What Happens After You Hit Buy

What actually happens after you click Buy, the behind-the-scenes journey of money and shares, India's move to T+1 (and T+0), and why it almost never fails.

- ·What clearing means

- ·Settlement explained

- ·India's T+1 cycle

- ·The role of the clearing corp

- ·Rolling settlement

- ·Why defaults are rare

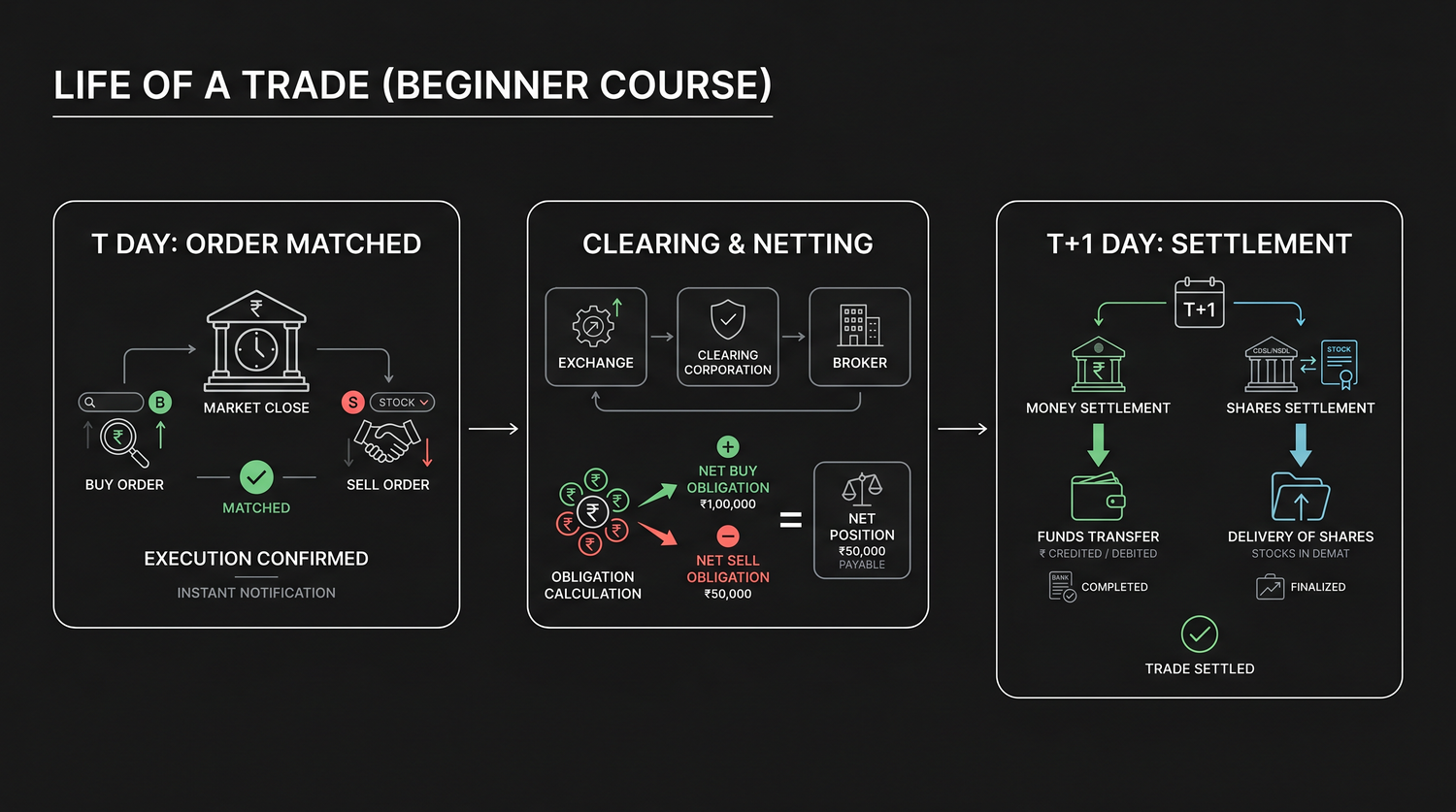

You bought 10 shares of Reliance at 10:15 this morning. By the time you locked your phone, the order said "executed" and the shares appeared in your portfolio. Done and dusted, right? Not quite. At that moment, no shares and no money have actually changed hands. What you witnessed was a promise, a binding agreement that you will pay and the seller will deliver. The real swap of money for shares happens later, behind the scenes, through a process called settlement.

This is the unglamorous plumbing of the market, and it is worth understanding for one reason: it is the part that makes everything else trustworthy. When this machinery works, and in India it almost always does, you can buy from a complete stranger on the other side of the country and be certain you will get your shares, and they will get their money. Let us open the hood.

A trade is a promise; settlement is the delivery

The single most useful idea in this chapter is that a trade and its settlement are two separate moments in time.

- The trade is the agreement: at 10:15, a buyer and a seller agreed on a price for 10 shares. The exchange matched them. A deal exists, but only on paper.

