happens with real numbers. Suppose your taxable income is exactly Rs 12 lakh. Run it through the slabs. The first 4 lakh is nil. The next 4 lakh, from 4 to 8 lakh, is taxed at 5%, which is Rs 20,000. The slice from 8 to 12 lakh is taxed at 10%, which is Rs 40,000. Add those and your tax before rebate is 20,000 plus 40,000, which is Rs 60,000. The Section 87A rebate of up to Rs 60,000 then cancels exactly that amount, leaving your tax at zero.

| Income band within Rs 12 lakh | Rate | Tax |

|---|---|---|

| First Rs 4 lakh | Nil | Rs 0 |

| Rs 4 lakh to 8 lakh | 5% | Rs 20,000 |

| Rs 8 lakh to 12 lakh | 10% | Rs 40,000 |

| Tax before rebate | Rs 60,000 | |

| Less Section 87A rebate | Minus Rs 60,000 | |

| Final tax | Rs 0 |

The old regime has its own, much smaller rebate, up to Rs 12,500, and only if income is Rs 5 lakh or less. You can see why the new regime appeals to so many. Its rebate reaches far higher, up to a full Rs 12 lakh of income.

The Rs 12 lakh "no tax" line comes from the rebate, not from a nil slab. Your tax is still calculated normally, and the rebate then cancels it. Cross that line, even by a little, and the rebate no longer fully applies, so the tax reappears. A small relief called marginal relief softens the jump just above Rs 12 lakh, so that a tiny amount of extra income does not trigger a disproportionately large tax.

One catch for traders and investors

The Section 87A rebate is generous, but it has an important limit that matters specifically to people who trade and invest. The rebate applies to your ordinary income taxed at slab rates, which includes F&O and intraday profits. It does NOT extend to income taxed at a special, fixed rate, and the two big ones for an investor are short-term capital gains on listed shares (taxed at 20% under Section 111A) and long-term capital gains on shares (taxed at 12.5% under Section 112A).

The practical effect is this. You can have a total income within the Rs 12 lakh line and still owe tax, if part of that income is equity capital gains. The slab-rate part may be wiped out by the rebate, but the tax on the special-rate capital gains is calculated separately and is not cancelled by the rebate. So an investor who sells shares should never assume that staying under Rs 12 lakh automatically means zero tax.

The Rs 12 lakh "no tax" comfort applies to slab-rate income, not to equity capital gains. Short-term gains at 20% and long-term gains at 12.5% are charged at their own fixed rates and the Section 87A rebate does not erase them. If you sell shares or equity funds, work out the capital-gains tax on its own, even when your total income looks safely within the rebate.

A worked tax example above the rebate line

Let us follow a trader whose income lands comfortably above the rebate, so you can see real tax being paid. Meera's total taxable income for the year, after all her trading profit and other earnings, is Rs 16 lakh. She is in the new regime by default.

Walk it slab by slab. The first 4 lakh is nil. From 4 to 8 lakh, 5% of 4 lakh is Rs 20,000. From 8 to 12 lakh, 10% of 4 lakh is Rs 40,000. From 12 to 16 lakh, 15% of 4 lakh is Rs 60,000. Her income stops at 16 lakh, so the higher bands do not apply. Add the pieces, 20,000 plus 40,000 plus 60,000, and her tax before cess is Rs 1,20,000. Because her income is above Rs 12 lakh, the full 87A rebate does not rescue her here, so that tax stands.

Meera's taxable income is Rs 16 lakh, new regime. Tax builds up as nil on the first 4 lakh, Rs 20,000 on the 4 to 8 lakh band, Rs 40,000 on the 8 to 12 lakh band, and Rs 60,000 on the 12 to 16 lakh band. That totals Rs 1,20,000 before cess. Health and Education Cess of 4% on 1,20,000 is Rs 4,800. Her final tax is 1,20,000 plus 4,800, which is Rs 1,24,800.

Surcharge and the four percent cess

Two add-ons sit on top of the slab tax, so it helps to know them now.

Surcharge is an extra charge that applies only to higher incomes, kicking in when total income crosses Rs 50 lakh and rising in tiers as income climbs further. Most beginning traders never reach it, but it is worth knowing it exists so a large year does not surprise you.

Cess applies to everyone. After your tax, and surcharge if any, a Health and Education Cess of 4% is added on top. In Meera's case the 4% cess on her Rs 1,20,000 of tax was Rs 4,800, which is why her final bill came to Rs 1,24,800. The cess is small per rupee but it always rides along, so never forget to add it when you estimate your own tax.

When you estimate your tax, finish with the cess. Work out the slab tax, add surcharge only if your income is very high, then add 4% cess on the total. Skipping the cess is a common reason a self-estimate falls short of the real bill.

Choosing the old regime with Form 10-IEA

The new regime is the default, but you are allowed to leave it for the old regime if the old one suits you better, for example when you have large deductions to claim. For a salaried person with no business income, this choice can be made each year fairly freely. For someone with business income, which includes futures and options and intraday traders, the rule is stricter.

If you have business income and want to opt out of the new regime into the old one, you must file Form 10-IEA, and you must do it within the due date for filing your return under Section 139(1). Miss that window and you stay in the new regime for the year. This is an easy step to overlook, and overlooking it can lock you into a regime you did not want.

If you trade futures and options or intraday, you have business income, and choosing the old regime means filing Form 10-IEA on time. Forget it and you are stuck in the new regime for the whole year. Decide early, not on the last day.

For most traders the new regime, with its wide slabs and the rebate up to Rs 12 lakh, is the simpler and often cheaper choice, which is why it is the default. But if you carry heavy deductions, it is worth comparing both before the deadline, ideally with a professional running the numbers both ways.

This chapter is meant for learning only and is not tax advice. Slabs, rebates, and surcharge thresholds can change every year, so please confirm the latest position with a qualified chartered accountant before you file.