Exchanges, Brokers & Depositories

From NSE and BSE to your demat account at NSDL or CDSL, the cast of intermediaries that route, hold and safeguard your shares.

- ·NSE & BSE exchanges

- ·The role of brokers

- ·Demat & depositories (NSDL/CDSL)

- ·Clearing corporations

- ·Discount vs full-service

- ·What each one charges

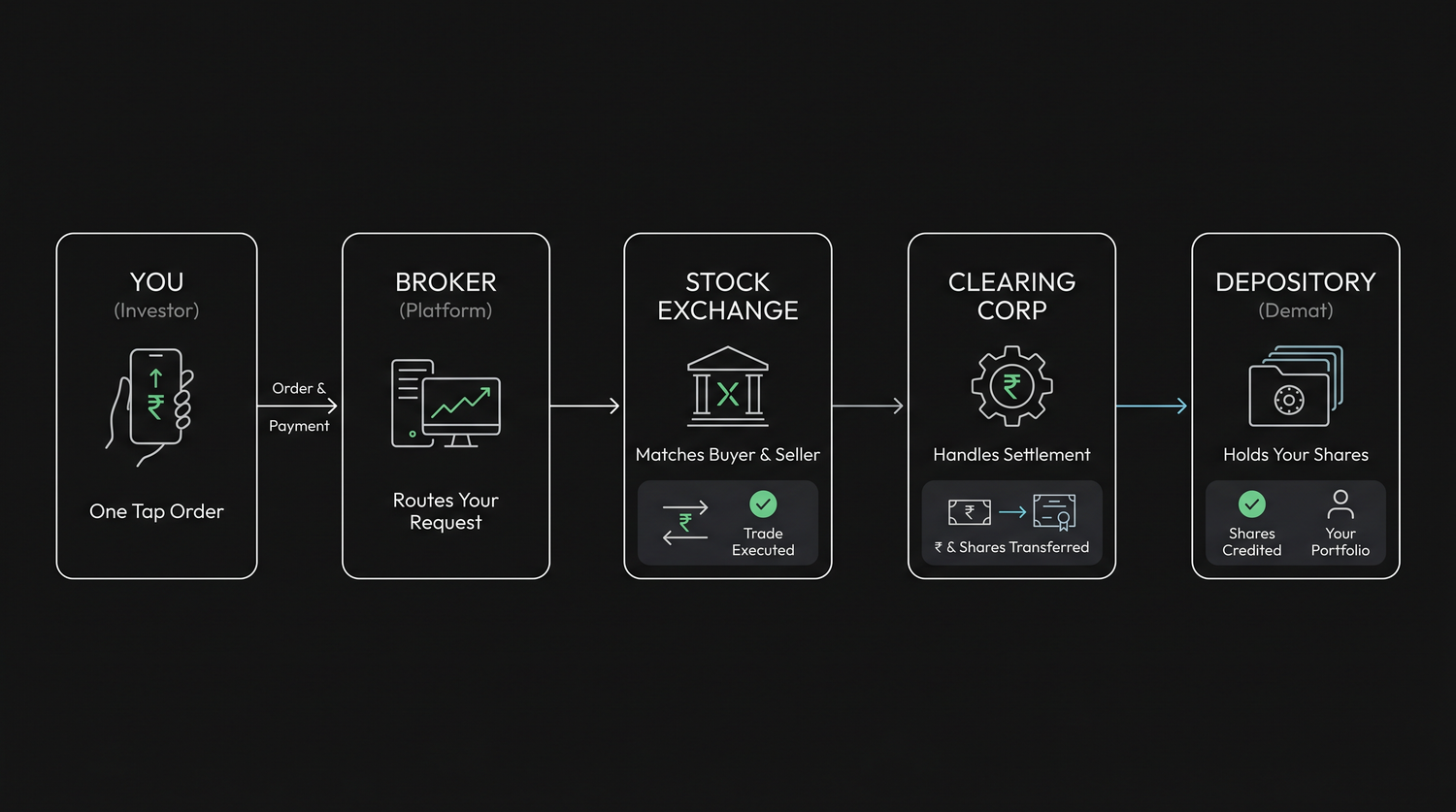

When you tap "Buy" on 10 shares of Reliance and the order fills in under a second, it feels like magic, one tap, done. But that single tap quietly sets off a relay race between four very different institutions, each with one job, each handing the baton to the next. None of them is you, none of them is the company you just bought, and yet without all four working together your trade simply could not happen, and your shares could not be safely held.

