The Trader's Year-Round Tax Checklist

Tax is won across the year, not the night before the deadline. Learn a simple month-by-month routine: pull your broker tax reports, track advance tax, keep expense proofs, reconcile with the AIS, and know when to bring in a chartered accountant.

- ·Pull your broker tax P&L

- ·Track advance tax quarterly

- ·Keep every expense proof

- ·Reconcile with the AIS

- ·Know when to hire a CA

- ·The final pre-filing checklist

For most traders, tax is something that happens in a panic. July arrives, the filing deadline looms, and suddenly you are hunting for statements you never saved, trying to remember a trade from eleven months ago, and praying the numbers add up. It is stressful, it is error-prone, and it is completely avoidable.

The traders who stay calm at filing time are not smarter or richer. They simply turned tax into a habit instead of an event. They keep a light, year-round routine, so that when the deadline comes, filing is just printing the answer to a sum they have been quietly working out all year. This final chapter hands you that routine: a month-by-month rhythm, the documents to reconcile, when to call in a professional, and a friendly checklist to run before you press submit. Let us turn tax from a yearly fright into a background task you barely notice.

The year-round mindset

The whole secret is this: a trader's tax return is built from records that only exist while the year is happening. Your turnover, your expenses, your advance tax, your foreign holdings, all of these are easy to capture in the moment and painful to reconstruct later. So the goal is not to "do your taxes" once a year. It is to spend a few minutes each quarter keeping your records current, so the return almost writes itself.

There are really only a handful of moving parts. You pull your numbers from your broker, you pay advance tax on time if you owe it, you keep your proofs in one place, you reconcile against what the department already knows, and you file on time on the right form. Master that loop and you have mastered the practical side of trading taxation.

Tax is a habit, not an event. Five quiet minutes each quarter saves five frantic hours in July, and far more than that if a mistake turns into a notice. The trader who records as they go is the trader who sleeps well at deadline time.

A month-by-month routine

You do not need to think about tax every day. You need a few anchor points in the year. Here is a simple calendar built around the four advance tax dates, which conveniently spread across the year and give you natural moments to tidy up.

| When | What to do |

|---|---|

| 15 June | Pay the first advance tax instalment if your net tax for the year is likely to exceed 10,000 rupees. Pull a fresh tax P&L from your broker for the start of the year. |

| 15 September | Pay the second advance tax instalment. Review your turnover so far and update your expense file. |

| 15 December | Pay the third instalment. Check whether your turnover is heading toward an audit threshold so there are no surprises. |

| 15 March | Pay the final instalment. Do a near-complete dry run of the year's profit, loss, and tax. |

| June to July (after year end) | Download your full-year broker tax P&L and turnover report, reconcile with the AIS and Form 26AS, then file ITR-3 on time. |

