Where to Put Your Money: The Asset Classes

Equity, debt, gold, real estate, cash and crypto, what each is, the risk-and-return trade-off, and why equities have historically built the most wealth.

- ·The major asset classes

- ·Risk vs return

- ·Equity, debt and gold

- ·Liquidity & taxation basics

- ·Where crypto fits

- ·Building a simple mix

Money cannot just sit there. The moment you have some savings, you face a quiet but unavoidable question: where should it live? A bank account, a fixed deposit, gold in a locker, a flat, a few shares, maybe a sliver of crypto, each is a different home for your money, with its own personality. Some homes are calm and safe but barely grow your money. Others grow it powerfully over decades but lurch up and down along the way.

These homes have a proper name: asset classes. There are really only a handful that matter, and once you understand the trade-offs between them, the entire world of investing stops looking like a casino and starts looking like a set of sensible choices. This chapter is your map of the territory, what each asset class is, how risky it is, what it has historically returned, and how quickly you can turn it back into cash.

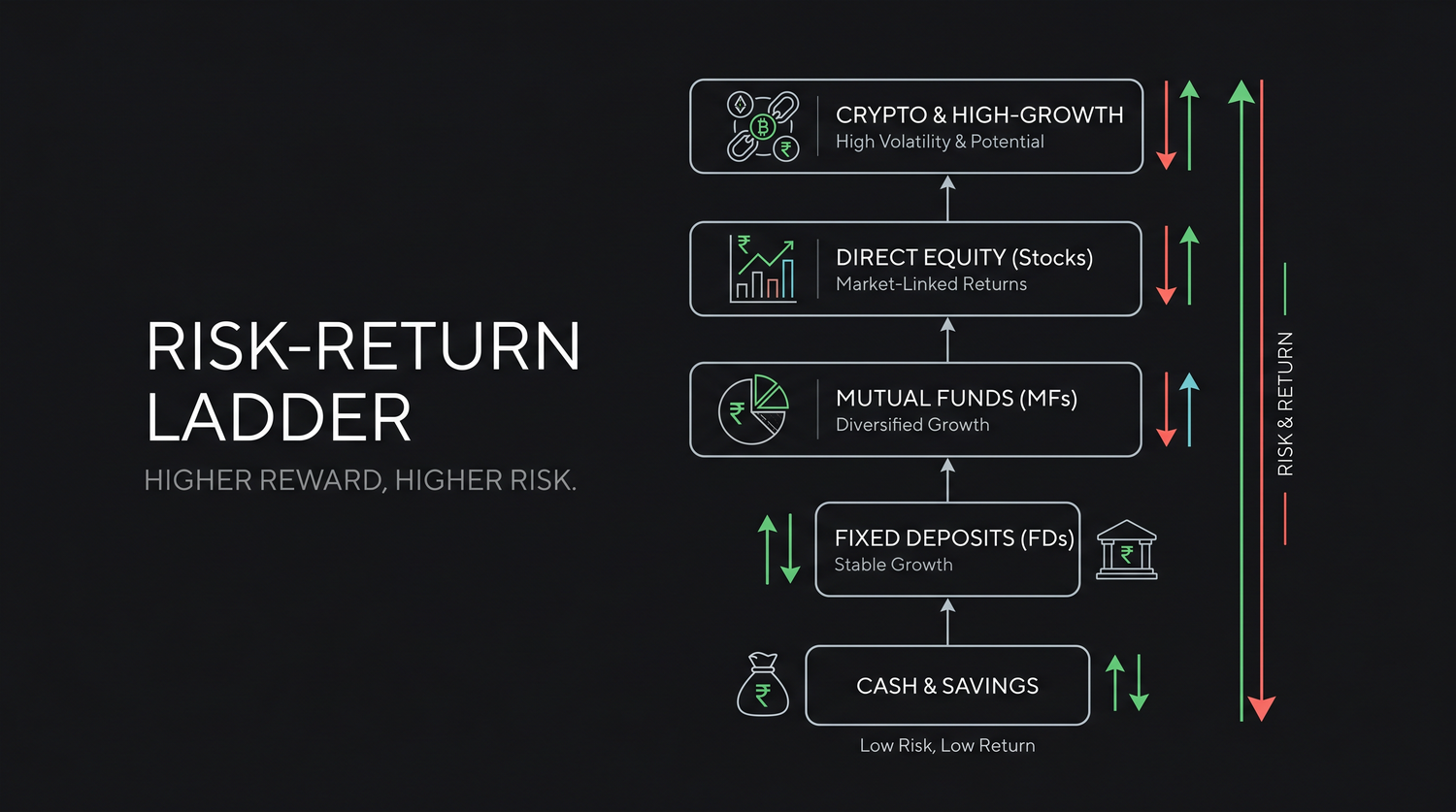

The handful of homes for your money

Strip away the jargon and almost everything you can invest in falls into one of six buckets:

- Equity (stocks), part-ownership of a real business. You profit as the business grows.

