Capital Gains on Shares and Mutual Funds

Buy, hold, sell: the most common way to invest, and its tax. Learn short-term vs long-term, the current rates, the one-year line that divides them, the tax-free LTCG limit, and grandfathering, all with worked examples.

- ·Short-term vs long-term

- ·The one-year holding line

- ·STCG and LTCG rates

- ·The tax-free LTCG limit

- ·Grandfathering explained simply

- ·A full worked example

Priya bought 200 shares of a well known company three years ago. Last month she sold them, and a tidy profit landed in her bank account. She is happy, and then a small worry creeps in. Does she owe tax on that profit? How much? And does it matter that she held the shares for years rather than days? These are the exact questions this chapter answers, and the good news is that capital gains on shares and equity mutual funds follow a small, clear set of rules. Once you know where the lines fall, you can work out your own tax in a couple of minutes.

When you buy a share or a mutual fund unit and later sell it for more than you paid, that profit is a capital gain. The asset rose in value while you owned it, and the government taxes that rise when you sell. If you sell for less than you paid, you have a capital loss, which is not a tax bill but can still be useful, as you will see. The whole subject turns on two questions. How long did you hold the asset, and how big is the gain?

Short-term or long-term: the twelve-month line

For listed shares and equity mutual funds that you buy and sell on a recognised exchange (where Securities Transaction Tax, the small levy on the trade, has been paid), one fact decides everything. The dividing line is twelve months.

If you held the asset for twelve months or less, your gain is short-term. If you held it for more than twelve months, your gain is long-term. That single distinction changes the tax rate, so it is worth checking the buy date and the sell date carefully before you do anything else.

