STT and the Charges Hiding in Every Trade

Every trade carries a Securities Transaction Tax and a stack of other charges. Learn what STT is, the rates on delivery, intraday, futures and options after the latest hike, and how these costs interact with your income tax.

- ·What STT is and who pays

- ·STT rates by trade type

- ·The latest STT hike

- ·Other charges in a contract note

- ·How STT affects your tax

- ·A worked STT calculation

Look closely at the contract note your broker sends after a trade and you will notice something. The price you paid for the shares is only part of the story. Stacked underneath are a handful of small charges, and one of them carries a name that confuses almost every beginner. It is called Securities Transaction Tax, or STT. It is tiny on a single trade, yet it quietly shapes how much active trading really costs, and for a serious trader it has a useful tax side too. This chapter explains what STT is, shows you the current rates, and walks you through the simple sums on a few real trades.

STT is a tax the government charges on the value of trades in listed securities. You do not pay it separately. It is collected automatically by the exchange through your broker at the moment you trade, so it appears on the contract note already deducted. Because it is fixed by law and the same for everyone, you cannot negotiate it or avoid it. The only thing that changes your STT bill is what you trade and how much.

What STT is and why it exists

The government introduced STT as a clean, hard-to-dodge way of taxing market activity. Every eligible trade leaves a digital footprint, and STT rides on that footprint. This matters for a reason that goes beyond the charge itself. Because STT is reported against your PAN, the tax department can see roughly how much you traded in a year, even before you file anything. We return to that idea elsewhere in the course, but keep it in mind. STT is both a charge and a tracker.

For you as a trader or investor, two practical things follow. First, you should know the rates so the numbers on your contract note never surprise you. Second, if you trade as a business, STT is a cost you are allowed to deduct, which softens its sting.

