What Makes a Stock Move

Price is just the latest agreement between a buyer and a seller. See how supply, demand, news and expectations move a stock minute by minute.

- ·Supply & demand

- ·Why price changes tick by tick

- ·News & expectations

- ·Earnings reactions

- ·The role of sentiment

- ·Return calculation

Here is a question that sounds simple but unlocks almost everything about the market: why does a stock's price change at all? One minute Reliance is at Rs 1,420, a few seconds later it is Rs 1,420.50, then Rs 1,419.80. Who decides those numbers? Not the company. Not the exchange. Not some committee setting a "fair price." The truth is humbler and far more powerful: a stock's price is simply the most recent amount a willing buyer and a willing seller agreed on. Nothing more.

Every tick you see on the screen is a fresh handshake. The price is not a fact handed down from above, it is a negotiation, happening thousands of times a second, between people who disagree about what the share is worth. Understand that, and the rest of this chapter falls into place.

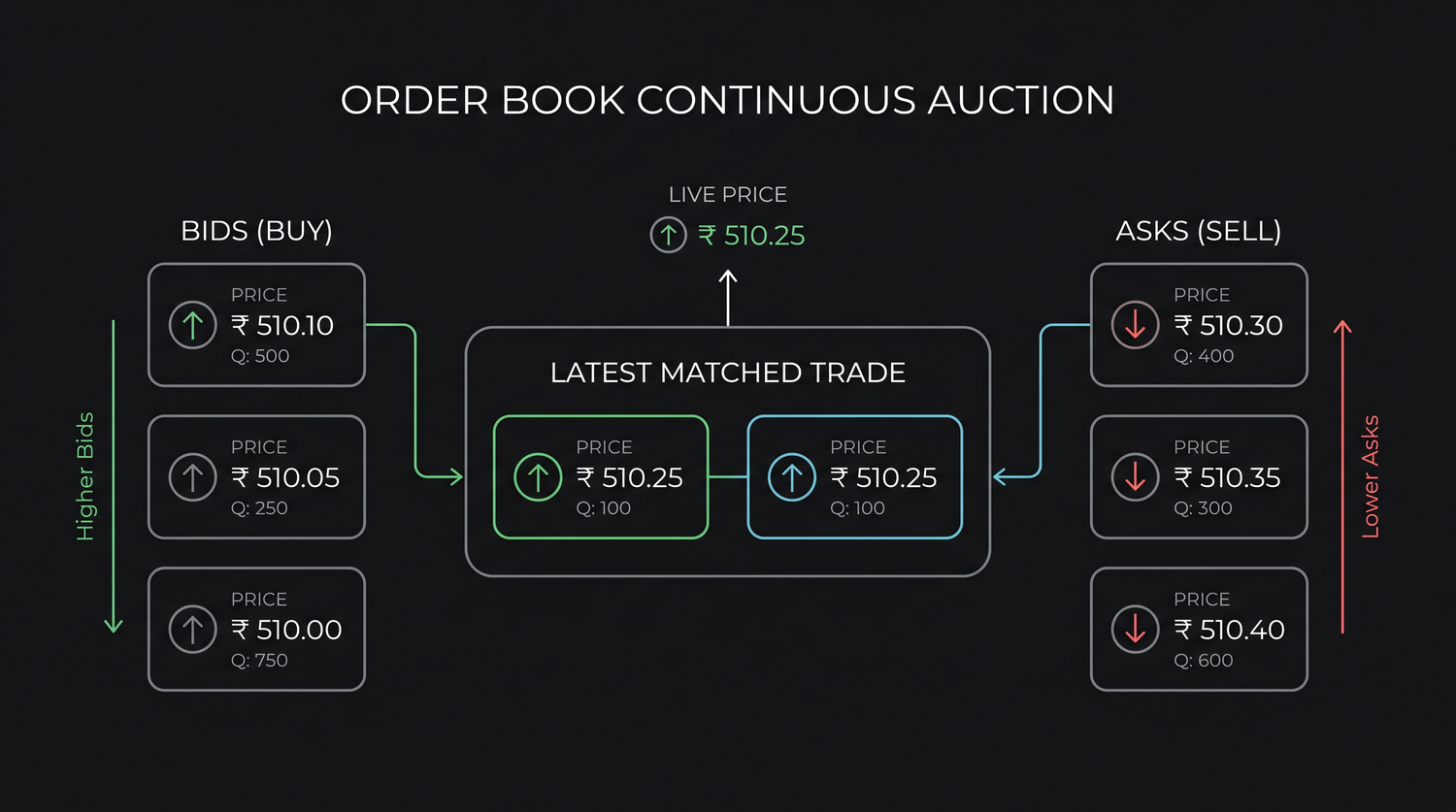

The order book: a continuous auction

Behind every stock sits an order book, a live list of everyone who wants to buy and everyone who wants to sell, and at what price. On one side are the buyers with their bids (the prices they are willing to pay). On the other are the sellers with their asks (the prices they want to receive).

A trade happens only when a buyer and a seller agree on a price, when someone is willing to pay what someone else is willing to accept. The price of that matched trade becomes the new "last traded price," the number you see quoted. Then the next match sets the next price, and so on, all day. It is a continuous auction, not a once-a-day gavel, but a rolling negotiation that never pauses during market hours.

This is why price moves tick by tick, and the logic is beautifully simple:

- When buyers are more eager than sellers, more demand than supply, buyers start accepting higher asks to get their shares. The price ticks up.

- When sellers are more eager than buyers, more supply than demand, sellers start accepting lower bids to offload. The price ticks down.