This chapter introduces that cast of characters: the exchanges where buyers and sellers meet, the broker who carries your order there, the depository that holds your shares electronically, and the clearing corporation that guarantees nobody gets cheated. Understand these four and the stock market stops feeling like a black box and starts looking like a remarkably well-organised assembly line.

The exchange: a giant organised marketplace

A stock exchange is simply a marketplace, but instead of vegetables or gold, the thing being bought and sold is ownership in companies. It is the place where someone wanting to sell 10 shares of Reliance is matched with someone wanting to buy them, at a price both agree on. The exchange does not own the shares or set the price; it runs the auction, matches orders, and publishes every trade so the whole market sees the same fair price.

India has two main stock exchanges, and they could not have more different backstories.

- The Bombay Stock Exchange (BSE), founded in 1875, is Asia's oldest stock exchange. It began under a banyan tree where a handful of stockbrokers met to trade, and today lists thousands of companies, more than any other exchange in India.

- The National Stock Exchange (NSE), launched in 1994, is the newer, fully electronic exchange. It is the larger of the two by trading volume, the vast majority of India's cash-market and derivatives turnover happens here.

The BSE began in 1875 under a banyan tree on what is now Dalal Street in Mumbai, where brokers literally gathered in the open to trade. "Dalal Street" has since become shorthand for the entire Indian stock market, the way "Wall Street" stands in for America's.

When the market is open

You cannot buy or sell a share at any hour you like. A trade only happens while the exchange is open, and India's equity market keeps regular office hours (IST):

- Normal trading: 9:15 AM to 3:30 PM, Monday to Friday. This is when almost all buying and selling happens.

- Pre-open: 9:00 to 9:15 AM, a short window where orders are collected and a fair opening price is discovered through an auction, so the day does not begin with a chaotic jump.

- Post-close: 3:40 to 4:00 PM, a brief window to place orders at the day's closing price.

- The market is shut on weekends and exchange holidays, though you will occasionally hear of a special one-hour Muhurat session on Diwali evening.

So if you tap Buy at 9 PM or on a Sunday, nothing executes, your order simply waits. Most apps let you place an after-market order (AMO) that queues up and is sent the instant the market next opens. The price you finally get is whatever the market is doing then, not when you placed it.

A share has no live price while the market is closed. The "last traded price" you see at night is just the final price from the last open session, frozen until 9:15 AM the next trading day. Real buying and selling can only happen during market hours.