- The settlement is the fulfilment: the buyer's money actually moves to the seller, and the seller's shares actually move to the buyer. This happens hours or a day later.

Between those two moments, two things have to be figured out and then carried out. Working out who owes what is called clearing. Actually moving the money and shares is called settlement.

Clearing: working out who owes what

On any given day, you might buy 10 shares of Reliance, sell 5, and buy 8 more. Multiply that by crores of trades across millions of investors, and the exchange has a tangled web of obligations. Clearing is the process of untangling it, calculating, for every participant, the net amount of money and shares they owe or are owed at day's end.

The key trick here is netting. Instead of settling every single trade individually, the clearing corporation adds up all your buys and sells in a stock and works out your net position. If you bought 10 and sold 5 of the same share, you only need to receive 5 net shares, not shuffle 15 separately. Netting collapses a mountain of individual trades into one tidy figure per investor per security. It is the difference between settling crores of trades and settling a handful of net obligations, a massive efficiency.

Clearing answers "who owes what?" Settlement answers "now let's actually pay and deliver." Clearing is the accounting; settlement is the action. The clearing corporation does the first and orchestrates the second.

Settlement: the actual swap

Once clearing has produced everyone's net obligations, settlement executes them. On settlement day, the system does two things simultaneously:

- Pay-in, buyers' money and sellers' shares are collected. Money is debited from buyers' bank accounts; shares are debited from sellers' demat accounts.

- Pay-out, the shares are credited into buyers' demat accounts, and the money is credited into sellers' bank accounts.

This simultaneous swap is the whole point. The buyer parts with cash as they receive shares; the seller parts with shares as they receive cash. Neither side has to trust the other directly, because the clearing corporation handles both legs at once.

Rolling settlement and the road to T+1

How long does this take? In a rolling settlement system, trades settle a fixed number of business days after the trade date. The trade day is called T, and the settlement happens a set number of days later.

India has steadily compressed this gap over the years, and it is a genuine point of pride:

| Era | Cycle | What it meant |

|---|---|---|

| Until 2001 | Weekly "badla" settlement | Trades piled up and settled once a week |

| 2002 | T+3 | Settle three working days after the trade |

| 2003 | T+2 | Two days, the global standard for two decades |

| Jan 2023 | T+1 | Settle the very next working day |

| 2024-25 | Optional T+0 | Same-day settlement, being phased in |

In January 2023, India completed its move to T+1, meaning a trade done today settles tomorrow. Crucially, India was among the very first major markets in the world to fully adopt T+1. The United States, for context, only moved to T+1 in May 2024, more than a year after India. For once, India's market plumbing was ahead of Wall Street's.

When India switched fully to T+1 in January 2023, it leapfrogged the developed world. The US, UK and Europe were still on the slower T+2 cycle at the time. A market often seen as "emerging" was, on settlement speed, leading the planet.

What T+1 actually feels like

For you as an investor, T+1 means real convenience. Sell your shares today, and the money is usable in your account the next working day. Buy today, and the shares are firmly yours, deliverable, the next day. Faster settlement also means less time for things to go wrong in between, which makes the whole system safer, not just quicker.

T+0: the same-day experiment

India did not stop at T+1. In March 2024, SEBI launched a beta of optional T+0 settlement, same-day settlement, where money and shares change hands on the very day you trade. From early 2025, it began a phased rollout across the top 500 stocks by market value, adding roughly 100 stocks at a time.

A few things to keep straight:

- T+0 is optional, running alongside T+1, not replacing it. You and your broker choose.

- It applies to a defined list of large stocks, expanding gradually.

- The aim is same-day liquidity, sell in the morning, have the cash the same afternoon.

It is an experiment that, if it succeeds, could make India one of the first markets anywhere with mainstream same-day settlement.

Do not confuse a fast settlement cycle with intraday trading. T+1 and T+0 are about how quickly a completed trade finalises. You can already buy and sell the same stock within a single day (intraday) regardless, that is a different feature. Settlement is about when the dust finally settles on ownership and cash.

