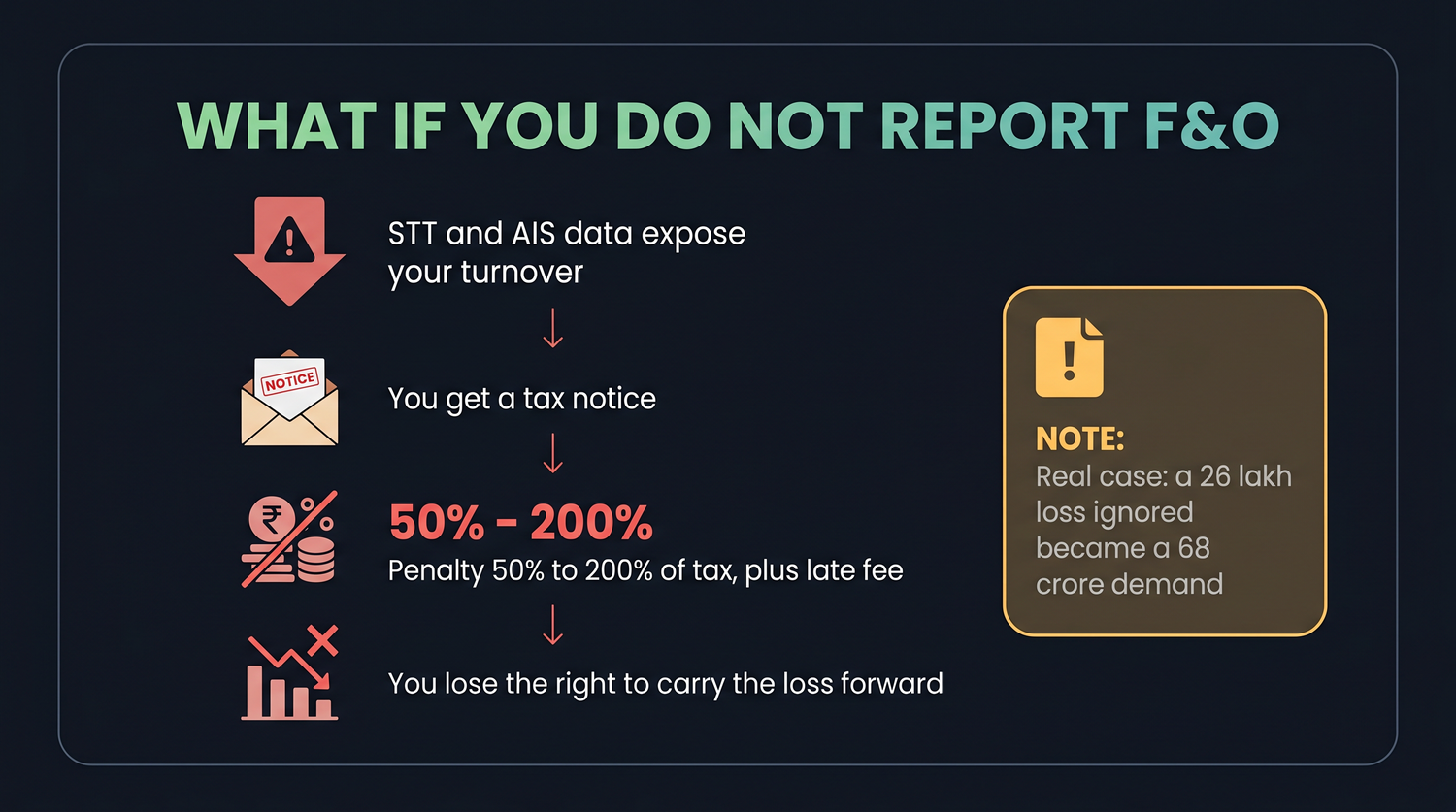

What Happens If You Do Not Report F&O

Hiding an F&O loss feels harmless. It is not. Learn the real case of a trader hit with a crore-sized demand, how the department links your turnover through STT data, and the penalties that turn silence into a disaster.

- ·The crore-sized demand case

- ·How STT data exposes you

- ·The notice under the law

- ·Penalties for non-disclosure

- ·Losing the carry-forward

- ·The simple way to stay safe

There is a story that every F&O trader in India should hear once, slowly, because it changes the way you think about a tax return forever. It involves a farmer in Karnataka, a loss he was sure did not matter, and a tax demand so large it reads like a typing error. The farmer did nothing dramatic. He simply assumed that because he had not made any money trading, there was nothing to report. That one quiet assumption is the most expensive mistake in this entire course. Let us walk through exactly what happened, why the tax department saw his trades even though he stayed silent, and the much smaller, calmer steps that would have kept him completely safe.

The Karnataka farmer: a loss that became a demand

Around 2014, a farmer in Karnataka started trading futures and options. Like many beginners, it did not go well. By the end he was down roughly Rs 26 lakh. He looked at that loss, decided there was no profit and therefore nothing to tell the tax department, and did not file a return for it. To him this felt like simple common sense. You report income, and he had none, so the matter was closed.

It was not closed. In 2021, years after he had moved on, the income tax department reopened his case. When they pulled the trading activity linked to his PAN, the figure was staggering. His F&O turnover, totalled up across all those trades, came to about Rs 69 crore. Remember from the turnover chapter that F&O turnover is the sum of the differences on each trade, not the contract values, but with active trading even a losing account can rack up an enormous turnover figure.