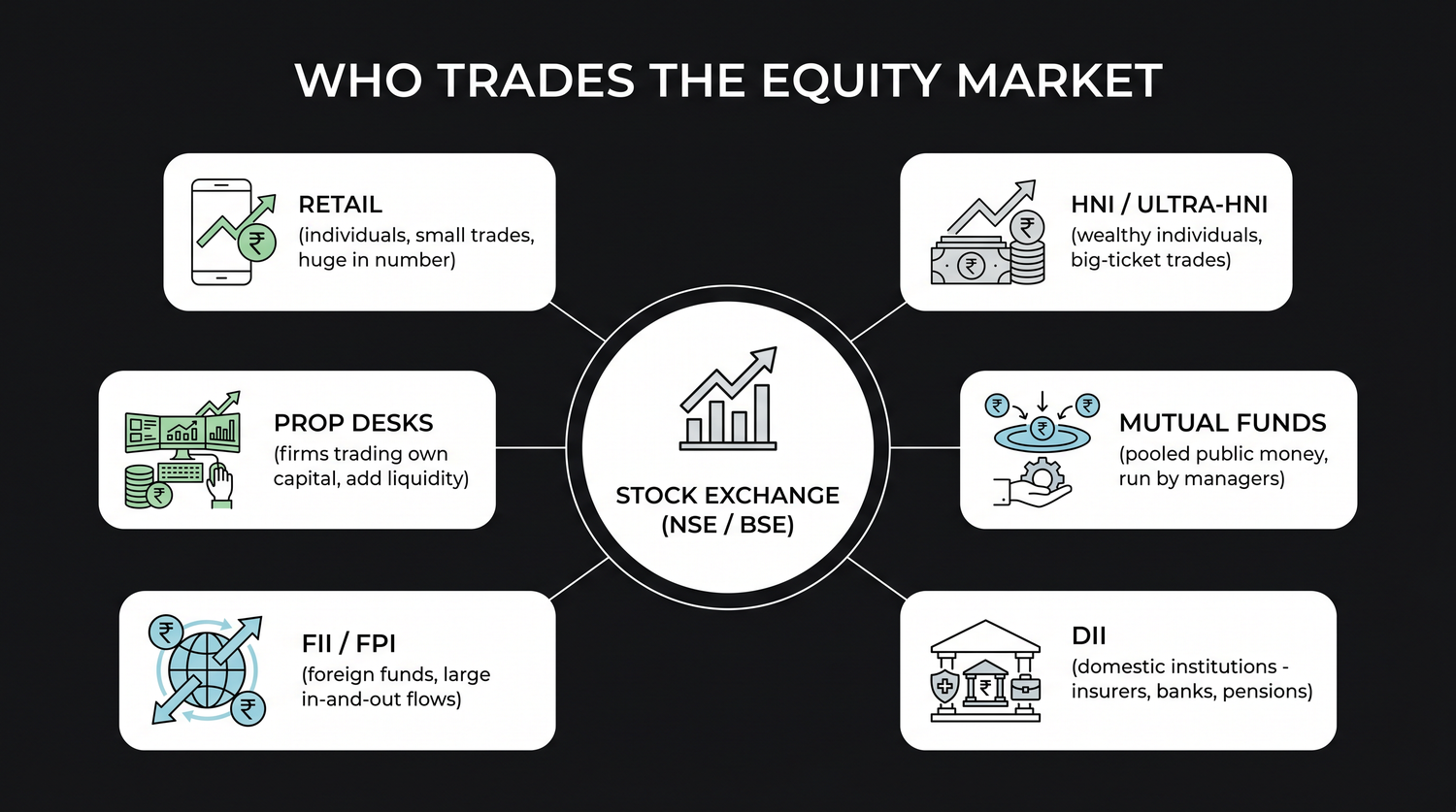

Who is trading: the market participants

When you buy a share, someone on the other side is selling it, but who are all these buyers and sellers? The equity market is a crowd of very different players, each with different goals, sizes and time horizons.

| Participant | Who they are | What they do in the market |

|---|---|---|

| Retail investors | Individuals like you, trading from a phone or laptop | Buy and sell in small amounts, tiny per trade, but enormous in total numbers |

| HNIs / Ultra-HNIs | High-net-worth individuals investing large sums | Big-ticket trades, often via PMS or AIFs; can move smaller stocks on their own |

| Mutual funds | Pools of many people's money run by professional managers | Invest your SIPs and lump sums across stocks, a huge, steady domestic force |

| DIIs (domestic institutions) | Indian mutual funds, insurers (such as LIC), banks, pension funds | Deploy domestic savings; in recent years they have cushioned the market when foreigners sell |

| FIIs / FPIs (foreign investors) | Large overseas funds investing in India | Move huge sums in and out; their "risk-on / risk-off" mood can swing the indices sharply |

| Proprietary (prop) desks | Brokerages and trading firms trading their own capital | Fast, high-volume trading and arbitrage that adds liquidity, so your order finds a match in milliseconds |

A few patterns are worth remembering. FIIs and DIIs are the heavyweights, when these institutions move billions, the whole index feels it (the FII-versus-DII tug-of-war returns in the macro chapter). Retail is mighty in numbers but small per trade. And prop and high-frequency desks are the quiet plumbing that keeps prices tight and trades filling instantly. Every time you buy, you are likely trading against one of these players, usually without ever knowing which.

The broker: your gateway to the exchange

Here is a catch: you cannot walk up to the NSE or BSE and place an order yourself. Only registered members, brokers, are allowed to send orders to the exchange. So a broker is your gateway. When you tap Buy in an app, that order travels to your broker, who routes it to the exchange in milliseconds. The broker is your licensed middleman, and for that service they charge a fee called brokerage.

Brokers come in two broad flavours:

| Discount broker | Full-service broker | |

|---|---|---|

| What they offer | A no-frills app to place trades | Trades plus research, tips, a relationship manager, advice |

| Brokerage | Flat, low (often a small fixed fee per order, or zero on delivery) | Usually a percentage of each trade's value |

| Best for | Self-directed investors who decide themselves | People who want hand-holding and advice |

The rise of low-cost discount brokers, charging a flat fee like roughly Rs 20 per executed order instead of a percentage, is a big reason a whole generation of young Indians started investing. It made buying a few shares genuinely cheap.

