Which ITR Form Is Yours

The wrong return form can invalidate your whole filing. Learn, in one simple map, which ITR form fits an investor, an intraday or F&O trader, a US-stock holder and a crypto trader, and why most traders end up on ITR-3.

- ·ITR-1 and ITR-2

- ·ITR-3 for business income

- ·ITR-4 and presumptive tax

- ·Which form for which trader

- ·Why F&O means ITR-3

- ·Mixing investing and trading

Picture two friends, Anjali and Vikram. Both made money in the markets last year, both sat down in good faith to file their taxes, and both typed their figures into a form on the income tax website. Three months later, only one of them received a notice. The difference was not how much they earned, and it was not honesty. It was a single choice at the very top of the page: which ITR form they picked.

Choosing your ITR form sounds like a boring administrative step, the kind of thing you rush through to get to the "real" numbers. But it is one of the few tax decisions where a wrong click, all by itself, can make your entire return invalid. The good news is that the rule for traders and investors is simpler than it looks. Once you can place yourself on a small map of four forms, you will know exactly where you belong, and why.

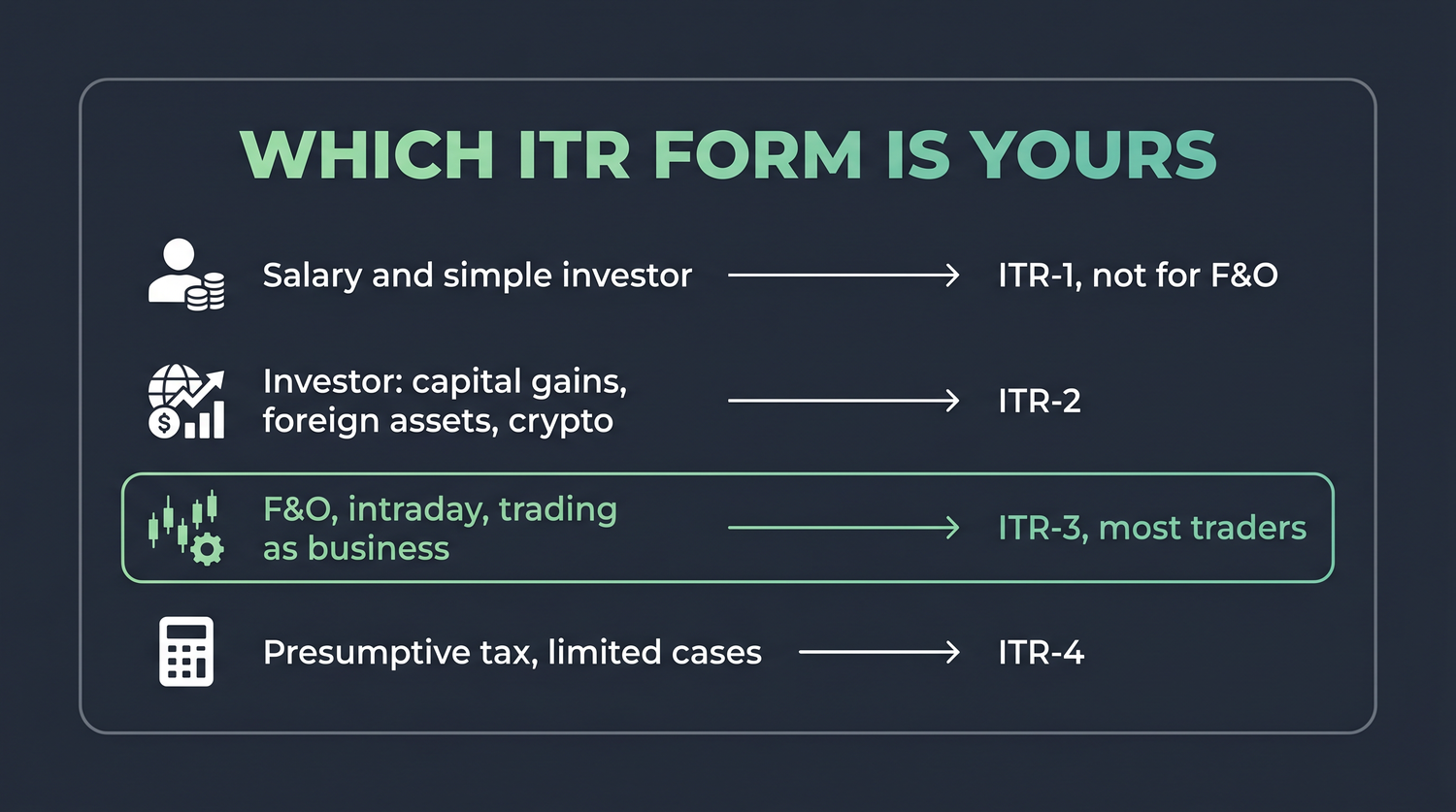

The four forms on one map

There are four income tax return forms that an individual is likely to meet. Each is built for a different kind of taxpayer. Think of them as four doors, and your job is to walk through the right one.

| Who you are | Form |

|---|---|

| Salary and a simple investor, small income | ITR-1 (Sahaj), but NOT for business or F&O |

| Investor with capital gains, foreign assets, or crypto as capital gains | ITR-2 |

| F&O, intraday, or trading as a business; crypto as business | ITR-3 (most traders) |

| Presumptive tax in limited eligible cases | ITR-4 (Sugam) |

The single most useful sentence in this whole chapter is this one: most active traders end up on ITR-3. If you trade futures and options, or you do intraday, or you treat trading as a business, that is your door. Everything else in this chapter is really about helping you confirm it, and understanding why the simpler forms will not fit you.

The form is not about how much you earned. It is about what KIND of income you earned. Salary, capital gains, and business income each have their own home, and the form you choose has to be roomy enough to hold all the kinds of income you have.

ITR-1 and ITR-4, the simple forms (and their limits)