- Debt (FDs and bonds), you lend money to a bank, company or government and earn a fixed interest in return.

- Gold, a real, scarce metal people have trusted for 5,000 years; a hedge when everything else wobbles.

- Real estate, land and property, which can earn rent and rise in value.

- Cash (and savings accounts), money you can spend instantly, earning almost nothing.

- Crypto, digital assets like Bitcoin; new, borderless, and wildly volatile.

That is the whole menu. Everything fancier, mutual funds, ETFs, index funds, is just a convenient basket of these same building blocks.

The one rule that explains everything: risk vs return

Here is the single most important idea in investing, and it governs every asset above: higher potential return always comes bundled with higher risk. There is no asset that is both perfectly safe and highly rewarding. If someone offers you one, they are either mistaken or lying.

"Risk" here does not mean "you will definitely lose money." It means uncertainty, how much the value bounces around, and how wide the range of outcomes is. A fixed deposit has a tiny range (you know almost exactly what you will get). Equity has a huge range over a single year (it might rise 30% or fall 20%) but a much narrower, much higher range over a decade.

Picture the asset classes as rungs on a ladder. The lowest rungs are calm and safe but grow your money slowly. Climb higher and both the potential reward and the bumpiness increase together.

There is no free lunch in investing. Every extra rupee of expected return is paid for with an extra unit of risk. The skill is not avoiding risk, it is taking the right amount of risk for your goals and your timeline.

Liquidity: how fast can you get your cash back?

Return and risk are not the only things that differ. Liquidity, how quickly and cheaply you can convert an asset back into spendable cash, matters just as much, especially in an emergency.

- Cash is perfectly liquid, it is cash.

- Stocks are highly liquid, sell during market hours and the money reaches your bank in a day or so.

- Gold ETFs and FDs are fairly liquid; physical gold needs a buyer and a haircut on price.

- Real estate is the least liquid of all, selling a flat can take months and heavy paperwork.

A high return is cold comfort if your money is locked in a property when you suddenly need it. This is why your emergency fund always sits in cash or liquid options, never in property.

A one-line note on tax

Tax quietly eats into every return, and it differs by asset (rules are approximate and change with each Budget):

| Asset | How gains are taxed (approx., India) |

|---|---|

| Equity / equity funds | 12.5% long-term (held over 1 year, above Rs 1.25 lakh); 20% short-term |

| FDs / debt funds | Added to your income, taxed at your slab rate |

| Gold (ETF/funds) | 12.5% long-term after 24 months holding |

| Real estate | 12.5% long-term after 24 months |

| Crypto | Flat 30% on gains, plus 1% TDS, with no loss set-off |

Crypto is taxed more harshly in India than almost any other asset: a flat 30% on every gain, a 1% tax deducted at source on each sale, and, uniquely, you cannot offset your crypto losses against your crypto gains. The taxman shares your profits but not your pain.