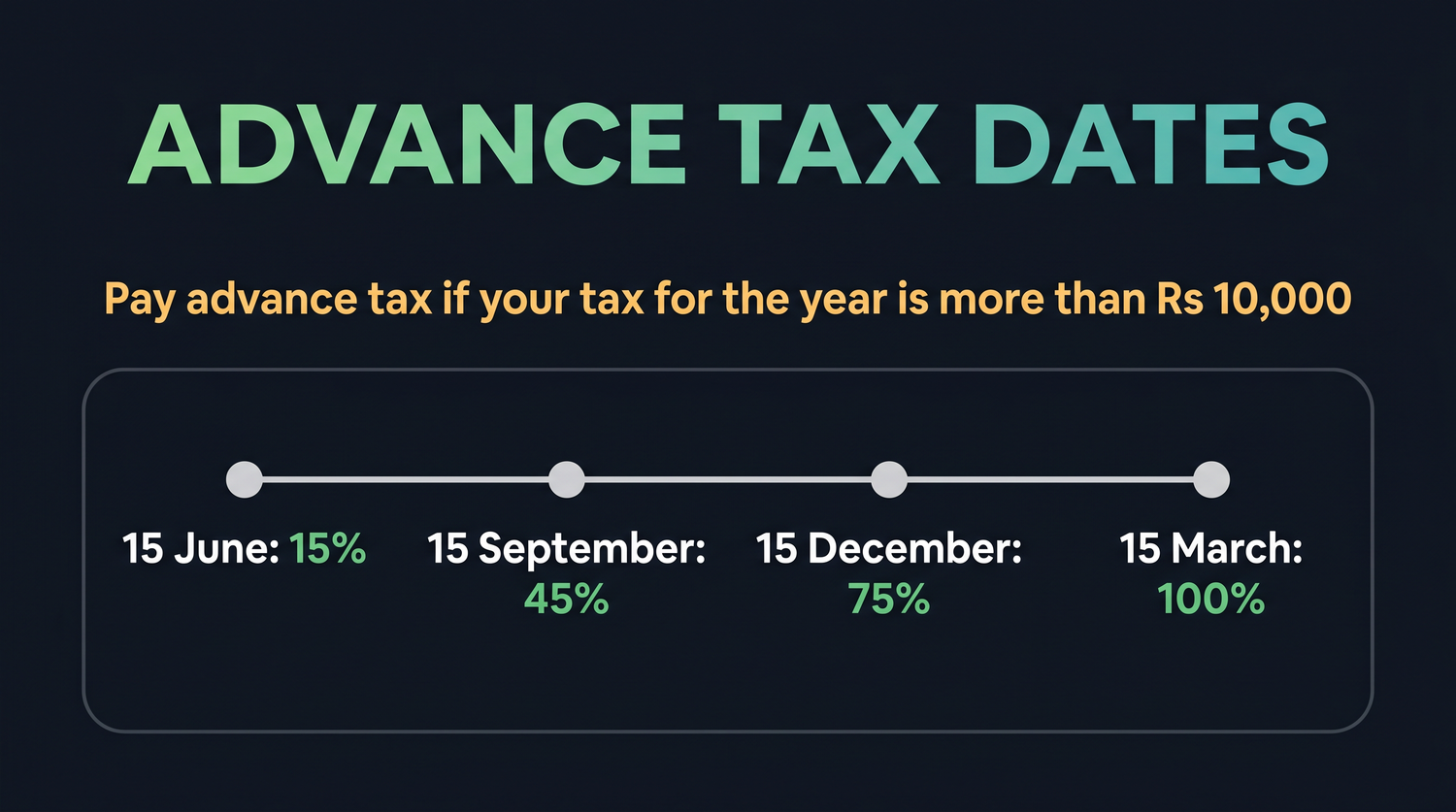

Advance tax is the part most beginners miss. If your net tax for the year is likely to be more than 10,000 rupees, you are expected to pay it in four instalments across the year, on 15 June, 15 September, 15 December, and 15 March, rather than all at once at the end. Paying on time avoids interest, and pegging your record-keeping to those same four dates means your books are never more than three months out of date.

Set four calendar reminders right now, one for each advance tax date. When each reminder fires, do two things in one sitting: pay any advance tax you owe, and download a fresh tax P&L from your broker. Two small tasks, four times a year, and your filing is already three-quarters done.

The four documents you reconcile

When the year ends, filing is mostly an act of reconciliation. You are checking that your own records agree with the records the department has already collected about you. Four documents do almost all the work.

Your broker tax P&L and turnover report is your starting point. Your broker prepares a statement that lays out your realised profits and losses and, importantly, your F&O turnover calculated the proper way, as the sum of favourable and unfavourable differences rather than the contract value. This is the backbone of your business income figure.

Your expense proofs are what let you reduce that business income legitimately. Keep every contract note, every invoice for software or services you use to trade, and your bank statements. These are deductible business expenses for a trader, but only if you can show them, so save them as the year goes.

The Annual Information Statement, the AIS, is the department's own picture of your financial year. It pulls together your trades, interest, dividends, and large transactions reported by banks, brokers, and others. The department tracks your trading turnover through STT and the AIS, so the figures you file should line up with what the AIS shows.

