Your Own Worst Enemy: Risk & Mindset

Most investors are beaten not by the market but by themselves. Meet position sizing, the biggest behavioural traps, FOMO, anchoring, loss aversion, and how to beat them.

- ·Risk vs reward

- ·Position sizing basics

- ·FOMO & herd behaviour

- ·Loss aversion & anchoring

- ·Why most traders lose

- ·Building good habits

You have spent this whole course learning how the market works, shares and indices, IPOs and settlement, what nudges a price up or down. Here is the uncomfortable truth that ties it all together: understanding the machinery is the easy half. The hard half is managing the anxious, hopeful, easily-spooked human being who has to sit still while their money rises and falls. Decades of data point to the same conclusion, most investors are not beaten by the market. They are beaten by themselves.

This chapter is about that opponent in the mirror. We will look at what risk really is, how to size your bets so no single mistake can wipe you out, and the handful of mental traps that quietly drain returns from clever, well-meaning people. None of it requires a finance degree. It requires honesty about how your own brain works under pressure.

Risk and reward: there is no free lunch

Every investment is a trade between two things: how much it might grow, and how much it might fall along the way. These two are joined at the hip. The chance of a higher return always comes bundled with a higher chance of a bumpy ride or a loss. Anything that seems to offer big rewards with no risk is either misunderstood or a lie, usually the second.

- A bank fixed deposit barely moves. Low risk, low reward.

- A large, established company's shares wobble. Medium risk, medium reward.

- A tiny unknown small-cap can double or halve in a month. High risk, high reward.

This is not a flaw in the system to be outsmarted; it is the system. The skill is not finding risk-free riches, they do not exist. The skill is deciding how much risk suits your goals, your timeline, and how well you sleep at night.

"Risk" is not the same as "loss." Risk is uncertainty, the range of things that could happen. A stock that swings wildly but you hold for twenty years may be far less risky to your actual goal than cash that quietly loses to inflation. Match the risk to the time you have, not to your mood today.

Don't bet the farm: position sizing and diversification

Here is the single most expensive beginner mistake: putting a huge chunk of your money into one "sure thing." It feels like conviction. It is actually a coin-flip with your future. The fix has an old name, don't put all your eggs in one basket, and a slightly more grown-up one: position sizing and diversification.

Position sizing means deciding, in advance, how much of your total money any single stock is allowed to be. If one company can sink 50% on a bad result, and good companies sometimes do, then keeping it to, say, 5% of your portfolio means your whole wealth only dips about 2.5%. Annoying, survivable. Put 80% in that same stock and the same bad day becomes a catastrophe you may never recover from.

Diversification is the same idea spread wider: own many stocks, across different industries, so that no single company, sector, or piece of bad news can sink you. When you own a broad index fund, you get this almost for free, the Nifty 50 spreads your money across fifty large companies in a dozen industries at once.

A simple beginner rule of thumb: no single stock as a very large share of your portfolio, and never invest money you will need within the next three to five years. Markets can stay down for a couple of years, and you do not want to be a forced seller at the bottom because rent is due.

