Intraday Trading: Speculative Income

Buy and sell the same day and the tax rules change completely. Learn why intraday equity is speculative business income, how it is taxed at slab rates, and the strict rule that intraday losses can only offset intraday gains.

- ·Why intraday is speculative

- ·Taxed at your slab rate

- ·The strict loss set-off rule

- ·Four-year carry-forward

- ·Turnover for intraday

- ·A worked example

Rohan buys 100 shares of a fast moving stock at half past nine in the morning, watches it climb through lunch, and sells the lot before three in the afternoon. No shares ever settle into his account. The whole position opened and closed on the same day. He made a clean Rs 4,000, and he assumes the tax will work just like the capital gains his uncle pays on long-held shares. He is in for a surprise. What Rohan did has its own special tax label, and understanding that label is the difference between filing correctly and filing wrong.

When you buy and sell the same stock on the same day without taking delivery, that is intraday trading. The tax law does not treat it as an investment at all. It treats it as a particular kind of business, with its own rate, its own loss rules, and its own carry-forward period. This chapter unpacks all three in plain terms.

Why intraday equity is called speculative

Earlier in the course we sorted trading into three buckets. Delivery shares and mutual funds are capital gains. Futures and options are non-speculative business income. Intraday equity sits in the third bucket on its own, and the law gives it a slightly old fashioned name. It is speculative business income.

The logic is straightforward once you say it aloud. A speculative transaction, in the words of the law, is one settled without actual delivery of the shares. When you square off an intraday position the same day, no shares change hands. You simply pocket or pay the difference between your buy price and your sell price. Because nothing is delivered, the profit is speculative. It is still business income, but of a special speculative type.

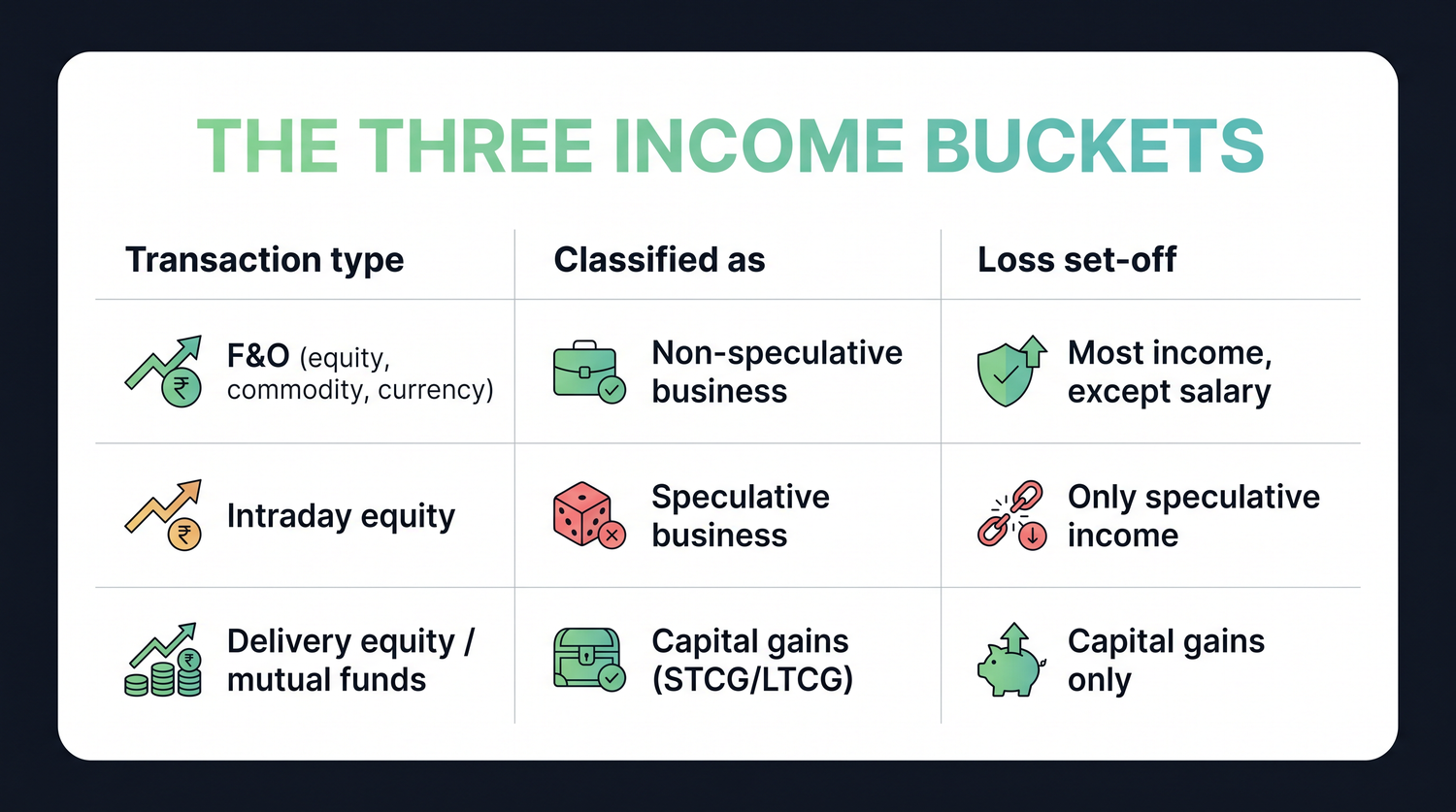

Intraday equity trading, where you buy and sell the same scrip on the same day with no delivery, is speculative business income. It is not capital gains and it is not the same bucket as futures and options. This single classification drives everything else in the chapter.

| Transaction type | Classified as | Loss can be set off against |

|---|---|---|

| Delivery equity and mutual funds | Capital gains | Capital gains only |

| Futures and options | Non-speculative business income | Most income heads, except salary |

| Intraday equity | Speculative business income | Only speculative income |

Taxed at your slab rate

Here is a piece of good news for the beginner who feared a scary special rate. Speculative business income is taxed at your normal slab rate. It simply adds to your total income for the year and is taxed along with everything else, according to the slab you fall into.