Here is where silence turned into disaster. A notice was issued, and it was missed. Because the farmer never responded to explain that this turnover was a loss-making trading book, the department was within its rights to treat the whole turnover as if it were income. The result was a demand of around Rs 68 crore, made up of tax, penalty and interest piled on top of a number that was never real profit in the first place.

The farmer's actual loss was about Rs 26 lakh. The demand raised against him was about Rs 68 crore. The gap between those two numbers is the entire lesson of this chapter. Nothing about his trading caused that gap. His silence did.

How the department already sees your trades

The natural question is, how did they even know? The farmer never told them anything. The answer is that you do not have to tell them. By the time you place a single F&O trade, two systems have already recorded it against your PAN.

The first is STT, the Securities Transaction Tax. Every futures sale and every options sale carries STT, collected automatically through your broker and exchange and tied to your identity. The government can see, trade by trade, that activity is happening in your name.

The second is the Annual Information Statement, the AIS. This is a yearly summary the department compiles for every taxpayer, pulling together your trades, interest, dividends, large transactions and more, all keyed to your PAN. When you log in to file, much of your financial life is already laid out in front of the department in the AIS.

Think of STT and the AIS together as a quiet ledger the department keeps on you. When you file your return, the system simply checks whether what you reported matches what it already knows. A trader who reports nothing, while the AIS shows heavy F&O turnover, creates an obvious mismatch.

That mismatch is what triggers trouble. A return that does not match the AIS can attract a notice, including a defective-return notice under Section 139(9). The farmer's case was an extreme version of the same mechanic. The data was always there. The only variable was whether he engaged with it.

The penalty list, in plain numbers

When you do not report F&O correctly, the costs are not vague. They are specific sections of the law with specific amounts. Here they are in one place, in plain language.

| What went wrong | The penalty |

|---|---|

| Under-reporting or concealing income (Section 270A) | 50% to 200% of the tax on the under-reported amount |

| Not maintaining books of accounts (Section 271A) | Rs 25,000 |

| Not getting a required tax audit done (Section 271B) | The lower of Rs 1,50,000 or 0.5% of turnover |

| Filing the return late (Section 234F) | Rs 5,000, reduced to Rs 1,000 if total income is up to Rs 5 lakh |

| Filing late, separate cost | You forfeit the carry-forward of your losses |

Read that first row again, because it is the one that did the damage in Karnataka. The penalty for under-reporting can run from half the tax up to twice the tax. When the department treats an entire Rs 69 crore turnover as income, the tax on that imaginary income is already huge, and then a penalty of up to double piles on top, and interest accrues for every year in between. That is how a Rs 26 lakh loss mathematically balloons into a Rs 68 crore demand.

The penalties are not the only loss. Section 234F charges a late-filing fee, but the quieter cost of filing late is losing the right to carry your F&O loss forward for eight years. Miss the deadline and a genuinely useful Rs 5,00,000 loss simply disappears from your future returns.

A worked example: the cost of staying quiet

Let us shrink the farmer's catastrophe down to ordinary scale so the maths is clear. Meet Anjali, a salaried professional who traded F&O on the side and ended the year with a loss of Rs 3,00,000. Like the farmer, she decided a loss meant nothing to report.

Her AIS, however, showed an F&O turnover of Rs 40,00,000 for the year. The mismatch between her silent return and that turnover drew a notice. Now compare the two paths in front of her.

| If Anjali had simply reported | If Anjali stays silent |

|---|---|

| Files ITR-3 showing the Rs 3,00,000 loss | Receives a notice over the AIS mismatch |

| Tax on the trading: nil, it was a loss | Risk that turnover is treated as income |

| Carry-forward of Rs 3,00,000 preserved for 8 years | Carry-forward lost; loss gone forever |

| Late fee under 234F: nil | Possible 234F fee plus 270A penalty of 50% to 200% of tax, plus interest |

Suppose, on the silent path, the department treats just Rs 5,00,000 of Anjali's turnover as unexplained income. At a 20% slab, the tax would be Rs 1,00,000. A Section 270A penalty at the lower end of 50% adds another Rs 50,000, so Rs 1,00,000 plus Rs 50,000 equals Rs 1,50,000, before any interest. On the reporting path, her tax on the same trading was zero, because it was a loss, and she kept a Rs 3,00,000 carry-forward as a bonus. Same trader, same loss, a difference of lakhs.

How to stay completely safe

The reassuring part is that the fix is almost insultingly simple. There is no clever structuring, no aggressive planning, no expensive trick. You just report.

Report your F&O every year, whether it was a profit or a loss. Use ITR-3, the form for traders, and enter the figures from your broker's tax profit and loss and turnover report. If it was a profitable year, you pay the tax due. If it was a loss, you report the loss, which costs you nothing in tax and actively helps you, because reporting the loss is exactly what lets you carry it forward and set it off against future income.

Reporting a loss is not an admission of failure to the tax department. It is the thing that protects you. The farmer's loss, properly filed, would have been a Rs 26 lakh asset carried forward, not a Rs 68 crore liability. Filing on time turns a bad year into a future tax shield instead of a future notice.

So the whole defence comes down to a short routine. Pull your broker reports, reconcile them against your AIS so there is no mismatch, file ITR-3 by the due date, and report every year without exception, especially the losing ones. Do that, and the frightening story of the Karnataka farmer stays exactly what it should be for you, a story you learned from rather than lived.

This chapter is meant for education only and is not a substitute for professional advice. Tax laws, penalty amounts and section numbers can change, so do sit with a qualified chartered accountant to confirm your filing position before you submit your return.