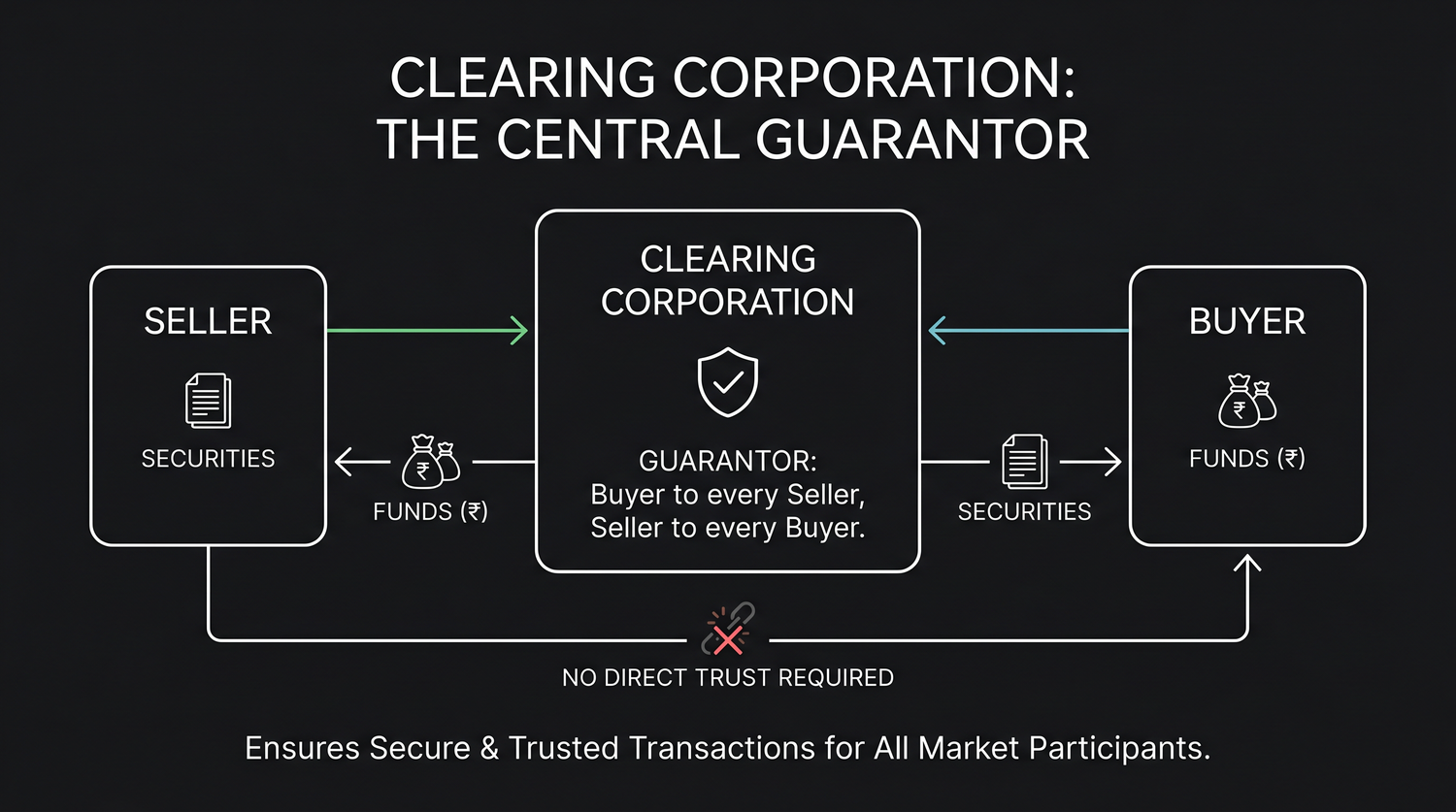

The clearing corporation: the guarantor in the middle

Now the most important safety idea of all. When you buy, how can you be sure the anonymous seller will deliver? You cannot, and you do not have to. The clearing corporation steps into the centre of every trade and legally becomes the buyer to every seller and the seller to every buyer. This is called novation.

Because of this, you are never actually relying on the stranger on the other side. You are relying on the clearing corporation, and it guarantees the trade. The buyer is guaranteed their shares; the seller is guaranteed their money. The danger that the other party vanishes, counterparty risk, is removed entirely.

Why settlement failures are vanishingly rare

If the clearing corporation guarantees everything, what happens when someone genuinely fails to pay or deliver? It is protected by layers of armour built up before trades are even allowed:

- Margins, traders must deposit money upfront as a security cushion, so they have skin in the game.

- The Settlement Guarantee Fund (SGF), a large pool of money kept aside specifically to complete a settlement if a member defaults.

- Auctions and penalties, if a seller fails to deliver shares, the system buys them in the open market to make the buyer whole, and penalises the defaulter.

Stacked together, these make a true settlement failure extraordinarily rare in India. The guarantee almost never has to be tested, which is exactly why investors can trade with total strangers without a second thought.

The reason you can buy shares from someone you will never meet, in a faraway city, with complete confidence, is the clearing corporation's guarantee. It quietly absorbs the risk that the other side defaults, turning a leap of faith into a routine, boring, safe transaction.

Quick recap

- A trade is a promise made when buyer and seller are matched; settlement is when money and shares actually change hands, two separate moments.

- Clearing works out who owes what (using netting to collapse many trades into tidy net figures); settlement carries out the actual pay-in and pay-out.

- India uses rolling settlement and completed its move to T+1 in January 2023, among the first major markets in the world, ahead of the US.

- SEBI introduced an optional T+0 (same-day) settlement from 2024-25, being phased across the top 500 stocks.

- The clearing corporation becomes buyer to every seller and seller to every buyer, removing counterparty risk and guaranteeing the trade.

- Thanks to margins, the Settlement Guarantee Fund and auctions, settlement failures are extremely rare.

Next, we rewind all the way to the beginning of a company's life, how a tiny startup raises money round by round, growing from an idea into a business big enough to one day sell its shares to you.