SEBI & the Guardians of the Market

Markets only work when they are fair. Meet SEBI, RBI and the rules that protect you, and why regulation exists, told through the scandals that created it.

- ·Who regulates the markets

- ·What SEBI does

- ·RBI's role

- ·Investor protection

- ·Why rules exist (the scandals)

- ·How complaints are handled

Imagine a cricket match with no umpire. No one to call a no-ball, no one to give a batsman out, no one to stop a bowler from tampering with the ball. Within minutes the game would collapse, not because the players are bad people, but because without a fair referee, nobody can trust the result. The stock market is exactly the same. It moves trillions of rupees between millions of strangers who will never meet. The only reason you are willing to send your hard-earned money into a screen and trust that real shares land in your account is that someone is watching, enforcing the rules, and punishing cheats.

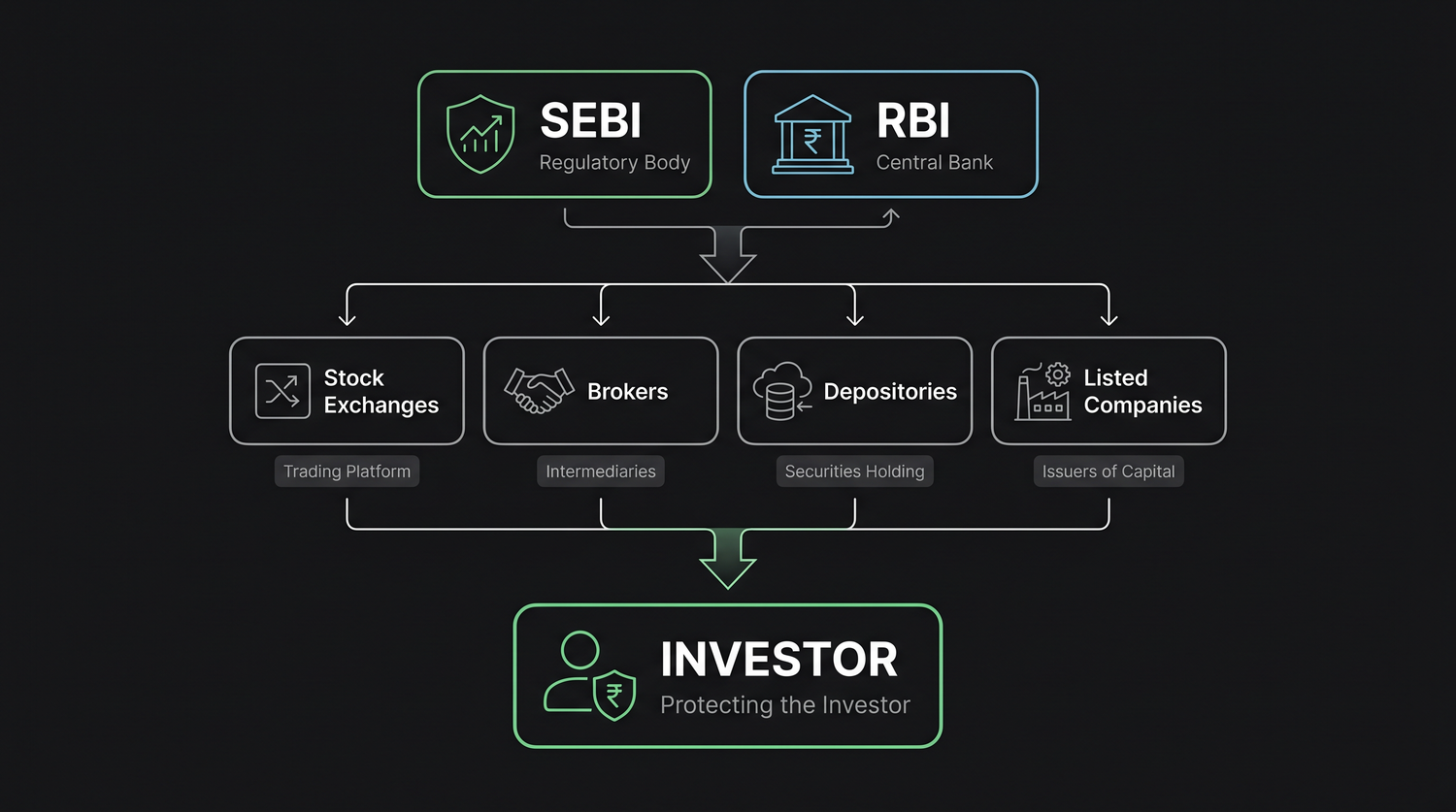

That someone, in India, is mainly SEBI, the Securities and Exchange Board of India, backed up by the RBI. This chapter introduces the guardians of the market: who they are, what they actually do in plain English, how they protect ordinary investors like you, and the dramatic scandal that gave SEBI its real powers. Because here is the uncomfortable truth, market regulation is written in the ink of past disasters.

Why markets must be regulated

Trust is the invisible foundation of every market. You will happily buy shares only if you believe a handful of things are true: that the company's reported profits are real and not fabricated, that the price is set by honest supply and demand rather than a manipulator, that your broker will not run off with your money, and that the shares you paid for will actually appear in your account.

Take away any one of those, and the whole system freezes. Nobody invests in a game they suspect is rigged. So regulation is not red tape that gets in the way of the market, regulation is what makes the market possible at all. It converts a den of suspicion into a place where a 22-year-old in a small town can confidently own a piece of India's biggest companies.

Regulation exists for one reason above all: trust. Fair rules, honest prices and protected investors are not a nice extra, they are the oxygen the market breathes. Without them, no rational person would ever invest, and there would be no market to speak of.

Meet SEBI, the market's chief referee