A common beginner mistake is thinking brokerage is the only cost. It is usually the smallest part. Every trade also carries statutory charges, and for tiny trades, these can add up to more than the brokerage itself. Always look at the total cost, not just the brokerage line.

What you actually pay on a trade

Beyond brokerage, a basket of small charges and taxes rides along on every trade. You do not pay these to your broker as profit, the broker simply collects most of them and passes them to the government or the exchange. The main ones, all approximate:

- Securities Transaction Tax (STT), a government tax on the trade value.

- Exchange transaction charges, a tiny fee the exchange takes for the match.

- GST, 18% charged on the brokerage and transaction charges.

- Stamp duty, a small state levy on buys.

- SEBI turnover fees, a minuscule charge funding the regulator.

- DP charges, a flat fee (often around Rs 13-20) when shares leave your demat account on a sell.

The headline takeaway: brokerage may be advertised as "zero," but a trade is never truly free. The good news is that for a long-term investor buying and holding, these costs are paid rarely and matter little.

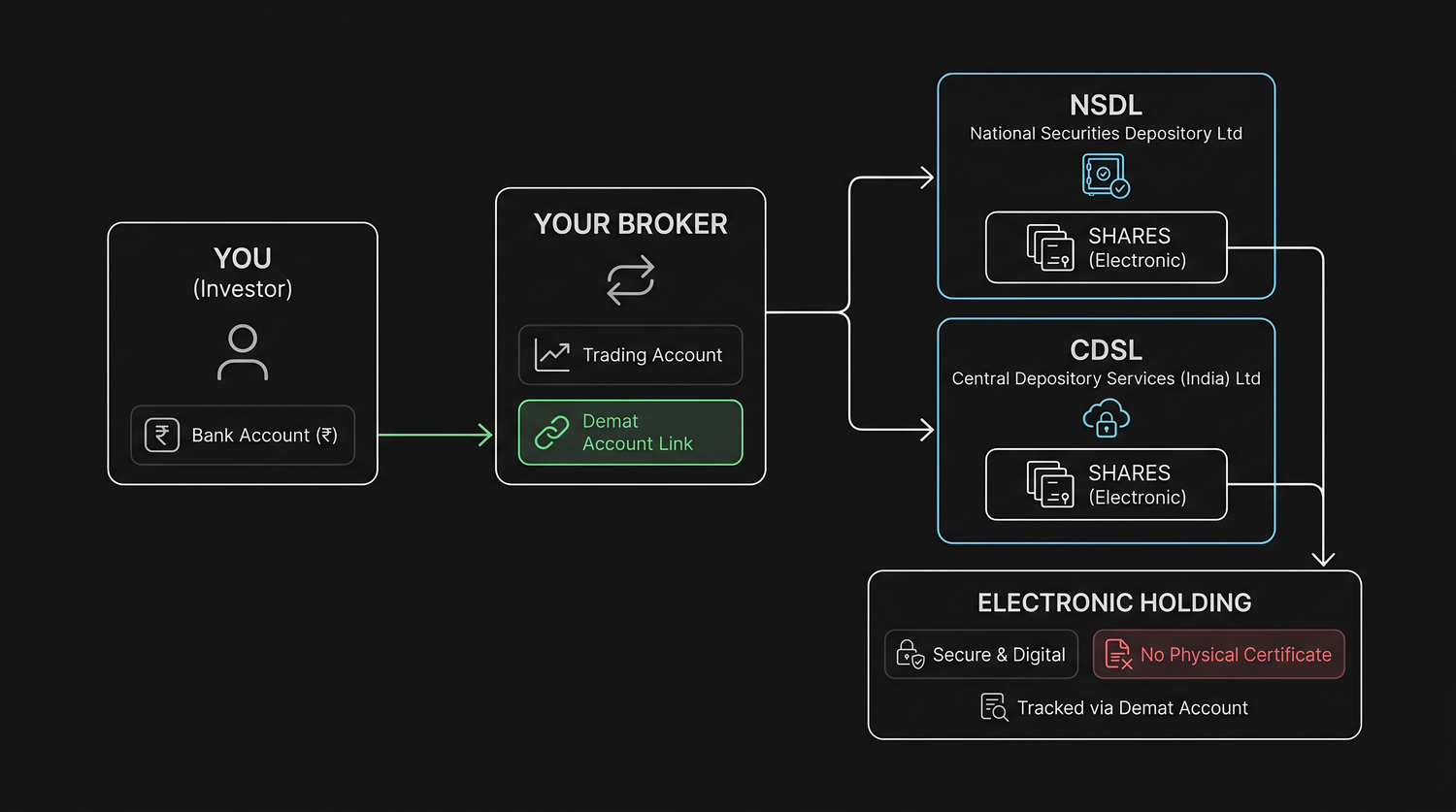

The depository: a bank for your shares

Once you buy shares, where do they actually live? Not in your broker's app, that is just a window. They live in a demat account, held at a depository. Think of a depository as a bank, but instead of holding rupees it holds your shares electronically. Just as your bank account shows your money as a number on a screen, your demat account shows your shares as electronic entries. "Demat" is short for dematerialised, meaning the shares exist as data, not paper.

India has exactly two depositories:

- NSDL, the National Securities Depository Limited, India's first, set up in 1996.

- CDSL, the Central Depository Services Limited.

You never deal with them directly. Your broker acts as a Depository Participant (DP), the bridge between you and the depository, and opens your demat account on one of the two. Your shares sit safely at NSDL or CDSL regardless of what happens to your broker's app.

The demat revolution

This electronic world is surprisingly recent. Until the late 1990s, owning a share meant holding a physical paper certificate. Selling meant couriering that certificate across the country with a signed transfer form, waiting weeks for it to be registered, and praying it did not get lost, torn, forged or stuck in "bad delivery" disputes. Settlement could take months. Fraud was rampant.