So if Rohan's only income were a modest salary that kept him in a low slab, his intraday profit would be taxed at that low slab rate. If he were a high earner already in the top slab, the same profit would be taxed at the top rate. There is no separate flat rate for intraday, unlike, say, crypto. It rides on your slab.

Over the financial year, Rohan's intraday trades add up to a net profit of Rs 1,20,000. He also earns a salary that places his marginal income in the 10 percent slab. His intraday profit is added to his total income and taxed at that slab. Tax on the 1,20,000 at 10 percent is Rs 12,000, plus the four percent cess. If instead his other income had pushed his margin into the 20 percent slab, the same 1,20,000 would attract Rs 24,000. The rate follows the person, not the trade.

Because it is business income, the usual business logic applies. Brokerage, Securities Transaction Tax on intraday sales, and other allowable trading charges can be deducted before arriving at the taxable profit. You report it as business income, not as capital gains, and most active traders use ITR-3 for this.

What counts as intraday, and what does not

It is worth drawing the boundary clearly, because the speculative label depends on one thing only. Was the position settled without delivery? If you buy a stock and sell it the same day so that no shares ever settle into your account, that is intraday and it is speculative. The moment shares are actually delivered to your account, the trade leaves the speculative bucket and becomes either a delivery investment or a delivery-based business trade, with their own rules.

A few common situations confuse beginners, so it helps to name them. If you buy today and the shares settle into your account, then sell tomorrow, that is a delivery trade, not intraday, because delivery took place. Futures and options, even when squared off the same day, are never speculative equity, because the law specifically treats them as non-speculative business. And selling shares you already hold in your account is a delivery sale, not an intraday short, because real shares moved. Speculative treatment is reserved narrowly for same-day equity positions that open and close without any delivery at all.

Why fuss over the boundary? Because the bucket decides the loss rules, and those rules are unforgiving, as we are about to see. Mislabel a delivery trade as speculative, or the reverse, and your set-off and carry-forward could be computed wrongly, which is the kind of error a later notice can expose.

The loss rule that catches people out

Now we reach the rule that surprises almost everyone, and it is worth slowing down for. A speculative loss can be set off only against speculative income. Nothing else.

Compare that with the other buckets. A non-speculative futures and options loss can be set off against most kinds of income, except salary. A capital loss can be set off against capital gains. But a speculative intraday loss is fenced in tightly. It cannot reduce your salary, it cannot reduce your delivery capital gains, and it cannot even reduce your futures and options profit. It can only be set off against other speculative income, which in practice means other intraday equity profit.

An intraday loss cannot be set off against your delivery investment gains, your salary, or your futures and options profit. It can only be set off against other speculative income. Treating intraday losses as freely adjustable against any income is a common and costly mistake.

If you cannot use the speculative loss this year, it does not vanish. It can be carried forward for four years and set off against speculative income in those future years. Note that four is shorter than the eight years allowed for ordinary business losses and capital losses. Speculative losses get the shortest leash. As with every loss carry-forward, you keep the right to carry it only if you file your return on time.

The carry-forward periods differ by bucket. Speculative losses carry forward four years. Non-speculative business losses and capital losses carry forward eight years. In every case, on-time filing is the price of admission. File late and the right to carry the loss forward is lost.

A case study that ties it together

Meet Sunita, who had a mixed year and shows exactly why these rules matter.

Sunita did three different things in the market during the year. Her intraday equity trading ended in a loss of Rs 50,000. Her delivery investing produced a short-term capital gain of Rs 80,000. And she also earned a salary.

Her instinct, like Rohan's, was to subtract the Rs 50,000 intraday loss from her Rs 80,000 delivery gain and pay tax on only Rs 30,000. That is not allowed. The intraday loss is speculative, and a speculative loss cannot touch her capital gains or her salary. So her Rs 80,000 short-term capital gain is taxed in full at its own rate, and her salary is taxed at her slab, untouched by the trading loss.

What happens to the Rs 50,000 intraday loss, then? It is not wasted, but it is parked. Sunita files her return on time, declares the speculative loss, and carries it forward for up to four years. If next year her intraday trading turns a profit of, say, Rs 30,000, she can set the carried loss against it and pay no tax on that Rs 30,000, leaving Rs 20,000 of loss still to carry. The loss is only ever useful against future speculative income, but reporting it on time is what keeps that option alive.

If you dabble in intraday alongside investing, keep the two records cleanly separate from day one. Tag every same-day square-off as speculative and every delivery trade as an investment. Your broker tax profit and loss statement usually splits these for you, which makes filing and any future set-off far simpler.

Step back and the shape of intraday tax is simple to hold in your head. Same-day equity trades are speculative business income. The profit is taxed at your ordinary slab rate and you may deduct trading charges against it. The loss is hemmed in, usable only against other speculative income, and it carries forward just four years, and only if you file on time. Knowing this keeps you from the twin traps of paying the wrong rate and wrongly netting an intraday loss against income it can never touch.

This chapter is educational only and not tax advice. The rules and rates can change with each Budget, so confirm your own situation with a qualified chartered accountant before you file.