SEBI is the main regulator of India's securities markets, stocks, bonds, mutual funds, derivatives, the lot. Think of it as the umpire, the rule-maker and the police force of the market rolled into one. Its job, in plain terms, is to keep the market fair, transparent and safe for ordinary investors. It does this through three broad roles:

- Protecting investors. SEBI's stated first priority is the small investor, making sure you are treated fairly and not fleeced by those with more information or power.

- Regulating the players. Stock exchanges, brokers, mutual funds, rating agencies, investment advisers, all must register with SEBI and follow its rules. Break them and SEBI can fine you, ban you, or hand the case to the courts.

- Developing the market. SEBI also modernises the market, pushing reforms like faster settlement, electronic shareholding and tighter disclosure, so India's markets stay world-class.

A huge part of SEBI's power is the rule of disclosure: companies must publicly reveal their financial results, major decisions and risks, so that every investor decides using the same facts. No secret information for insiders, no hiding bad news. Sunlight, SEBI believes, is the best disinfectant.

The RBI: guardian of money and banks

If SEBI guards the markets, the Reserve Bank of India (RBI) guards the money and the banks behind them. The RBI is India's central bank, and while it does not police your stock trades, its decisions ripple through every market.

The RBI's main jobs are to issue the rupee, control inflation by setting interest rates, regulate the banks (including the one holding your account), and manage the country's foreign exchange. When the RBI raises or cuts the repo rate, it changes the cost of borrowing across the whole economy, which moves FD rates, loan EMIs and, indirectly, stock prices.

A simple way to remember the split: SEBI watches the share market; the RBI watches the banking and money system. They overlap at the edges, for instance, both have a say in market infrastructure, but their core beats are different. SEBI protects your investments; the RBI protects your rupee and the banks that hold it.

How investors are protected

SEBI's investor-protection toolkit is genuinely useful, and as a beginner you should know what stands between you and the sharks:

- Fair rules that ban insider trading, price manipulation and misleading advertisements.

- Mandatory disclosure, so companies cannot hide their true financial state.

- Segregation of your assets, your shares are held in your own demat account at a depository, not pooled where a broker could misuse them.

- Action against fraud, investigations, heavy fines, bans from the market and referrals for prosecution.