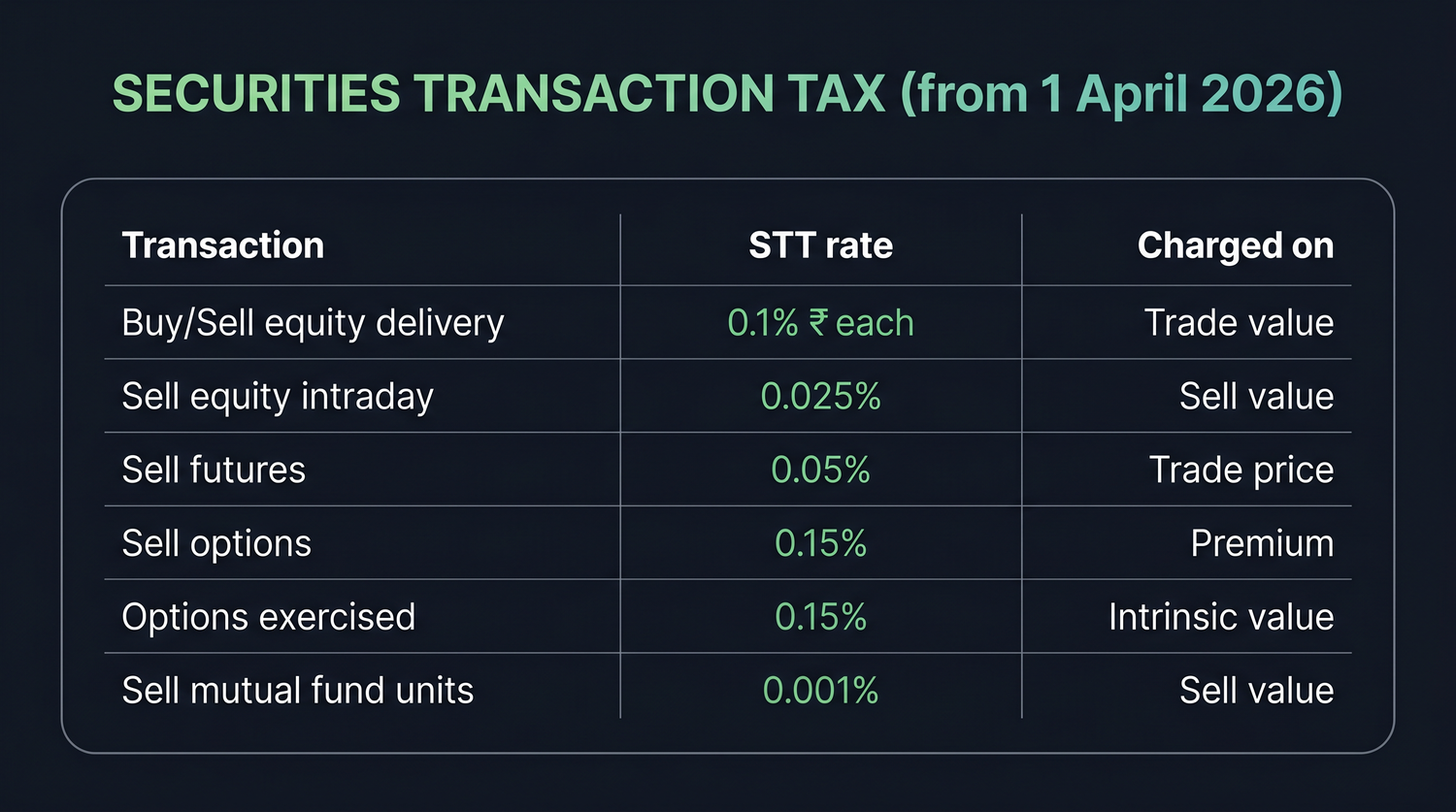

The STT rate table

Rates were revised in the Budget and the figures below are effective from 1 April 2026. Notice that for most products STT falls on the seller, and that delivery trades are charged on both the buy and the sell side.

| Transaction | STT rate | Paid by | Charged on |

|---|---|---|---|

| Buy or sell equity delivery | 0.1% each side | Buyer and seller | Trade value |

| Sell equity intraday | 0.025% | Seller | Sell value |

| Sell equity mutual fund units | 0.001% | Seller | Sell value |

| Sell futures | 0.05% | Seller | Trade price |

| Sell options | 0.15% | Seller | Option premium |

| Options exercised | 0.15% | Purchaser | Intrinsic (settlement) value |

For most trades, STT is paid by the seller. The big exception is equity delivery, where both the buyer and the seller pay 0.1 percent. Options are charged on the premium, not on the large notional value of the contract, which keeps the rupee figure small.

The Budget hike on futures and options

The Budget raised STT on derivatives, and the reasoning was openly stated. Futures and options had drawn in a wave of very active traders, and the government wanted to curb excessive speculation. Raising the cost of each trade is one lever to do that.

The new derivative rates are 0.05 percent on the sale of futures and 0.15 percent on the sale of options, where the option figure is charged on the premium. These may look like rounding errors, but for someone placing dozens of trades a day they add up into a real monthly cost. A higher STT makes rapid-fire trading more expensive, which is precisely the intended effect.

STT on options is charged on the premium, not on the full contract value. That is why selling an option that controls lakhs of rupees of stock can cost only a few rupees in STT. Always read the rate against the base it applies to.

Working out STT on real trades

The arithmetic is the same every time. Take the value the rate applies to, then multiply by the rate. Here are three worked sums covering the most common situations.

Selling one futures lot. You sell a futures contract worth Rs 5,00,000. STT on the sale of futures is 0.05 percent. So STT equals 0.05 percent of 5,00,000, which equals Rs 250.

Buying shares for delivery. You buy 500 shares at Rs 100 each, a trade value of Rs 50,000. Delivery STT is 0.1 percent on each side. So STT on the buy equals 0.1 percent of 50,000, which equals Rs 50.

Selling an option. The premium is Rs 50 and the lot size is 65, so the premium value is 50 times 65, which equals Rs 3,250. STT on the sale of an option is 0.15 percent. So STT equals 0.15 percent of 3,250, which equals Rs 4.88.