ITR-1, also called Sahaj, is the easiest form. It is meant for a salaried person who also has some interest income and perhaps one house property, with a modest total income. A pure saver who keeps money in a bank and a fixed deposit, with no share trading at all, lives here comfortably.

The trap is that ITR-1 was never designed for the markets. The moment you have capital gains from selling shares or mutual funds, ITR-1 stops being the right form, because it has no place to report them. And it absolutely cannot hold business income, which is what F&O and intraday produce. So if you have done any serious trading, ITR-1 is the wrong door, full stop.

ITR-4, also called Sugam, is built for the presumptive taxation scheme, where small businesses and professionals declare income as a fixed percentage of turnover instead of maintaining full books. It suits, say, a small shopkeeper or a freelance professional under the presumptive rules. For traders it applies only in limited eligible cases, and most active F&O traders do not fit neatly into it. Treat ITR-4 as a special case to discuss with a chartered accountant, not your default.

If you traded F&O or did intraday even once during the year and you reach for ITR-1, you have almost certainly chosen the wrong form. ITR-1 has no room for capital gains and no room for business income. This is the most common beginner mistake at the very first step.

ITR-2, the investor's form

ITR-2 is the form for the investor who is not running a trading business. If your market activity is buying shares and mutual funds and holding them, so that your profits are capital gains rather than business income, ITR-2 is usually where you belong.

ITR-2 is roomy. It can hold salary, more than one house property, and capital gains both short-term and long-term. Crucially, it is also the form that carries Schedule FA, the section where a resident must disclose foreign assets such as US shares and ETFs, and Schedule VDA, where crypto is reported when you are treating it as capital gains. So the calm long-term investor who owns some Indian stocks, a few US shares, and a little crypto held as an investment can do everything on ITR-2.

A quick test helps you place yourself. Ask: "Am I an investor who occasionally sells, or am I a trader running an activity?" Delivery shares and mutual funds held for their gains are capital gains, and that is ITR-2 territory. F&O and intraday are business income, and that pushes you to ITR-3.

The one thing ITR-2 cannot do is business income. It has no section for "profits and gains of business or profession." And that is exactly the line F&O and intraday cross. The moment your activity becomes business income, ITR-2 is no longer enough, and you move up to ITR-3.