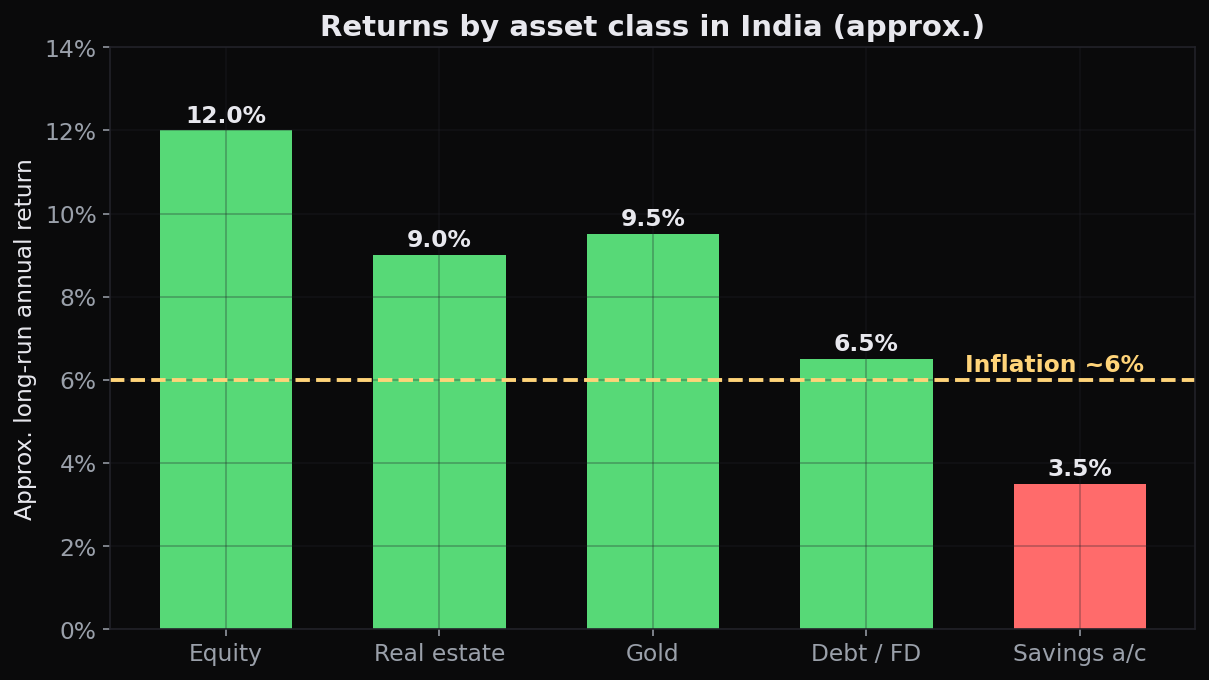

The big comparison, side by side

Now put it all together. The table below is the heart of this chapter, tape it to your wall. (Returns are long-run historical averages in rupees, are approximate, and never guaranteed.)

| Asset class | Typical risk | Typical long-run return (approx.) | Liquidity |

|---|---|---|---|

| Cash / savings | Very low | 3-4% | Instant |

| Debt (FDs, bonds) | Low | 6-7% | Medium-High |

| Gold | Medium | 8-10% | Medium-High |

| Real estate | Medium-High | 7-9% (plus rent) | Very low |

| Equity (stocks) | High (short term) | ~12% | High |

| Crypto | Very high | Unknown, extreme swings | High |

Read the equity row carefully. It carries the highest short-term risk yet the highest long-run return, and that is exactly the bargain we met in Chapter 1: accept the bumps over months, and equity has historically rewarded you the most over decades.

Why equity has built the most wealth

Over long stretches, no mainstream Indian asset has matched equity. The reason is simple and powerful: when you own a stock, you own a slice of a living, growing business that reinvests its profits, expands, raises prices with inflation, and compounds its earnings year after year. Gold just sits in a vault; a good company works for you.

The proof is in the headline index itself. The BSE Sensex began in 1979 at a base value of 100. Today it trades around 76,000-77,000. A flat that cost a few lakh in 1979 has not multiplied anywhere near as much.

From a base of 100 in 1979 to roughly 77,000 today, the Sensex has multiplied about 770 times in around 45 years. That is the quiet power of owning businesses and letting them compound, the kind of growth no locker full of gold has ever delivered.

The recent picture: gold's golden run and crypto's wild ride

Investing is not a museum, the asset classes are alive and moving, and the last two years have been dramatic.

Gold has had a spectacular run. It rose roughly 27% in 2024 and surged further through 2025, hitting record after record, MCX gold crossed Rs 1,23,000 per 10 grams, and internationally gold passed $4,000 an ounce for the first time in history. The drivers: global uncertainty, wars, and central banks around the world buying gold to lean less on the US dollar. Gold's job in a portfolio is exactly this, to shine when nervousness spikes.

One change to note: the popular Sovereign Gold Bonds (SGBs), government bonds that tracked the gold price and paid 2.5% annual interest, were discontinued in the 2025 Budget, with no new tranches being issued. Investors who already hold them keep earning interest until maturity, but new buyers must now use gold ETFs or gold funds instead.

Crypto, meanwhile, remains the wildest rung on the ladder. Bitcoin can swing 10% in a day and has, in past cycles, fallen 70%+ from its peaks before recovering. It produces no profits, pays no dividend, and has no long-run track record, so treat it as a tiny, speculative slice you can afford to lose, never the foundation of your wealth.

A common beginner mistake is chasing whatever rose most last year. Gold's huge 2024-25 run does not guarantee a repeat, just as crypto's past rallies were followed by brutal crashes. Past performance is a story, not a promise. Diversify instead of sprinting after the latest winner.

