Why Tax Matters

A true story of a trader who lost money yet ended up owing crores, because he never filed. Learn why the tax department already knows your trades, and why ignoring tax is the most expensive mistake a trader can make.

- ·The trader who owed crores on a loss

- ·How the department already sees your trades

- ·Profit or loss, you still report

- ·What this course covers

- ·A promise: plain English only

- ·The one rule: file, every year

In a quiet town in Karnataka, a farmer opened a trading account and started buying and selling futures and options. This was around 2014. Like many beginners, he traded actively, hoping the market would add to a modest farming income. It did not. By the time he stopped, he had lost about Rs 26 lakh of his own money. There was no profit, no windfall, nothing to celebrate. So he did what felt natural. He shut the account, swallowed the loss, and did not file an income tax return for those trades. His reasoning was simple and, to most beginners, completely understandable. If there is no profit, there is nothing to report.

That one assumption almost destroyed him.

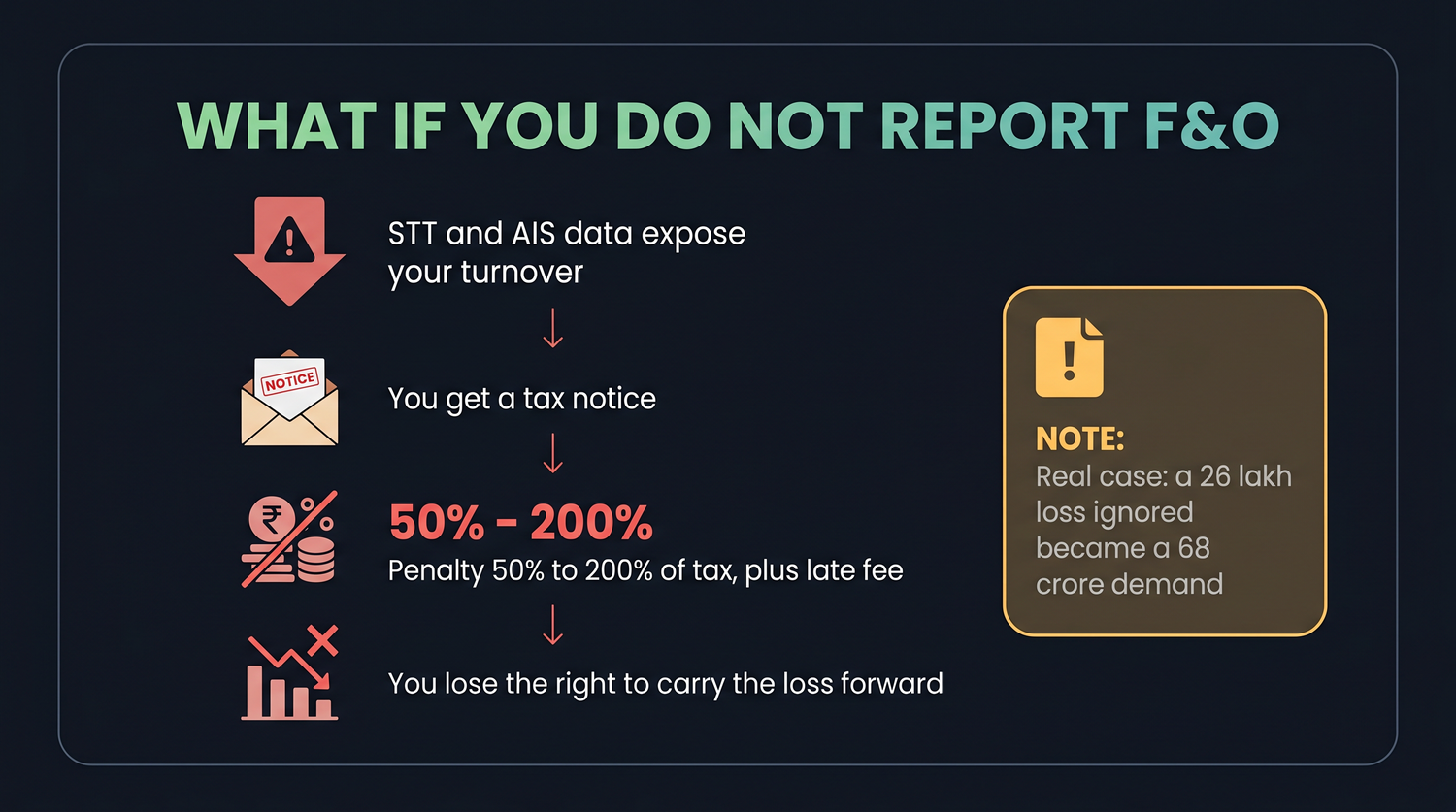

In 2021, years after he had moved on, the income tax department reopened his case. When they pulled the records linked to his PAN, they found something he had never thought about. His total futures and options turnover, the full value churned through all those trades, came to about Rs 69 crore. Not his loss, not his profit, but the sheer size of activity that had passed through his account. A notice went out asking him to explain. He missed it. He was a farmer, not someone who checks an income tax portal. And when a taxpayer does not respond, the department is allowed to make its own assessment. With no explanation on record, the entire Rs 69 crore of turnover was treated as if it were income. The demand that landed on him, tax plus penalty plus interest, came to around Rs 68 crore.

How a small loss became a giant demand

Sit with that for a moment. A man who lost Rs 26 lakh was handed a bill for roughly Rs 68 crore. The gap between those two numbers is the entire reason this course exists.