The enemy in the mirror

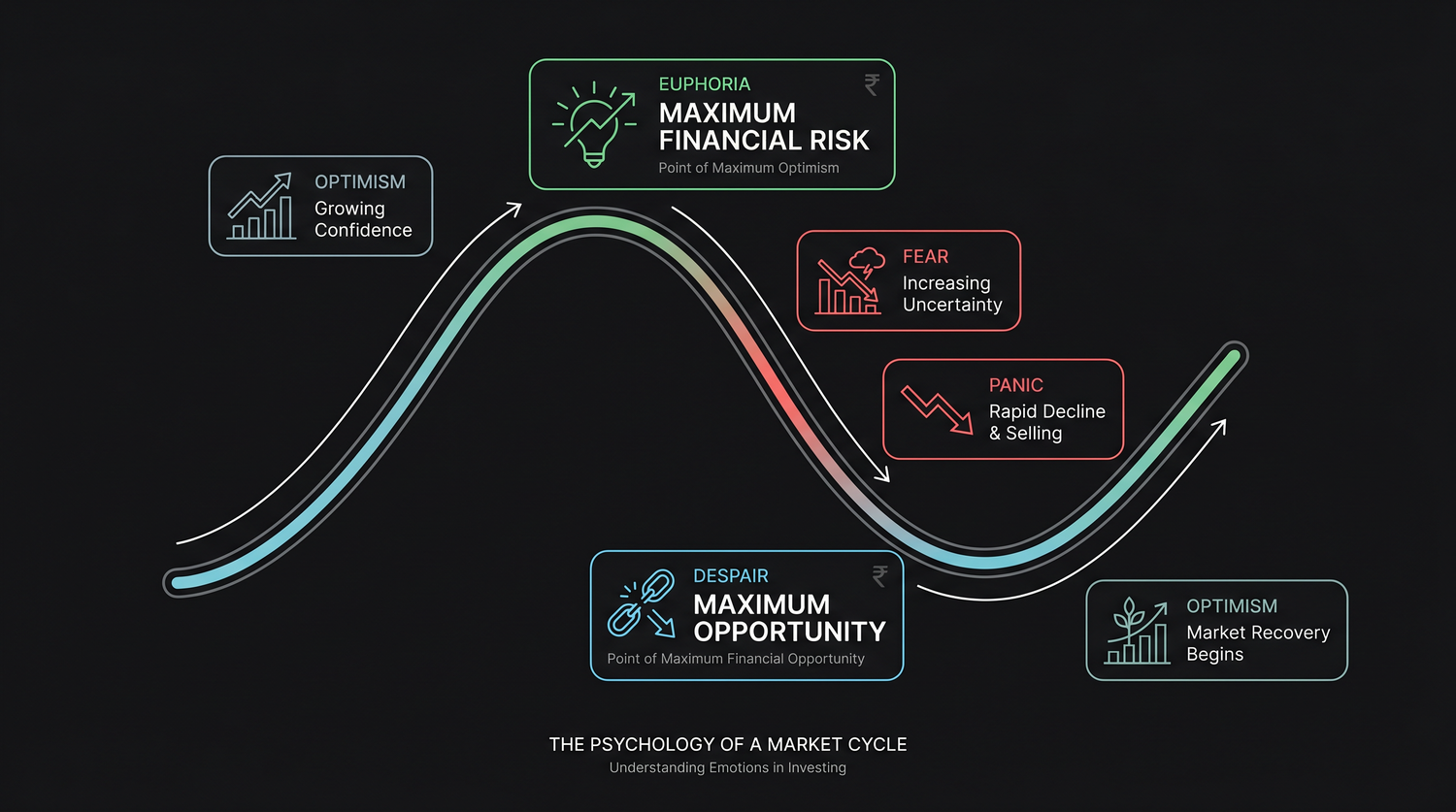

Now the real subject of this chapter. Your brain was built to keep an ancestor alive on a savannah, to run with the herd, to fear loss, to act fast on a fright. Those instincts are catastrophic for investing, where the winning move is usually to do nothing while everyone around you panics or celebrates. Markets even have a famous emotional shape, repeated in every boom and bust.

Look at that curve. The point where everyone feels most confident, euphoria, near the peak, is the moment of greatest danger. The point where everyone feels sick and hopeless, despair, near the bottom, is where the best long-term bargains sit. Our feelings are an almost perfect reverse signal. Understanding that is half the battle. The named traps below are the specific ways the feeling gets you.

