F&O Turnover Is Not What You Think

The single biggest F&O confusion is turnover. Learn why turnover is not your contract value but the sum of your gains and losses, how options add the premium, and the genuine expenses you can claim against your profit.

- ·Turnover is not contract value

- ·The absolute profit method

- ·How options premium is added

- ·Using your broker tax report

- ·Expenses you can claim

- ·Keeping the proofs

Anita opened her broker tax report, scrolled to the bottom, and felt her stomach drop. The "total contract value traded" line read Rs 3.2 crore. She had traded Nifty and Bank Nifty options all year, a few lots at a time, and somehow the number had grown to a figure that looked like she was running a small empire. "If my turnover is over three crore," she thought, "I must need a tax audit, maybe even owe a fortune." She closed the laptop and lost a night's sleep over a number that meant almost nothing.

Anita made the most common turnover mistake there is. She confused the value of the contracts she traded with her tax turnover. They are completely different things, and the gap between them is enormous. This chapter shows you what F&O turnover really is, how to compute it in a couple of minutes, and which expenses you are allowed to subtract before you are taxed.

Turnover is not the contract value

When you trade one Nifty lot, the contract might be worth several lakh rupees. Trade in and out a few hundred times in a year and those contract values pile up into crores. But that pile is not your turnover for tax purposes. It never was.

For working out the tax-audit threshold, the accountancy body's guidance is clear. Turnover is not the contract value. It is the aggregate of your favourable and unfavourable differences. In plain words, you add up the absolute value of every profit and every loss. A loss counts as a positive number here, not a negative one. You are measuring how much trading you did, not whether you won or lost.

This single idea shrinks Anita's terrifying Rs 3.2 crore down to something far smaller and far more honest. Her contract value was crores. Her actual turnover, once we add up only the profits and losses, turns out to be a tiny fraction of that.

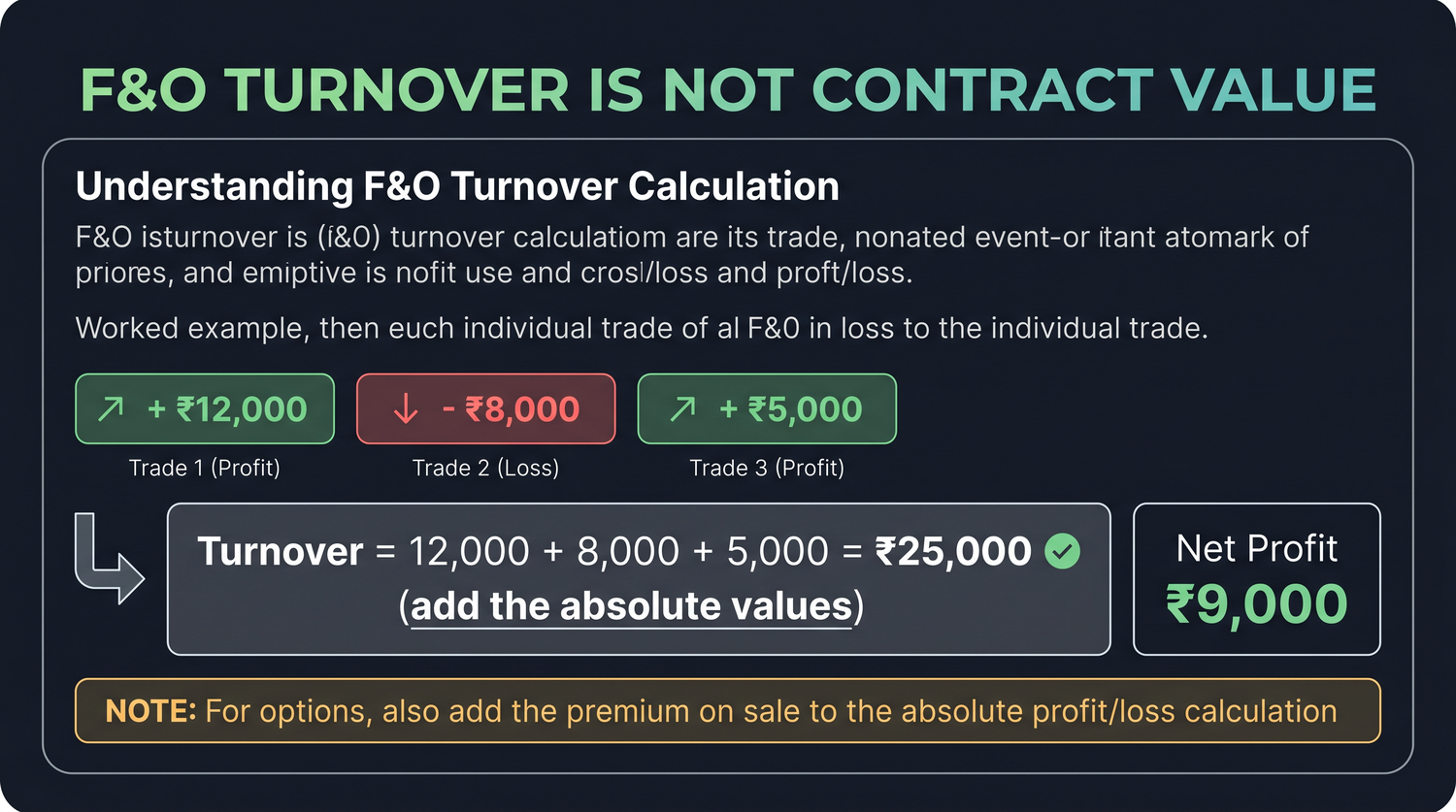

Turnover for F&O is the sum of the absolute values of every profit and every loss, not the value of the contracts you traded. A profit of Rs 12,000 and a loss of Rs 8,000 together add Rs 20,000 to your turnover, not several lakh.

