The Three Buckets: How Your Profit Is Classified

Before any tax, your gains fall into one of three buckets: capital gains, business income, or speculative income. Learn the simple test that decides which bucket your trades land in, with a clear table, because the bucket changes everything.

- ·Capital gains vs business income

- ·Speculative vs non-speculative

- ·Delivery, intraday, and F&O

- ·Why the bucket matters

- ·The classification table

- ·Examples for each bucket

Picture three people who all spend their day in the stock market. The first buys shares of good companies and holds them for years, checking the price only now and then. The second sits glued to a screen, buying and selling the same stock within a single day, squeezing out small moves. The third trades futures and options, taking large positions that swing fast. To an outsider they are all just "trading". To the tax department, they are three completely different kinds of taxpayer, taxed under three different sets of rules.

This is the most important idea in the whole course, and it is also the one beginners get wrong most often. The tax you pay does not depend only on how much you made. It depends first on which bucket your activity falls into. Get the bucket right, and almost everything else follows. Get it wrong, and you can pay too much, lose valuable benefits, or file a return that the department rejects as defective.

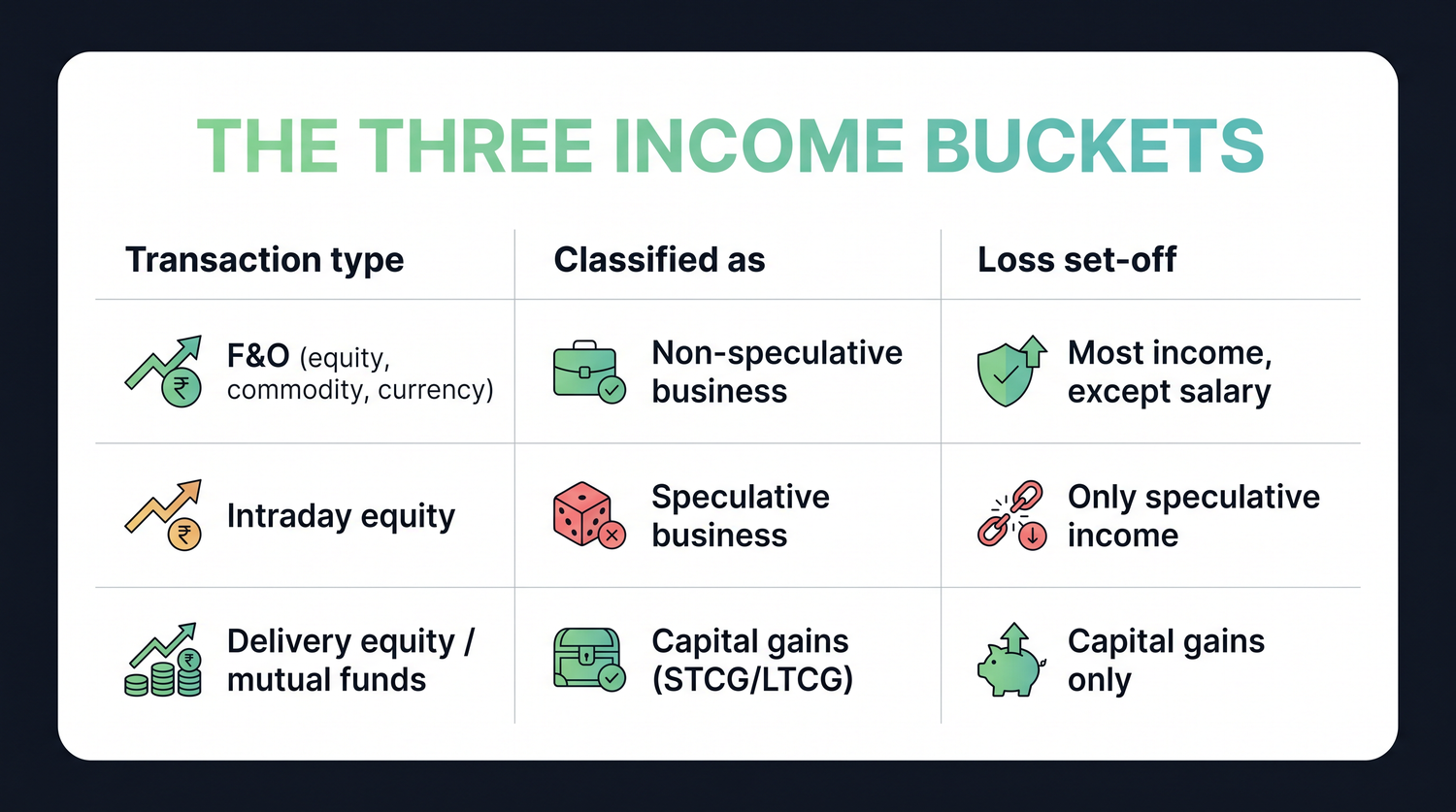

The three buckets at a glance

Every kind of market activity in this course drops into one of three buckets. Each bucket has its own rule for how the income is taxed and, just as important, its own rule for what a loss can be set off against. "Set-off" simply means using a loss to cancel out some gain, so you pay tax only on what is left.

| Transaction type | Which bucket | What a loss can be set off against |

|---|---|---|

| Futures and options (equity, commodity, currency) | Non-speculative business income | Most income heads, except salary |

| Intraday equity trading | Speculative business income | Only speculative income |

| Delivery equity and equity mutual funds | Capital gains, short-term or long-term | Capital gains only |

Read that third column carefully, because it is where the real differences live. A futures and options loss is flexible and can be set off against many kinds of income. An intraday loss is locked in a tiny box and can only be used against other intraday-style gains. A capital loss can only meet a capital gain. Same trader, same market, three very different rule books.