Form 26AS is your tax credit statement. It shows the tax already deducted or collected on your behalf, such as TDS and TCS, and the advance tax you paid. You reconcile it so that you claim every rupee of credit you are owed and so your final tax matches reality.

Do not report F&O as capital gains. This is the single most common and most costly mistake a trader makes. Futures and options are business income, reported in ITR-3, not short-term or long-term capital gains. Reporting it the wrong way invites a mismatch with the AIS and a notice, and it can make your return defective.

A 60-second reconciliation, in plain numbers. Suppose your broker tax P&L shows F&O turnover of 25,000 rupees, made up of a 12,000 profit, an 8,000 loss, and a 5,000 profit, for a net profit of 9,000 rupees. You open your AIS and confirm the trading activity it lists is consistent with that broker report. You open Form 26AS and confirm the advance tax you paid on the four dates is sitting there as credit. Three documents, one consistent story. When all three agree, you file with confidence instead of crossed fingers.

When to bring in a chartered accountant

Doing your own taxes is a fine goal, and for a salaried investor with simple capital gains it is very achievable. But trading adds wrinkles, and there are clear moments when a qualified chartered accountant earns their fee many times over. Call one in when any of these is true.

Bring in a CA when your turnover is large or an audit may apply, because the audit thresholds, the cash-receipt rules, and the turnover calculation itself reward professional care. Bring one in when you hold foreign assets, such as US shares or ETFs, because Schedule FA disclosure is mandatory even with no gain and the penalties for getting it wrong are severe. And bring one in when you deal in crypto, where the flat-rate rules, the no-set-off rules, and the unsettled treatment of crypto derivatives are genuinely tricky. In short, the moment turnover, audit, foreign assets, or crypto enters your year, a professional is not a luxury, it is sensible insurance.

One reason to never let the deadline slip: filing ITR-3 on time, by the due date, is what protects your loss carry-forward. If you trade and you made a loss, filing on time is exactly how you keep the right to set that loss against future profits, for up to eight assessment years for a non-speculative business loss. File late and you can forfeit that valuable carry-forward entirely.

The final pre-filing checklist

You have reached the end of the course, so let us bring it all together into one calm checklist to run before you submit your return. Tick each line and you have done the important things right.

| Check | Done when |

|---|---|

| Broker reports | You have downloaded the full-year tax P&L and turnover report from your broker. |

| Advance tax | You paid across the four dates if your net tax exceeded 10,000 rupees, and it shows in Form 26AS. |

| Expense proofs | Contract notes, invoices, and bank statements are saved and totalled. |

| Reconciliation | Your figures agree with the AIS and Form 26AS. |

| Right form | You are filing ITR-3 if you have F&O or intraday business income. |

| Right bucket | F&O is reported as business income, not as capital gains. |

| Foreign and crypto | Schedule FA and Schedule VDA are completed if they apply to you. |

| On time | You are filing by the due date to protect your loss carry-forward. |

| Professional check | A chartered accountant has reviewed it if turnover, audit, foreign assets, or crypto are involved. |

If you can tick every line of that checklist, you have done the hard part. Filing then becomes the easy part: entering numbers you already trust into the right form, on time. That is the whole game.

Here is the encouraging truth to carry out of this course. Tax felt scary at the start because it was unfamiliar, not because it was beyond you. You now understand the three income buckets, the slabs and the regimes, how capital gains and STT work, why F&O is business income, how turnover and audits are judged, how US stocks and foreign assets are treated, how crypto is taxed, which ITR form is yours, and how to keep a record all year so filing is painless. That is a real, practical command of the subject that most traders never bother to build.

You do not have to memorise every number. You only have to keep the habit, ask for help at the right moments, and file honestly and on time. Do that, and tax stops being the thing you dread and becomes just another part of being a serious, professional trader. Well done for seeing it through. Now go file with confidence.

This chapter, and this course, is for learning only and is not tax advice. Tax rules, rates, and forms change every year, so always confirm your specific situation with a qualified chartered accountant before you file for AY 2026-27.