He did nothing dishonest. He had no profit to hide. His only mistake was silence. He never filed, so he never told the department, in its own language, that this was a loss and not income. The system does not assume the best on your behalf. When you stay quiet, it fills the blank with the worst case, and the worst case here was that every rupee of turnover was taxable.

Had he simply filed a return showing the loss, almost none of this would have happened. A reported loss is just a loss. It is not income, it carries no tax, and as you will see later in this course, it can even be carried forward to save tax in future years. The act of reporting is what protects you. Hiding nothing is still very different from saying nothing.

The danger is rarely the tax itself. The danger is not filing. An unreported account leaves a blank that the department is free to fill with its own assumption, and that assumption is almost never in your favour.

The department already sees every trade

Many traders quietly believe their activity is invisible. It is not, and it has not been for years. Almost everything you do in the market leaves a digital footprint that flows straight to the tax department, with your PAN attached.

The first source is Securities Transaction Tax, usually called STT. Every time you buy or sell shares, futures, or options on an exchange, a tiny tax is collected on the spot. Sell one futures lot worth Rs 5,00,000 and STT of 0.05% of 5,00,000, which is Rs 250, is taken automatically. Buy 500 shares at Rs 100 each for delivery, and STT of 0.1% of 50,000, which is Rs 50, is collected. You may not even notice these small amounts, but each one is a stamped record that a trade happened, on what value, under your name.

The second source is the Annual Information Statement, or AIS. This is a yearly summary the department prepares for you, pulling together your trades, dividends, interest, big purchases, and more, all gathered from banks, brokers, and exchanges. Your broker reports your trading data. The exchange reports turnover. It all lands in one place, tagged to your PAN, long before you sit down to file.

So the real picture is the opposite of what beginners imagine. The department often knows the shape of your trading year before you do. Filing is not you volunteering a secret. It is you confirming a story they already half know. When your return matches their records, life is calm. When it does not, or when there is no return at all to compare against, that mismatch is exactly what triggers a notice.

Think of it like a school attendance register that someone else is already keeping. Your broker marks you present every time you trade, and the exchange notes the size of each position. By the year's end there is a full record with your name on it. Filing your return is simply you signing the same register and agreeing with what it says. Refusing to sign does not erase the entries. It only makes you look like the one person who would not confirm a record everyone else can already read.

You do not reveal your trades by filing. They are already reported through STT and the AIS, tagged to your PAN. Filing simply lets your version match theirs, which is what keeps you out of trouble.

Profit or loss, you still file

Here is the single habit that would have saved the Karnataka farmer. You file your return every year you trade, whether you made money or lost it. A loss is not a reason to skip filing. A loss is a reason to file with extra care, because reporting it is what protects you.

Reporting a loss does two good things. First, it tells the department the truth, so no one can later treat your turnover as income. Second, a properly reported and on-time loss can be carried forward and used to reduce tax in later, more profitable years. Skipping the return throws both benefits away.

Suppose this year your futures and options trading ends in a net loss of Rs 2,00,000. You file your return on time and report it honestly. Next year your trading turns around and you make a profit of Rs 3,00,000. Because you reported and carried forward last year's loss, you can set it off against this year's gain. You are taxed on only 3,00,000 minus 2,00,000, which is Rs 1,00,000, instead of the full 3,00,000. The loss you bothered to report became real money saved. Had you stayed silent, that Rs 2,00,000 would simply have vanished.

That is the quiet power of filing. Even a painful year can be turned into a future saving, but only if you write it down in a return that reaches the department on time.

Consider a second, gentler story to balance the farmer's. Priya traded futures and options for a year and ended down by Rs 1,50,000. She was disheartened, but she still filed her return and reported the loss before the deadline. Two years later she had learned from her mistakes and made a profit of Rs 4,00,000. Because her earlier loss was reported and carried forward, she set off the Rs 1,50,000 against that profit and was taxed on only Rs 2,50,000. The very loss that once felt like pure pain came back as a real reduction in her future tax. The only thing she did right at the time was file. Everything good that followed grew from that one small act of discipline.

What this course will walk you through

Tax for traders feels frightening mostly because no one explains it in plain language. This course is built to fix that, one small idea at a time, with examples in rupees and stories you can relate to.

Over the coming chapters you will learn the three buckets your income can fall into, and why the bucket matters more than the amount. You will see how the new tax regime works, with its slabs, its rebate, and the deadlines for advance tax. You will understand capital gains on shares and mutual funds, the charges that nibble at every trade, and why futures and options are treated as business income rather than capital gains. You will meet the idea of turnover, the tax audit, and how losses can be set off and carried forward. Later chapters cover US stocks, foreign asset disclosure, crypto, and finally a simple year-round checklist you can actually follow.

You do not need to memorise statute numbers to stay safe. You need three habits. File every year, file on time, and report honestly even in a losing year. Everything else in this course builds on those three.

The goal is not to turn you into an accountant. It is to remove the fear, so that when filing season arrives you feel calm and prepared instead of anxious and confused. The farmer's story is extreme, but its lesson is gentle. Tax trouble almost never comes from making a loss. It comes from saying nothing about it. Once you decide to report every year, the scariest version of this whole subject is already behind you.

A reported loss is harmless. An unreported account is what becomes dangerous. The cheapest insurance a trader can buy is a return filed on time, every single year.

This chapter is for learning only and is not tax advice. Tax rules and rates change every year, so please confirm your own situation with a qualified chartered accountant before you file.