Your First Steps as an Investor

Your practical first steps, opening a demat account, the two paths of buying stocks directly versus mutual funds and index-fund SIPs, and how to form your own point of view before you ever buy.

- ·Demat & KYC, in plain words

- ·Direct stocks vs mutual funds

- ·Index funds & the SIP habit

- ·Forming a point of view

- ·A sensible beginner roadmap

- ·Starting small and safe

You have spent the last fifteen chapters learning how the market works, what a share is, who runs the exchanges, what moves prices, how the macro weather blows. Now comes the chapter that actually changes your life: turning all that understanding into a few simple actions. Most people stay "someday investors" forever, trapped in the gap between knowing and doing. The aim here is to close that gap, calmly, cheaply, and safely, so that by the end you know exactly what the first steps look like.

A gentle reminder before we start: this is education, not advice. It will not name a single broker or fund, because the right one depends on you. What it will give you is a clear, non-scary map from saver to investor.

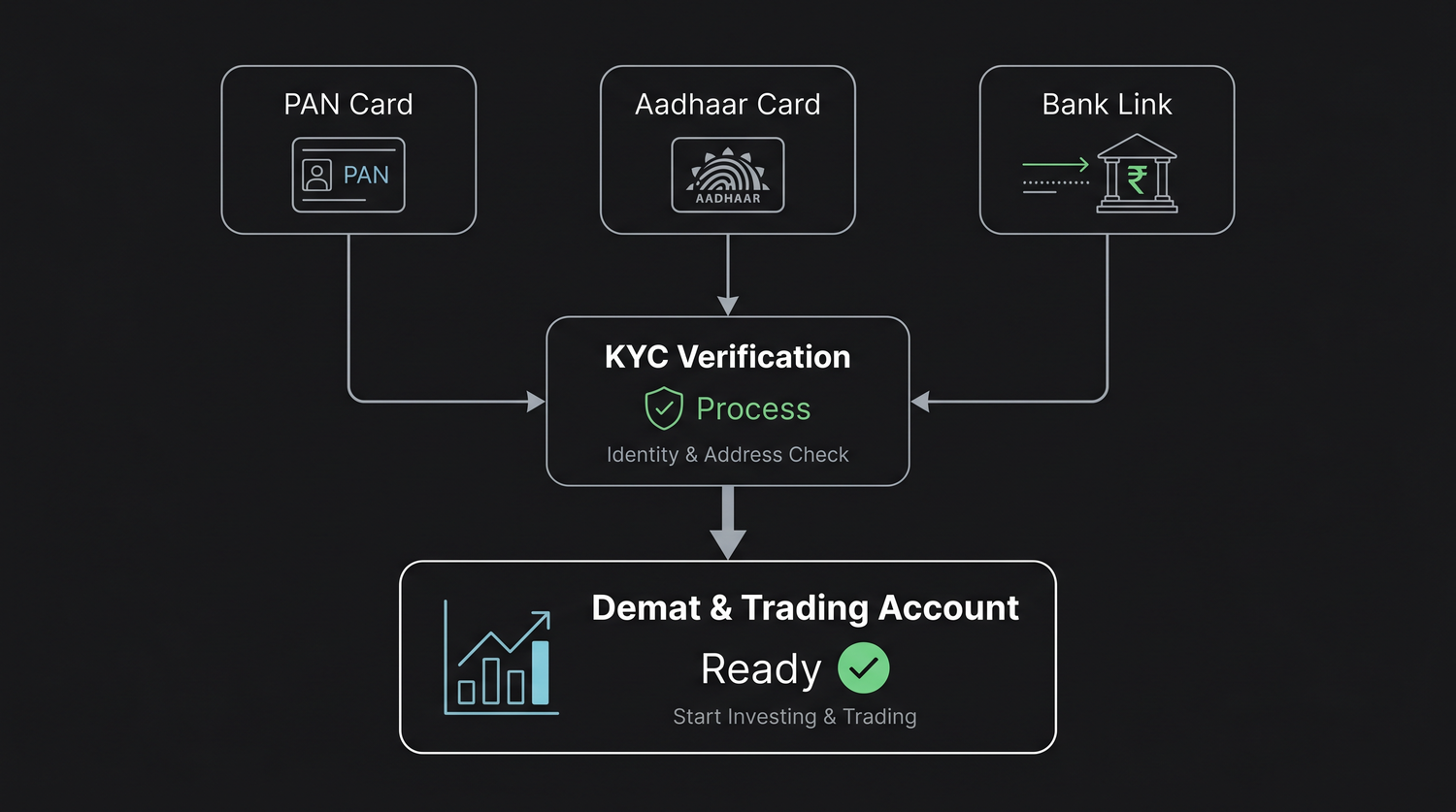

Step one: the demat and trading account

To buy and hold shares, you need two linked accounts, and these days they are usually opened together, fully online, in a day or two:

- A demat account holds your shares in electronic form, the way a bank account holds your money. (Recall the depositories, NSDL and CDSL, from the market-ecosystem chapter, your demat account sits with one of them.)

- A trading account is what lets you place buy and sell orders on the exchange.

KYC, in plain words