The first question in trader tax is never "how much did I make". It is "which bucket does this fall into". The bucket decides the tax rate, the form you file, and what your losses are allowed to cancel.

The simple test for each bucket

You do not need legal training to sort your trades. A few plain questions will place almost any activity in the right bucket.

Ask first, did I take delivery and hold the shares, even overnight? If the shares actually entered your account and you held them, this is the capital gains bucket. Whether the gain is short-term or long-term depends only on how long you held, which a later chapter covers in full.

Ask next, did I buy and sell the same stock on the same day, without taking delivery? That is intraday equity trading, and it sits in the speculative business bucket. The word "speculative" here is just a tax label for a trade settled without delivery. It does not mean you were reckless.

Ask finally, was this a futures or options contract? Futures and options are always business income, and specifically non-speculative business income, no matter how short or long you held them. This surprises many beginners who assume that because they are "trading", it must be capital gains. It is not. Futures and options are a business in the eyes of tax law.

The word "speculative" is a tax term, not a judgement of your skill. Intraday equity is called speculative only because the shares are never delivered. A careful, disciplined intraday trader still sits in the speculative bucket.

Meet the three traders

Rules stick better when they wear a face, so let us follow our three traders through one year.

Anita is a delivery investor. She buys shares of solid companies and lets them sit. This year she sold some holdings and made a gain. Her activity is capital gains. If she held a stock for twelve months or less, the gain is short-term; if longer, it is long-term. Should she ever book a loss, that loss can only be set off against another capital gain, never against her salary or her bank interest.

Ravi is an intraday scalper. He buys and sells the same shares within the day and never takes delivery. His activity is speculative business income, taxed at his slab rate. Here is the trap he must respect. If he loses money on intraday, that loss can only be set off against other speculative income. It cannot touch his salary, and it cannot even be set off against a futures and options profit.

Meera trades futures and options. Her activity is non-speculative business income, also taxed at slab rates, but with a far friendlier loss rule. A futures and options loss can be set off against most of her income, with salary being the main exception. That flexibility is one reason this bucket matters so much, and the course returns to it in detail later.

Notice that Ravi and Meera are both taxed at their slab rate, because both intraday and futures and options are business income. The difference is not the tax rate. It is the loss rule. Ravi's speculative loss is boxed in tightly, while Meera's non-speculative loss roams freely across most income heads. Anita, sitting in the capital gains bucket, plays by an entirely separate rate book that a later chapter unpacks. Three traders, three rule books, and the only way to keep them straight is to name the bucket first.

A worked example of why the bucket matters

Let us put real rupees on it. Imagine in the same year you have three outcomes. You make a profit of Rs 1,00,000 trading futures and options. You lose Rs 40,000 on intraday equity trades. And you earn a salary alongside all this.

It is tempting to think the intraday loss simply reduces your futures and options profit, so you would be taxed on 1,00,000 minus 40,000, which is Rs 60,000. That is wrong, and the bucket rule is the reason.

| Item | Bucket | Amount | Can it reduce the F&O profit |

|---|---|---|---|

| F&O profit | Non-speculative business | Plus Rs 1,00,000 | This is the profit being taxed |

| Intraday loss | Speculative business | Minus Rs 40,000 | No, speculative loss is ring-fenced |

Your futures and options profit of Rs 1,00,000 stands on its own and is taxed in full at your slab rate. The intraday loss of Rs 40,000 is stuck in the speculative bucket. It can only wait and hope for a future speculative gain to cancel against. Two activities that felt like one "trading account" to you are kept strictly apart by the rules.

Same trader, same year. F&O profit Rs 1,00,000, intraday loss Rs 40,000. Because the buckets differ, the intraday loss cannot reduce the F&O profit. You are taxed on the full Rs 1,00,000 of F&O income at your slab rate, while the Rs 40,000 intraday loss is carried inside the speculative bucket, waiting for a future intraday gain to offset. Mixing the two up would understate your tax and could make your return defective.

Never assume a loss in one bucket can wipe out a profit in another. Intraday losses meet only intraday gains. Capital losses meet only capital gains. F&O losses are the flexible exception, but even they cannot touch salary.

Why this is the foundation

Once you can name the bucket, the rest of the course slots neatly on top. Capital gains have their own rates and a long-term versus short-term split. Speculative and non-speculative business income are taxed at your slab and reported as business in the return. Each bucket also decides which income tax form you must use, and using the wrong form is a common way a return gets marked defective.

So before worrying about rates, rebates, or deadlines, train yourself to ask the bucket question on every trade. Delivery and mutual funds go to capital gains. Intraday equity goes to speculative business. Futures and options go to non-speculative business. That single sorting habit will keep your filing clean and your losses working as hard as they legally can.

Keep a simple note for each activity you do, tagging it as capital gains, intraday speculative, or F&O business. When filing season arrives, that one-line tag tells you the rate, the set-off rule, and the form, all at once.

This chapter is for education only and is not tax advice. The rules and rates here can change from year to year, so do confirm your own filing with a qualified chartered accountant.