Put those three beside each other and the pattern is clear. The futures sale on a five lakh contract cost Rs 250. The delivery purchase cost Rs 50. The option sale on a contract controlling thousands of rupees of stock cost under five rupees, because options are charged only on the premium. None of these is large on its own. The cost shows up in the totals when you trade often.

| Trade | Base value | Rate | STT |

|---|---|---|---|

| Sell 1 futures lot | Rs 5,00,000 | 0.05% | Rs 250 |

| Buy 500 shares delivery | Rs 50,000 | 0.1% | Rs 50 |

| Sell 1 option lot | Rs 3,250 premium | 0.15% | Rs 4.88 |

How the small charge adds up over a year

A single STT of a few hundred rupees feels trivial, and on one trade it is. The picture changes when you count a whole year of activity. Suppose a futures trader sells twenty contracts a month, each worth about Rs 5,00,000. At Rs 250 of STT per sale, that is twenty times 250, which equals Rs 5,000 a month, and across twelve months it equals Rs 60,000 for the year, on the sell side of futures alone. Add the option sales and the delivery purchases, and the annual STT for an active trader climbs into a number that genuinely matters.

This is exactly the effect the Budget hike was designed to have. By making each derivative trade a little more expensive, the higher STT nudges traders to trade with more care and less churn. For the long-term investor who buys delivery and holds, STT barely registers, because it is charged only on the way in and out and the holding does the work in between. For the rapid trader, STT is a steady cost of doing business that rewards selectivity over sheer volume.

It helps to know how the plumbing works. STT is collected at source by the exchange and remitted to the government, so there is no separate STT return for you to file. It is one of the most leak-proof taxes in the system, which is part of why the department can use the STT trail to estimate a trader's turnover for the year.

The sensible response is not to fear STT but to fold it into how you think about a trade. A strategy that needs hundreds of trades to make a small edge has to clear its STT cost first. A calmer, more selective approach pays STT far less often. The charge quietly favours patience, and that is worth remembering when you compare trading styles.

STT is a deductible business expense

Here is the part that turns STT from a pure cost into something more bearable. If you trade as a business, which most active futures, options and intraday traders do, then STT paid is a business expense you can deduct from your trading income. It reduces the profit on which you are taxed.

This is a meaningful difference from the old days, and it is one reason classifying your activity correctly matters. An investor reporting capital gains treats charges differently from a trader reporting business income. For the trader, every rupee of STT, brokerage and other allowed charges comes off the top before tax is worked out.

Do not add up STT by hand. Your broker provides a yearly tax profit and loss statement that totals STT and the other charges for you. Hand that statement to your chartered accountant so the full deductible amount is captured. Missing it simply means paying more tax than you needed to.

Let us see this in a short case study.

Vikram trades futures and options full time. Over the financial year his trades net a profit of Rs 6,00,000 before charges. His broker statement shows STT of Rs 45,000 along with other allowable charges. Because he reports this as business income, the STT and the other charges are deductible. His taxable trading profit drops by the STT alone from 6,00,000 to 5,55,000, and then further once the remaining charges are subtracted. The STT he could not avoid paying at least works for him at tax time by lowering the income he is taxed on.

STT is only one line on the contract note. Brokerage, exchange charges, the Goods and Services Tax on those charges, stamp duty and SEBI fees also apply, and the regulator charges may differ by segment. Treat the broker tax statement as the single source of truth for the year, and let a professional reconcile it.

The takeaway is calm and practical. STT is a small, fixed tax you cannot escape, charged mostly on the seller, raised recently on derivatives to slow down heavy speculation. Know the rates, check your contract notes against them, and if you trade as a business, make sure your STT is claimed as the deductible expense it is.

This chapter is educational only and not tax advice. STT rates are revised in the Budget from time to time, so confirm the current figures and your own treatment with a qualified chartered accountant before you file.