Before either account opens, you must complete KYC, "Know Your Customer." It is simply the legal check that you are who you say you are, and it is the same safeguard that makes fraud harder across the whole financial system. You will typically need:

- PAN card, your tax ID, the backbone of any Indian financial account.

- Aadhaar, used for identity and address, often for instant e-verification by OTP.

- A bank account, linked so money can move in and out (a cancelled cheque or your bank details).

- A photo and signature, and sometimes a brief video verification.

The whole process is online now, upload, verify with an OTP, e-sign, done. No queues, no thick files of photocopies like in the old days.

India has crossed roughly 21.6 crore demat accounts, about 216 million (as of December 2025), many times the number just a few years earlier. A whole generation is opening accounts from their phones in minutes, a task that once took weeks of paperwork.

:::key Opening the account is the easy part, and the smallest. Of those ~21.6 crore demat accounts, fewer than 5 crore are active in any given year; many of the rest were opened and left idle, or are duplicates one person holds across brokers. The account is just a door. Being ready to invest, an emergency fund in place, costly debt cleared, a simple plan and a steady SIP, is the real milestone. If you opened an account and never invested, you are not behind; you are exactly where most people are. The rest of this chapter is about walking through that door properly.

:::

Two paths from here

With your account open, a beginner reaches a fork in the road. Both paths are valid; they suit different people and often work best together.