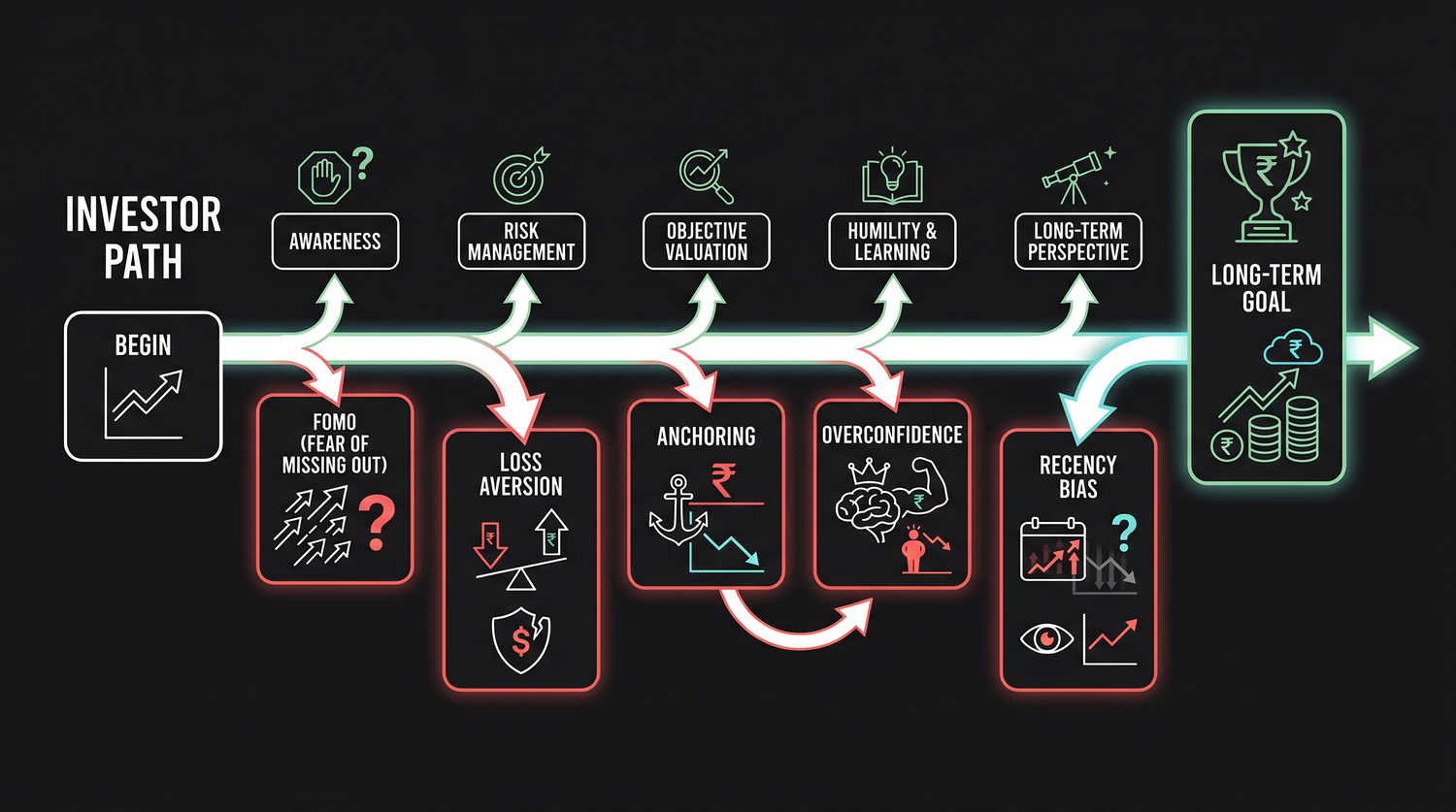

FOMO and the herd

When a stock has already shot up 200% and your neighbour, your barber, and three Telegram groups are all talking about it, the pull to jump in is enormous. That is the fear of missing out, and it is herd behaviour at work, we feel safe doing what the crowd is doing. The cruel joke is that by the time something is obviously working and everyone is in, most of the gain has already happened, and you are buying from the smart money that is quietly selling to you.

Loss aversion: watering weeds, cutting flowers

Psychologists have shown that the pain of losing money is roughly twice as intense as the pleasure of gaining the same amount. This single quirk causes one of the commonest mistakes: investors hold their losers far too long ("I'll sell when it gets back to what I paid") and sell their winners far too early ("let me lock in this small profit before it vanishes"). The result is a portfolio where you keep watering the weeds and cutting the flowers, exactly backwards.