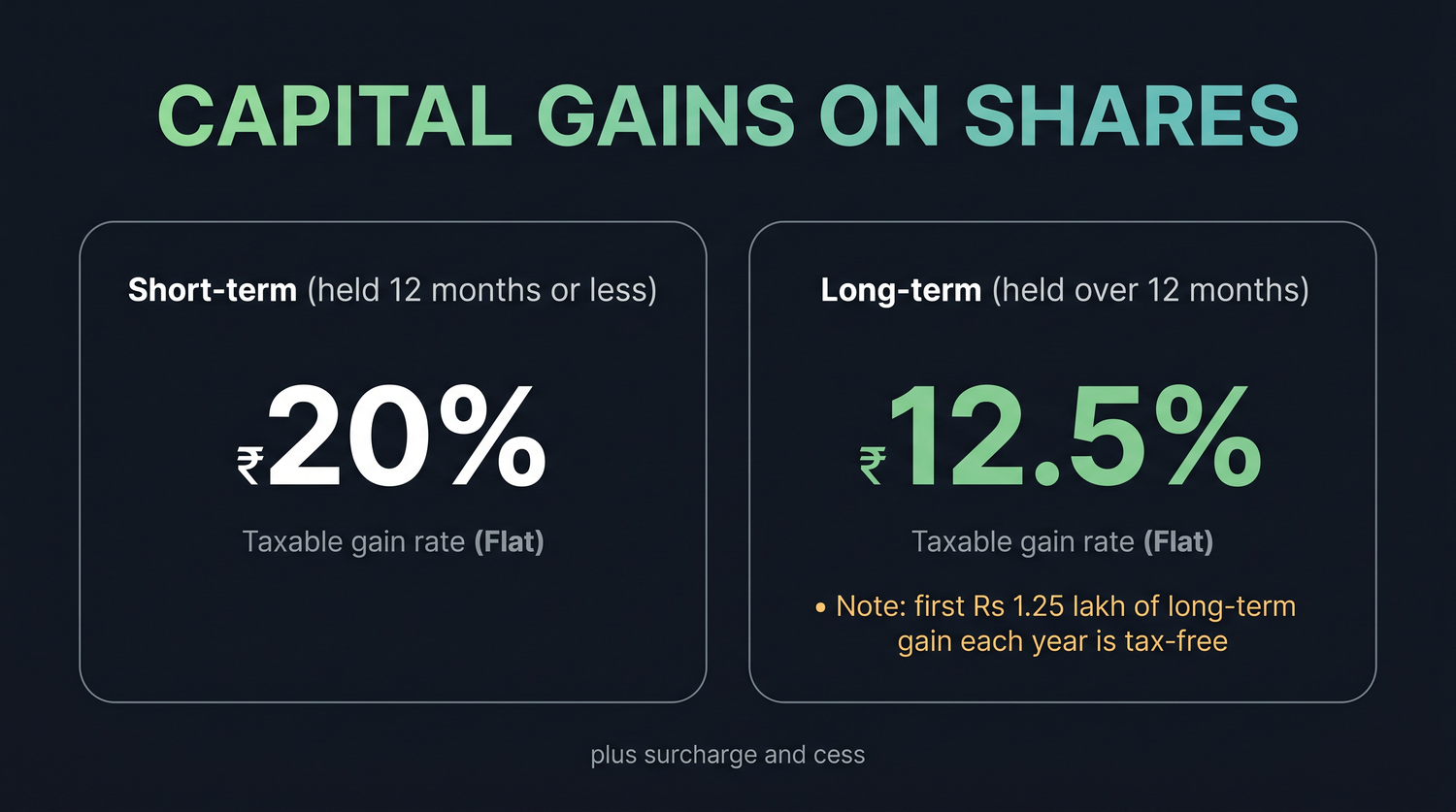

| Holding period | Type of gain | Section | Tax rate |

|---|---|---|---|

| 12 months or less | Short-term (STCG) | 111A | 20% |

| More than 12 months | Long-term (LTCG) | 112A | 12.5% on gains above Rs 1.25 lakh a year |

For listed shares and equity mutual funds, twelve months is the line. Hold for twelve months or less and the gain is short-term, taxed at 20 percent. Hold for more than twelve months and it is long-term, taxed at 12.5 percent, with the first Rs 1.25 lakh of long-term gain each year completely tax-free.

A short note on the section numbers, because they sound scarier than they are. Section 111A is simply the rule for short-term gains on listed equity. Section 112A is the rule for long-term gains on listed equity. You do not need to memorise them. Your tax software and your chartered accountant use them, and now you know what they mean.

How much you actually pay

Short-term gains are the simpler of the two. Take your gain and apply twenty percent, then add surcharge (only if your total income is very high) and the four percent Health and Education Cess on top.

Suppose Priya had instead sold those 200 shares after only eight months, booking a short-term gain of Rs 40,000. Tax at 20 percent on 40,000 equals Rs 8,000, plus the four percent cess on that tax. Short and simple, but you can see the rate is not gentle, which is one reason patient investors prefer the long-term route.

Long-term gains come with a gift built in. The first Rs 1.25 lakh of long-term capital gain in a financial year is tax-free. You pay the 12.5 percent rate only on the long-term gain above that threshold. This exemption resets every year, so an investor who books gains in measured amounts can use it again and again.

Ravi sells equity mutual fund units he held for two years and books a long-term gain of Rs 2,00,000. The first Rs 1.25 lakh is tax-free. The taxable part is 2,00,000 minus 1,25,000, which equals 75,000. Tax at 12.5 percent on 75,000 equals Rs 9,375, plus the four percent cess. That is a remarkably light bill on a two lakh gain, which is the reward for holding for the long-term.

One point about that Rs 1.25 lakh exemption is worth fixing in your mind. It is per person, per financial year, across all your equity shares and equity mutual funds combined. It is not per stock and not per trade. So if you have several winning holdings, plan your selling with the whole year in view, because the single yearly allowance is shared across everything.

A quick word on what does not get this friendly treatment. Debt mutual funds are taxed at your slab rate, not at these equity rates. Other listed securities where no STT was paid follow the 12.5 percent long-term rule but without the equity short-term concession. This chapter is about the common case, which is listed shares and equity mutual funds bought and sold on the exchange.