The launch of NSDL in 1996 began the demat revolution, converting paper certificates into electronic records. It transformed Indian markets from slow and risky to fast and safe, and is one of the biggest reasons ordinary people can now invest with a few taps. Today, holding physical share certificates is essentially extinct.

Your shares are held at a depository (NSDL or CDSL), not by your broker. The broker is only the access point. This separation is a deliberate safety design: even if your broker shut down tomorrow, your shares would still be safe in your demat account at the depository.

Types of demat account

Not every demat account is the same. Depending on who you are and what you need, you open one of a handful of standard types. Here are the common ones in India:

| Demat account type | Suitable for | Key feature |

|---|---|---|

| Regular | Resident individuals | Unlimited holdings |

| Joint | Family / business partners | Shared control |

| Corporate | Companies, LLPs | Legal-entity compliance |

| NRI Repatriable | NRIs with an NRE bank account | Funds can be transferred abroad |

| NRI Non-Repatriable | NRIs with an NRO account | Funds stay within India |

| BSDA (Basic Services) | Small / beginner investors | Low or zero AMC, with holding limits |

| Custodial | Minors, via a guardian | Operated by a guardian |

| Premium | HNIs and frequent traders | Extra services and support |

If you are just starting out and will hold only a small amount, ask for a BSDA, a Basic Services Demat Account. SEBI designed it for small investors: the yearly maintenance charge (AMC) is zero for holdings up to Rs 4 lakh and only a small fee up to Rs 10 lakh, so you are not paying annual fees while your portfolio is still tiny. You may hold only one BSDA and it must be your only demat account, which is exactly right for a beginner.

The clearing corporation: the guarantor in the middle

There is one last, quiet hero. When you buy and someone else sells, how do you know the seller will actually deliver the shares, and how does the seller know you will actually pay? In the old days, this trust gap caused defaults. Today it is solved by the clearing corporation.

The clearing corporation steps into the middle of every trade and becomes the buyer to every seller and the seller to every buyer. It guarantees the trade: the buyer always gets the shares, the seller always gets the money, even if one side defaults. This removes counterparty risk, the danger that the person on the other side of your trade vanishes. NSE's clearing arm is NSE Clearing; BSE trades clear through Indian Clearing Corporation. We will explore exactly how this works in the next chapter.