That is the entire engine. Up or down, every move traces back to one imbalance: at this instant, was there more hunger to buy or more hunger to sell?

A stock price is not what a company is "worth." It is the live score of an ongoing tug-of-war between buyers and sellers. More eager buyers than sellers pushes it up; more eager sellers than buyers pulls it down. Everything else in this chapter is really about what makes the crowd lean one way or the other.

What tips the balance

If price is a tug-of-war, the interesting question becomes: what makes a wave of people suddenly want to buy, or rush to sell? A few big forces:

- News. A new government contract, a factory fire, a regulatory ban, a CEO resignation, fresh information instantly changes how people value a company, and they reposition.

- Earnings. Every quarter, companies report their profits. Strong results pull buyers in; weak ones send sellers running. (More on the twist below.)

- Expectations. This is the subtle, market-defining one. Prices reflect not just today but what people expect tomorrow.

- Sentiment. Sometimes the whole market is simply fearful or greedy, and that mood sweeps individual stocks along regardless of their own news.

Markets price the future, not the present

Here is the single most counter-intuitive truth for beginners, and getting it early will save you years of confusion: the market is a forward-looking machine. Today's price already bakes in what investors expect to happen. So a stock does not react to whether the news is good or bad in absolute terms, it reacts to whether the news is better or worse than what was already expected.

This is why you will see a company report record profits, genuinely excellent numbers, and watch the stock fall the same afternoon. How? Because investors had expected even better. The great result still missed the even-higher expectations already priced in, so the buyers who had bid the stock up in anticipation now sell in disappointment.

The flip side is just as real: a struggling company can report an ugly loss and the stock rises, simply because the loss was smaller than feared. The market is always comparing reality against expectation, not against zero.

Traders have a saying for this: "buy the rumour, sell the news." A stock often climbs for weeks in anticipation of a great result, as expectation builds, and then falls the moment the actual good news arrives, because the people who bought the rumour now take their profits. The news everyone waited for becomes the trigger to sell. Good news, falling price, and now you know why.

Sentiment and the herd

Markets are made of people, and people are emotional and social. When prices are rising, optimism feeds on itself, others are making money, so more pile in, pushing prices higher still. This is herd behaviour, and it works in reverse too: when prices fall, fear spreads, people sell to avoid further pain, and the selling itself drives prices lower.

Sentiment can detach a stock from its fundamentals for surprisingly long stretches, sending it higher than any sober valuation justifies in a bubble, or lower than it deserves in a panic. Recognising that the crowd is part of the price is one of the most useful mental models you can carry. We devote a whole later chapter to mastering your own psychology so the herd does not carry you along.

"Everyone is buying it" is not a reason to buy. By the time a stock is the talk of every WhatsApp group, much of the optimism is already in the price, and you may be buying exactly when the early crowd is preparing to sell. The herd is loudest right before it turns.

A concrete example: results day

Picture a fictional IT company, InfoCore, trading at Rs 500. Analysts expect quarterly profit growth of 15%, and over the past month the stock has quietly climbed from Rs 450 to Rs 500 as investors positioned for a strong number. Results come out: profit grew 12%, genuinely healthy growth, but below the 15% the market had priced in. Within minutes, disappointed buyers turn sellers, the order book tilts to the sell side, and InfoCore drops to Rs 465.

A neighbour who only reads the headline is baffled: "Profits grew and the stock fell?" But you understand now, the market was comparing 12% against an expected 15%, not against zero. The growth was real; it simply was not enough. Had InfoCore delivered 18%, the same report would have sent it soaring.

Putting a number on it: calculating your return

Whichever way a stock moves, you will want to measure how you did. Two numbers matter.

Absolute return is the plain rupee gain or loss:

Absolute return = Selling price, Buying price

Buy at Rs 400, sell at Rs 500, and your absolute gain is Rs 100 per share.

Percentage return scales that to your investment, so you can compare it fairly against anything else:

Percentage return = (Gain / Buying price) x 100

Here: (100 / 400) x 100 = 25%. A 25% return.

Percentage matters more than rupees. A Rs 100 gain on a Rs 400 stock is a 25% return. The same Rs 100 gain on a Rs 2,000 stock is only 5%. Same rupees, very different result, always think in percentages so you are comparing like with like.

There is one more layer: time. A 25% return is spectacular in one year and mediocre over ten. To compare investments held for different lengths, people convert returns to a per-year figure, the annualised return. The exact maths comes later; for now, just lock in the instinct to always ask two questions about any return: how much, and over how long? A number without a timeframe is only half a fact.

When someone boasts that a stock "doubled," your first question should be "over what period?" Doubling in one year is extraordinary; doubling over fifteen years works out to under 5% a year, slower than a fixed deposit. Return and time are inseparable. Never let anyone quote you one without the other.

Quick recap

- A stock's price is just the latest agreement between a willing buyer and a willing seller, a fresh handshake, thousands of times a second, not a value handed down from above.

- The order book runs a continuous auction: more eager buyers than sellers ticks the price up, more eager sellers than buyers ticks it down.

- News, earnings, expectations and sentiment are what tip that balance and send the crowd leaning one way.

- Markets price the future, so a stock reacts to results relative to expectations, a great quarter that misses even-higher hopes can still fall ("buy the rumour, sell the news").

- Herd behaviour can push prices far above or below fair value, which is why "everyone is buying" is a warning, not a reason.

- Measure your outcome with absolute (rupee) and percentage return, and always pair any return with the timeframe it took.

Next, we widen the lens from a single stock to the whole economy, how interest rates, inflation, the rupee, crude oil and global flows tug at Indian shares from above.