Grandfathering: protecting gains you made long ago

Here is a question that troubled many investors. The 12.5 percent long-term tax on equity is relatively recent. What about someone who bought shares long ago, when there was no such tax, and watched them grow enormously? Should the government suddenly tax all of that old growth? The answer the law gives is a fair one, and it is called grandfathering.

Grandfathering applies to shares and equity units bought before 31 January 2018. The idea is that gains built up until that date are protected, and only the growth after it is taxed. The law does this by letting you use a higher cost figure when you calculate your gain, so less of the old appreciation is caught in the net.

The rule sounds fiddly, but it is just a two-step comparison. To find the cost of acquisition for a holding bought before that date:

- Take the lower of (the fair market value on 31 January 2018) and (your actual sale price).

- Take the higher of (the figure from step one) and (your actual purchase price).

Whatever comes out of step two is the cost you use. Let us run the classic example through it.

You bought shares for Rs 15,000 long ago. Their fair market value on 31 January 2018 was Rs 18,000. You sold them for Rs 20,000. Step one: the lower of the fair market value (18,000) and the sale price (20,000) is 18,000. Step two: the higher of that 18,000 and your actual cost (15,000) is 18,000. So the cost taken is Rs 18,000, not your real Rs 15,000. Your long-term gain is 20,000 minus 18,000, which equals Rs 2,000. Without grandfathering, the gain would have been 20,000 minus 15,000, equal to 5,000. The rule has shielded Rs 3,000 of your old gain from tax.

For any holding bought before 31 January 2018, look up the fair market value on that date (usually the highest quoted price on 31 January 2018). It can lawfully raise your cost and shrink your taxable gain. Your broker tax statement often applies grandfathering already, but it is worth understanding so you can check the figure.

When the sale is a loss

Not every sale is a profit, and the rules treat losses carefully. A capital loss can be set off only against capital gains, never against your salary or business income. Within that, a long-term capital loss can be set off only against a long-term capital gain. A short-term loss is a little more flexible, because it can be set off against either a short-term or a long-term gain.

If you cannot use the loss this year, you do not lose it. A capital loss can be carried forward for eight assessment years and used against future capital gains, provided you filed your return on time. So even a losing year is worth reporting properly, because the loss becomes a stored credit against future profits.

A full year, start to finish

Let us tie the threads together with a short case study.

Anjali had an active year. In June she sold a stock she had held for five months and booked a short-term gain of Rs 30,000. In December she sold equity mutual fund units held for three years and booked a long-term gain of Rs 1,60,000. She also sold an old family holding bought before 2018, where grandfathering left a tiny long-term gain of Rs 2,000.

Her short-term gain of Rs 30,000 is taxed at 20 percent, which comes to Rs 6,000. Her long-term gains add up to 1,60,000 plus 2,000, which equals 1,62,000. The first Rs 1.25 lakh is tax-free, so the taxable long-term portion is 1,62,000 minus 1,25,000, which equals 37,000. Tax on that at 12.5 percent is Rs 4,625. Her total capital gains tax before cess is 6,000 plus 4,625, which equals Rs 10,625, plus the four percent cess on top.

Notice what the year-long view bought her. By holding most of her winners past twelve months and by leaning on the Rs 1.25 lakh exemption, Anjali turned what could have been a heavy bill into a modest one. That is the practical heart of this chapter. The tax is not something to fear, but it does reward planning around the twelve-month line and the yearly exemption.

Buy date and sell date are not always the obvious calendar dates. For mutual funds bought through a monthly plan, each instalment has its own purchase date and its own holding period. When in doubt, rely on the dated capital gains statement and have a chartered accountant confirm which units are short-term and which are long-term.

This is an educational guide only and not tax advice. Rates and rules change with every Budget, so confirm the current position with a qualified chartered accountant before you file.