ITR-3, the trader's home

ITR-3 is the form most active traders end up using, and once you understand why, the whole map clicks into place. ITR-3 is the only individual form that can report business income, the bucket that holds F&O and intraday.

Remember the classification from earlier in the course. Futures and options are non-speculative business income. Intraday equity is speculative business income. Both are reported under "profits and gains of business or profession," and that section lives only in ITR-3. So if you trade derivatives or do intraday, ITR-3 is not optional, it is the correct form by definition.

What makes ITR-3 so powerful is that it is the most complete of the four. It can hold everything the other forms can hold and then add business income on top. Salary, house property, capital gains from your delivery investments, foreign assets in Schedule FA, crypto in Schedule VDA whether as capital gains or as business, and your F&O and intraday business income, all on one return. That is why the busy person who both invests and trades almost always lands here.

If you trade F&O and you also opt for the old tax regime, remember Form 10-IEA. Because you have business income, opting out of the default new regime needs Form 10-IEA filed within the due date under Section 139(1). It is easy to miss, so flag it before you file.

When you both invest and trade

Here is the situation that confuses most people, and it is more common than you would think. You have a salary. You also hold some shares for the long term, which gives you capital gains when you sell. And on the side, you trade a few F&O lots, which is business income. Three different kinds of income in one year. Which form?

The answer is reassuring once you see it: you can have capital gains AND business income on the very same return. You do not file twice and you do not choose between them. ITR-3 is built to carry both at once. Your long-term investments go into the capital gains schedule, your F&O sits in the business schedule, your salary in the salary section, and it all adds up to one total income on one form.

Meet Vikram. During the year he earned a salary, sold some shares he had held for two years and made a long-term capital gain of 80,000 rupees, and traded futures and options for a small business profit of 40,000 rupees.

He cannot use ITR-1, because it holds neither capital gains nor business income. He cannot use ITR-2, because although it holds his salary and his capital gains, it has no room for the F&O business profit. The F&O is the deciding factor. Vikram files ITR-3, where his salary, his 80,000 capital gain, and his 40,000 business profit all sit comfortably together. One form, all three kinds of income.

His friend Anjali, by contrast, only held shares as an investor and never touched F&O, so her capital gains fit neatly in ITR-2. Same markets, different doors, because the kind of income was different.

The simple rule that falls out of this: pick the form by the most demanding kind of income you have. If any part of your year is business income, F&O or intraday, you need ITR-3, even if most of your money came from salary or investments. The most demanding bucket sets the form.

Why the wrong form makes a return defective

So what actually happens to someone who picks the wrong door? This is where Anjali and Vikram's story comes back. A return filed on the wrong form can be treated as defective. The department can issue a defective-return notice under Section 139(9), telling you that the form you used does not match the income you reported, and giving you a window to fix it.

A defective return is not the end of the world, but it is a headache you do not need. If you ignore the notice or miss the window, the return can be treated as if it was never filed at all. And a return that is treated as not filed loses one of the most valuable things a trader has: the ability to carry a loss forward. If you reported an F&O loss on the wrong form and the return becomes invalid, you can lose the right to set that loss against future profits, which is precisely the protection you filed for in the first place.

The wrong form is not a small typo, it can make the whole filing defective under Section 139(9). The most frequent cause is reporting F&O as capital gains on ITR-2, instead of as business income on ITR-3. F&O is business income. If you have it, ITR-3 is your form.

Put it all together and the map is short enough to keep in your head. A pure salaried saver with no market activity uses ITR-1. An investor with capital gains, foreign shares, or crypto held as an investment uses ITR-2. Anyone with F&O, intraday, or trading as a business, which is most active traders, uses ITR-3, and ITR-3 happily carries their investments too. ITR-4 is a limited presumptive case to raise with a professional. Choose by your most demanding income, and you walk through the right door the first time.

This chapter is for learning only and is not tax advice. Tax forms, schedules, and rules change from year to year, so before you file for AY 2026-27 please confirm your correct form with a qualified chartered accountant.