The absolute-difference method, worked step by step

The cleanest way to learn this is with three trades. Suppose over the year you make exactly three F&O trades and they settle like this:

| Trade | Result | Absolute value (for turnover) |

|---|---|---|

| First | Profit of Rs 12,000 | 12,000 |

| Second | Loss of Rs 8,000 | 8,000 |

| Third | Profit of Rs 5,000 | 5,000 |

To get your turnover, you ignore the plus and minus signs and add the three absolute values together. So turnover equals 12,000 plus 8,000 plus 5,000, which is Rs 25,000.

Now compare that with your actual profit, which is what you are taxed on. There you do respect the signs: 12,000 minus 8,000 plus 5,000 equals a net profit of Rs 9,000. Two different numbers from the same three trades, doing two different jobs. The Rs 25,000 turnover is only used to check whether you cross an audit threshold. The Rs 9,000 net profit is what actually gets taxed.

Three trades: profit 12,000, loss 8,000, profit 5,000. Turnover is 12,000 plus 8,000 plus 5,000 equals Rs 25,000. Net profit is 12,000 minus 8,000 plus 5,000 equals Rs 9,000. Turnover measures activity; net profit measures the money you keep and pay tax on.

Carry this method to Anita. Her contract value was Rs 3.2 crore, but when she added up the absolute value of each winning and losing trade across the year, her turnover came to roughly Rs 6 lakh. That is the number that matters for the audit question, and it is nowhere near the crores that frightened her. The contract value was a red herring all along.

Options add the premium received on sale

Options have one extra twist, and it is worth getting right. For options, you add the premium received on the sale of options to the turnover figure as well, on top of the favourable and unfavourable differences.

The reason is that when you sell or write an option, the premium you receive is itself a measure of the business you transacted. So it joins the turnover count. There is one sensible guard against double counting. If that sale premium is already sitting inside your net profit figure, you do not add it a second time. The aim is to count each rupee of activity once, not twice.

In practice you should not be doing this arithmetic by hand at all. Your broker provides a tax profit-and-loss statement, often labelled a "turnover report", that already applies these rules for you. It lists your realised profits, your realised losses, and the option premium component, and it totals the turnover the way the guidance requires.

Do not compute F&O turnover by hand from your contract notes. Download your broker's tax profit-and-loss or turnover report, which already adds the absolute profits, the absolute losses, and the option sale premium correctly. Then have a chartered accountant review the figure before you rely on it.

Never use the contract value or the total traded value as your turnover. It is many times larger than the real figure and will make you believe you have crossed thresholds you are nowhere near. The audit question is decided on the absolute-difference turnover, not on contract value.

The expenses you are allowed to claim

Here is the quiet advantage of F&O being a business. A business is taxed on its profit after expenses, not on its gross takings. So before your F&O profit is taxed, you may subtract the genuine costs of earning it. These are real deductions that reduce your tax, and most beginners forget to claim them.

| Expense | What it covers |

|---|---|

| Brokerage | The fee your broker charges on each trade |

| Securities Transaction Tax (STT) | For a trader, STT paid on trades is a business expense |

| Exchange and transaction charges | Exchange, clearing and regulatory fees on your trades |

| Internet and phone | The connection you trade and research over |

| Charting, data and research tools | Subscriptions to charting platforms, data feeds, research |

| Chartered accountant fee | What you pay your CA to prepare and file the return |

| Laptop or computer depreciation | A yearly share of the cost of equipment used to trade |

A few of these deserve a word. STT, the tax charged on the trade itself, is treated as a deductible business expense for a trader, unlike for an investor. Equipment such as a laptop is not deducted all at once; instead you claim depreciation, which simply means writing off a portion of its cost each year over its useful life. Your CA will apply the correct rate.

Put together, these expenses can be meaningful. Imagine a trader with Rs 1,50,000 of net F&O profit who paid Rs 18,000 in brokerage and STT, Rs 12,000 for internet and a charting subscription, and Rs 8,000 to a CA, with another Rs 7,000 of laptop depreciation. That is Rs 45,000 of legitimate expenses. The trader is then taxed on Rs 1,50,000 minus 45,000, which is Rs 1,05,000, not the full Rs 1,50,000. At a 15% slab that single step saves roughly Rs 6,750 in tax, all of it perfectly legal.

The expense must be genuine and connected to your trading. A personal holiday is not an expense. A data subscription you actually use to trade is. If part of a cost is mixed, like a home internet bill used for both trading and personal browsing, claim only the reasonable trading share and let your CA guide the split.

Keep your proofs, or the deduction may not hold

A deduction you cannot prove is a deduction you can lose if you are ever asked. The fix is simple and it is a habit, not a project. Keep the paperwork as the year goes along.

Save your broker contract notes and the annual tax profit-and-loss report. Keep invoices for any tools, subscriptions and your CA fee. Hold on to bank and card statements that show the payments leaving your account. File them in one folder, digital or paper, so that at filing time everything is in one place and nothing is reconstructed from memory.

This matters for the turnover number too. The same broker report that proves your expenses also documents how your turnover was computed. If a question ever arises about whether you crossed an audit threshold, that report is your evidence that the figure was worked out the right way.

Anita's panic ended the moment she understood the difference. Her real turnover was modest, her net profit was a clear number she could plan around, and her year of brokerage, data and CA fees became deductions that lowered her tax. Nothing about her trading changed. Only her understanding did, and that is usually all it takes.

This chapter is for learning only and is not tax advice. Tax rules and turnover guidance can change, so please have a qualified chartered accountant confirm your turnover and expenses before you file.