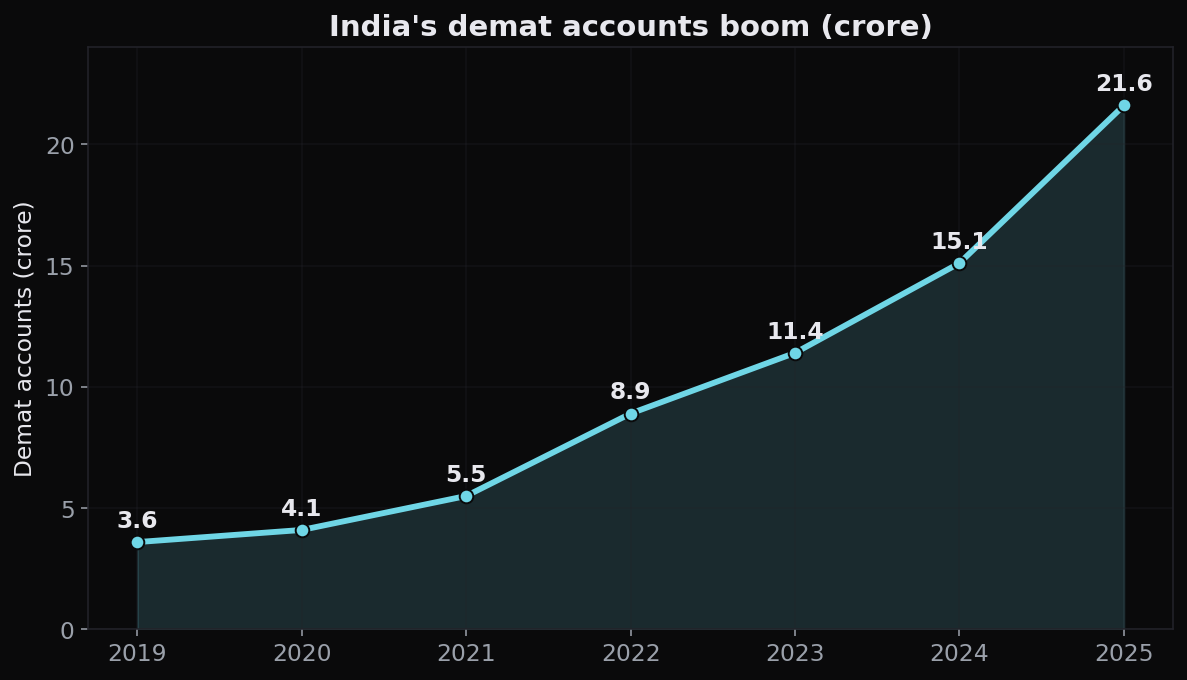

India is opening demat accounts like never before

Put all four together and the result is a system so cheap and trustworthy that Indians are joining it in droves. The number of demat accounts has crossed 21.6 crore, about 216 million (combined NSDL and CDSL, as of December 2025), up from under 4 crore just before the pandemic. That is a more-than-fivefold jump in a few short years.

Of those accounts, CDSL holds the large majority by number, roughly four of every five accounts, around 17 crore, while NSDL holds far fewer, about 4 crore. Yet NSDL holds the far larger share by value of assets, because big institutions and the highest-value holdings tend to sit with it. Two depositories, two very different centres of gravity.

But an account opened is not an investor at work. Of those roughly 21.6 crore accounts, the NSE counts only about 4.9 crore as active, having placed even a single trade in the past year. Strip out the many people who hold several accounts across brokers (often to improve IPO-allotment odds) and the number of distinct investors is closer to 12 crore. A large share of accounts simply sit dormant or duplicated. The account is only a door; actually investing, patiently and regularly, is the real step, and that is the journey we map when you take your first steps as an investor.

A demat account (which holds shares) is usually paired with a trading account (which places orders) and your bank account (which holds the cash). The trio works together: bank funds the buy, trading account places it, demat account stores the shares. We will walk through opening these when you take your first steps as an investor.

Quick recap

- A stock exchange (NSE or BSE) is the marketplace that matches buyers and sellers, BSE is Asia's oldest (1875), NSE is the largest by volume.

- A broker is your licensed gateway to the exchange; discount brokers charge low flat fees, full-service brokers charge more for advice.

- Beyond brokerage, every trade carries small charges and taxes (STT, GST, stamp duty, exchange and DP fees), so no trade is truly free.

- A depository (NSDL or CDSL) is a bank for your shares; your demat account holds them electronically, safe even if your broker disappears.

- The demat revolution replaced risky paper certificates with electronic records, and India now has about 21.6 crore demat accounts (December 2025), though only a fraction are actively traded.

- The clearing corporation guarantees every trade, removing the risk that the other side defaults.

Next, we follow your order past the click of Buy and into the plumbing, how a trade is cleared and settled, and why, thanks to T+1, your shares show up almost the very next day.