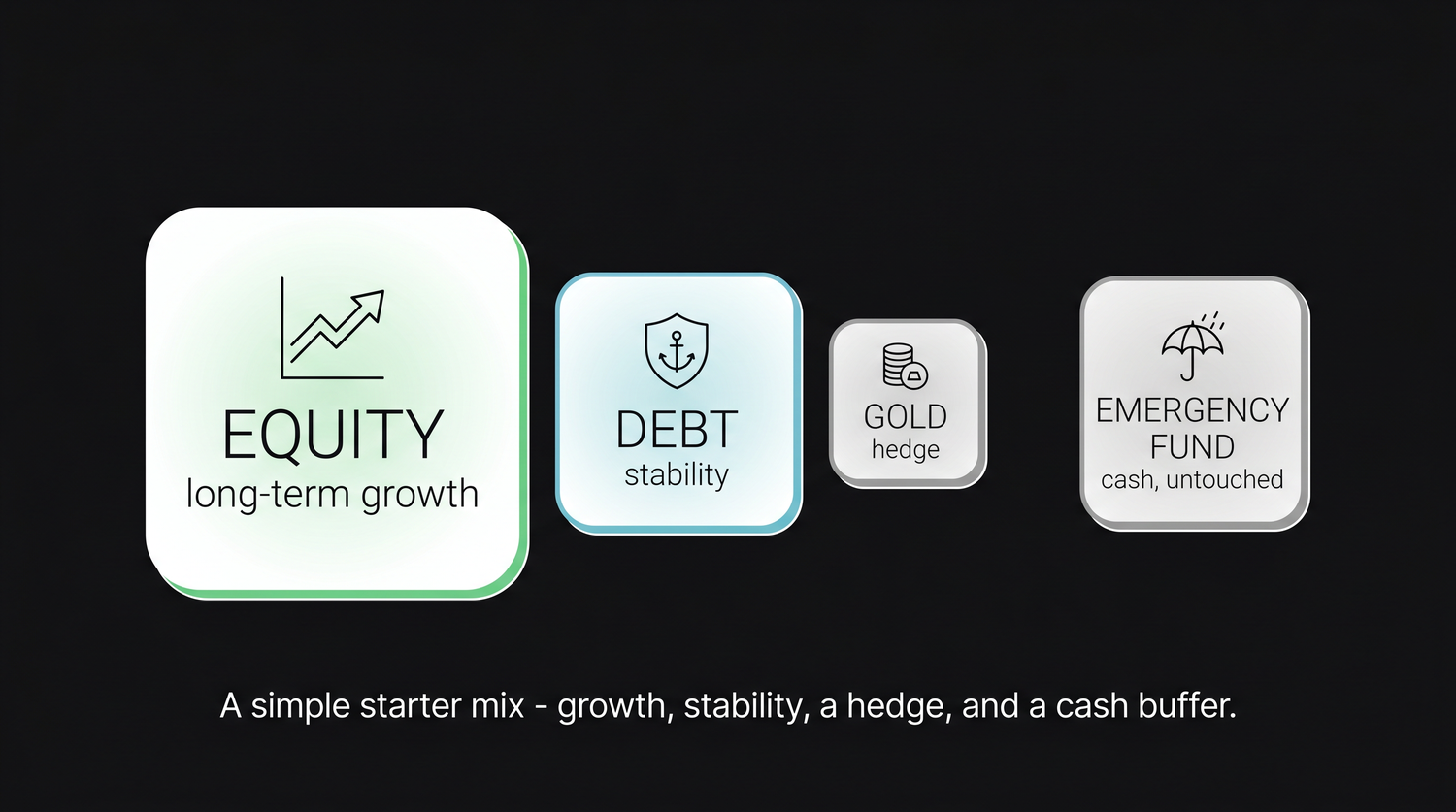

Building a simple mix

You do not have to pick one home for all your money, in fact, you should not. Spreading money across asset classes is called asset allocation, and it is your seatbelt: when one zigs, another often zags. A common, sensible starting framework (an illustration, not advice) ties your equity share to your timeline, the longer until you need the money, the more equity you can stomach.

A classic rule of thumb says keep roughly "(100 minus your age)%" in equity, so a 25-year-old might hold ~75% in equity, the rest in debt and a little gold. It is only a starting point, not a law, but it captures the right instinct: the young, with time on their side, can afford to ride equity's waves.

The exact percentages matter far less than the habit: keep an emergency fund in cash, lean on equity for long-term growth, hold some debt for stability, and add a little gold as insurance.

Quick recap

- Your money lives in asset classes, equity, debt, gold, real estate, cash and crypto, each with its own personality.

- The master rule is risk vs return: higher potential reward always rides alongside higher risk. There is no free lunch.

- Liquidity decides how fast you can get cash back, stocks and FDs are quick, real estate is slow; keep emergencies in cash.

- Equity carries the most short-term bumpiness but has historically built the most wealth, because you own growing businesses.

- Gold had a record 2024-25 run as a safe haven (note: SGBs are now discontinued), while crypto stays extremely volatile and is taxed at a flat 30%.

- Asset allocation, spreading money sensibly across classes, is your seatbelt; the habit matters more than the exact percentages.

Now that you know where money can grow, let us zoom into the most powerful home of all, the stock market, and answer the most basic question of all: what is a share, really?