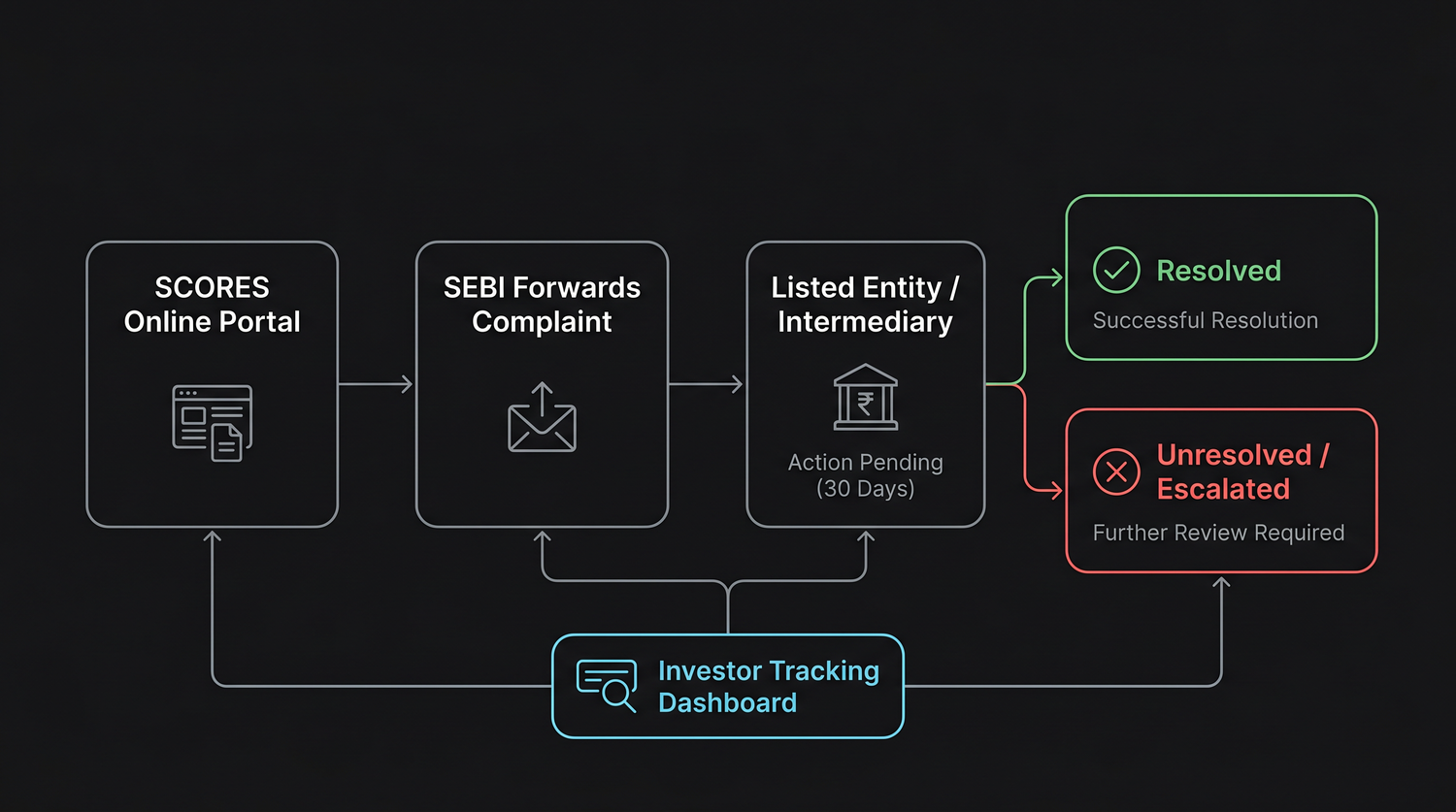

- A complaint system, the official SCORES platform, where any investor can formally raise a grievance and track it.