Anchoring: the price you paid doesn't care about you

You bought a stock at Rs 500. It is now Rs 380. You refuse to sell because you are anchored to that 500, it has become a magic number in your head. But the stock has no idea what you paid. Its future depends only on the business from here, not on your purchase price. Tying decisions to your entry price, rather than to what the company is actually worth now, is one of the quietest, costliest biases there is.

Overconfidence and recency bias

After a few good calls, almost everyone starts to feel like a genius. That is overconfidence, and it leads to bigger bets, more trading, and less caution, right before reality humbles you. Its cousin is recency bias: assuming whatever just happened will keep happening. When markets have risen for three years, people feel they always will; after a crash, they swear stocks are a scam. Both are the brain mistaking the recent past for the permanent future.

Studies that track real investor behaviour, such as Morningstar's long-running "Mind the Gap" research, repeatedly find that the average fund investor earns noticeably less per year than the very funds they own, often by around one to one-and-a-half percentage points, purely from buying and selling at the wrong moments. The fund did fine. The investors, trading on emotion, sabotaged themselves. (Figures are approximate and vary by period.)

Why most people who "trade" lose

This connects to the core message of the whole course: you cannot reliably time the market, and trying to is exactly how most people lose. The instinct is to sell when things look scary and buy when things look exciting, which, as that emotion curve shows, means selling near bottoms and buying near tops. Do that a few times and you have engineered the worst possible outcome.

The data on active, frequent traders is brutal and consistent across countries: the large majority lose money over time, especially in fast products like intraday and derivatives, once you count costs and taxes. Meanwhile the "boring" investor who simply kept buying a low-cost index fund every month, through crashes, through booms, ignoring the noise, usually ends up ahead of the clever crowd. Not because they were smarter. Because they got out of their own way.

Be especially wary of yourself right after a big win or a big loss. After a win you will feel invincible and take a reckless bet; after a loss you will feel desperate and try to "win it back" fast. Both states are when people blow up accounts. The strongest move in those moments is to close the app and do nothing for a day.

Habits that beat your own brain

You cannot delete these instincts, they are factory-installed. But you can build systems that stop them from making your decisions for you.

- Automate it. Set up an automatic monthly investment (an SIP). When the buying happens on autopilot, FOMO and fear never get a vote.

- Write your plan down, what you own, why, and what would actually make you sell. When emotion strikes, re-read it instead of reacting.

- Check your portfolio less. Daily watching turns normal wobbles into stress and tempts you to tinker. Monthly or quarterly is plenty.

- Decide rules in advance, in calm moments, your position-size limit, how much cash you keep, how you'll behave in a crash. Calm-you should govern panicked-you.

- Expect crashes. Markets fall 30-50% every so often, it is normal, not the end. Investors who expect it stay calm; those shocked by it sell at the worst time.

Two friends invest through a sharp 35% market crash. Anjali, watching the news in horror, sells everything near the bottom to "stop the bleeding," then waits, too nervous to buy back, and misses most of the recovery. Vikram does nothing; his automatic SIP even keeps buying cheaper units all the way down. Two years later the index has fully recovered and gone higher. Same market, same crash. Anjali locked in a permanent loss; Vikram came out ahead. The only difference was behaviour.

Quick recap

- Higher reward always rides with higher risk, anything promising big returns with no risk is a misunderstanding or a lie.

- Size your positions and diversify so no single stock or sector can wipe you out; a broad index fund diversifies almost for free.

- Markets move in an emotional cycle, peak euphoria is maximum risk, deepest despair is maximum opportunity; your feelings are a reverse signal.

- The big traps, FOMO and herd, loss aversion, anchoring, overconfidence, recency bias, quietly turn smart people into poor investors.

- You cannot time the market; panic-selling and greed-buying are how most people lose, while the steady, boring, automated investor usually wins.

- Build systems, automate, write the plan, check less, decide rules when calm, to keep your own brain from making the decisions.

There is one more way to lose money that has nothing to do with your psychology and everything to do with someone else's greed, the outright scam. In the final chapter we meet India's most infamous frauds, the red flags they all share, and exactly how to make sure you are never the victim.