SCORES: your formal complaint channel

If a broker, company or mutual fund wrongs you and won't fix it, you do not have to beg or give up. SCORES (SEBI Complaints Redress System) is a free online portal where you lodge a complaint, which SEBI then routes to the offending entity with a deadline to respond, and you can track the status the whole way.

Before you ever invest a rupee, check that whoever you are dealing with, broker, adviser, mutual fund, is registered with SEBI (you can verify this on SEBI's website). A SEBI registration number is not a guarantee of profits, but dealing with registered, accountable entities is your first and cheapest line of defence against fraud.

Written in the ink of scandal: the Harshad Mehta story

Here is the part most people do not know: SEBI existed on paper from 1988 but had almost no real power, it was a toothless advisory body. What gave it teeth was a catastrophe.

In 1992, stockbroker Harshad Mehta, nicknamed the "Big Bull", was found to have siphoned an estimated Rs 4,000 crore out of the banking system using fake receipts, and funnelled it into a handful of stocks, ramping their prices to dizzying heights. When the scam unravelled, the market crashed, ordinary investors were wiped out, and public trust collapsed. The country realised, painfully, that it had no real cop on the beat.

The response was the SEBI Act of 1992, which transformed SEBI from a powerless committee into a statutory regulator with the authority to investigate, fine and ban. Nearly every major protection you enjoy today, dematerialised shares, faster settlement, strict disclosure, traces back, directly or indirectly, to the lessons of that scandal.

Almost every major Indian market reform was born from a disaster. The 1992 Harshad Mehta scam gave SEBI its statutory teeth; the 2001 Ketan Parekh scam tightened settlement and banned the risky "badla" system; the 2009 Satyam fraud overhauled corporate-governance rules. The rulebook protecting you today is, quite literally, written in the ink of yesterday's scams.

The modern frontier: finfluencers and F&O

The guardians are still very much at work, and the battlefield has moved to your phone. Two recent crackdowns show SEBI adapting to new dangers.

First, finfluencers. As social media filled with self-styled "experts" pushing stock tips, courses and "guaranteed" strategies, SEBI moved in. From early 2025 it barred registered entities (brokers, mutual funds, advisers) from associating with unregistered finfluencers, and restricted educators from using recent live market data to disguise tips as "education." The message is blunt: giving specific stock advice without a SEBI registration is illegal, however many followers you have.

Second, the futures and options (F&O) clampdown. SEBI's own research delivered a sobering verdict: roughly 91% of individual F&O traders lost money in FY25, with net losses of about Rs 1.05 lakh crore in a single year. In response, SEBI tightened the rules, fewer weekly expiries, bigger minimum contract sizes and stricter monitoring, specifically to keep small investors from being lured into a game where the overwhelming majority lose.

Beware anyone online promising "sure-shot" tips, guaranteed returns or get-rich-quick F&O strategies, especially in private WhatsApp or Telegram groups. SEBI's data is brutally clear: the vast majority of fast-trading retail participants lose money. A regulator can punish fraud after the fact, but only you can avoid the trap in the first place. Scepticism is your strongest protection.

Quick recap

- Markets run on trust, and regulation is what creates it, without fair rules and honest prices, no one would invest at all.

- SEBI is the chief referee of India's securities markets, protecting investors, regulating brokers and exchanges, and enforcing strict disclosure.

- The RBI guards money and banks, setting interest rates that ripple through every market; SEBI watches shares, the RBI watches the rupee.

- Investors are protected by fair rules, mandatory disclosure, segregated demat holdings, anti-fraud action, and the SCORES complaint platform.

- SEBI got its real statutory powers from the SEBI Act of 1992, passed after the Harshad Mehta scam, reforms are written in the ink of past scandals.

- Today SEBI is cracking down on unregistered finfluencers and tightening F&O rules after finding that ~91% of individual derivatives traders lose money.

You now know who keeps the market honest. Next, we tour the machinery itself, the exchanges, brokers and depositories that take your click and turn it into real, safely-held ownership.