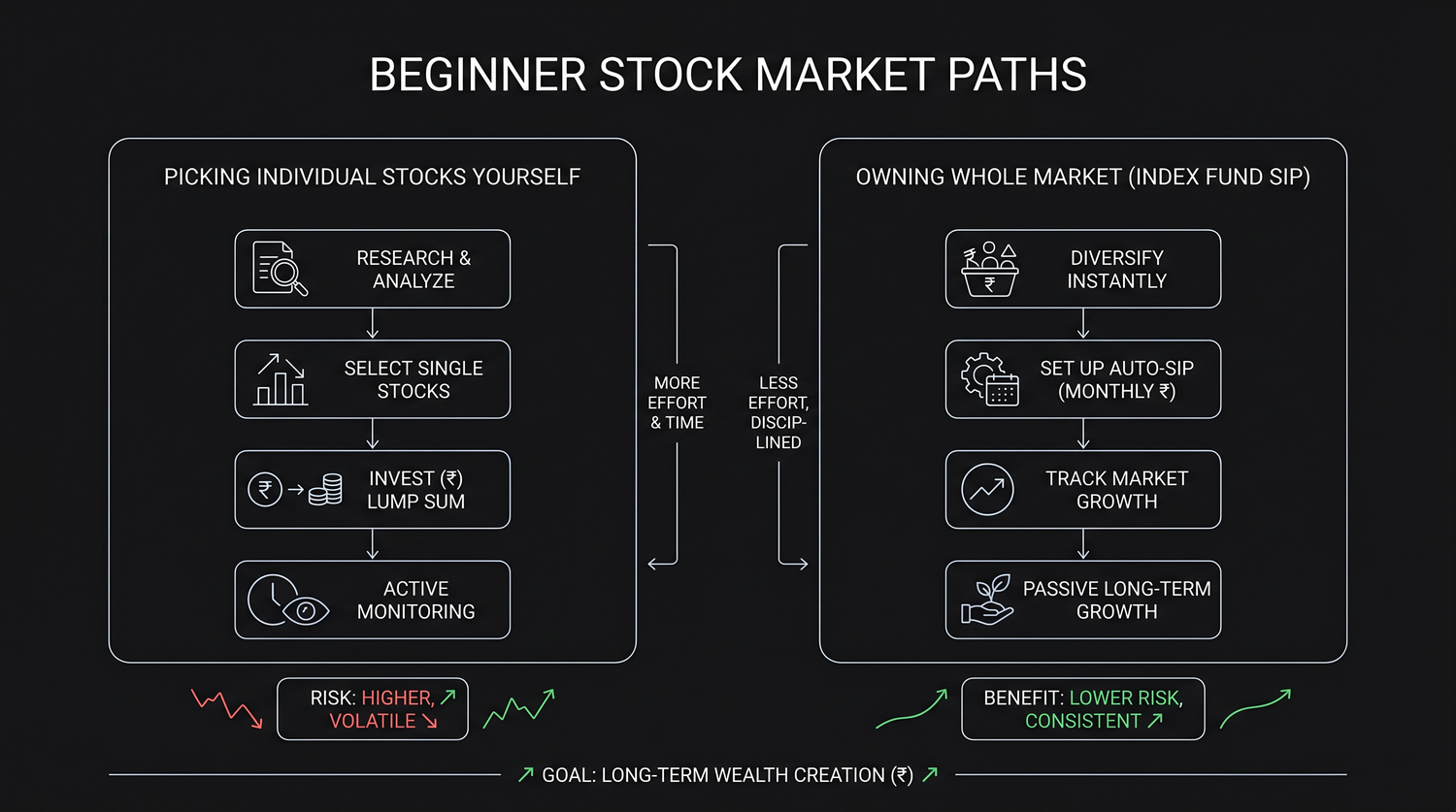

Path 1: buy individual stocks directly

You research and pick specific companies, then buy their shares yourself.

- Upsides: full control, you own exactly what you choose, and the potential for higher returns if you choose well. You also learn the fastest this way.

- Downsides: it demands real research on every company, carries more risk (one bad pick can hurt), needs time and a steady temperament, and makes emotional mistakes easy.

This path suits you best after you have learned the basics and want an active role, usually starting with only a small slice of your money.

Path 2: mutual funds and index funds, via SIP

Instead of picking stocks yourself, you buy a fund that holds many stocks for you.

A mutual fund pools money from thousands of investors, and a professional invests it across many companies, giving you instant diversification in a single purchase.

An index fund is a special, low-cost type of mutual fund that simply mirrors an index like the Nifty 50. It buys all 50 stocks in the same proportions as the index, so one purchase makes you a part-owner of India's 50 largest companies at once. There is no manager trying to beat the market, it just quietly tracks it, at a very low fee.

Upsides: instant diversification, hands-off, low cost, and no need to analyse individual companies, which is exactly why it suits most beginners.

Downsides: you will match the index, not beat it, and it feels far less exciting than picking a winner.

The SIP habit

The single most beginner-friendly habit in all of investing is the SIP, Systematic Investment Plan. You invest a fixed sum, say Rs 1,000 or Rs 5,000, automatically every month into a fund. Three quiet superpowers come with it:

- Discipline on autopilot, you invest every month regardless of your mood or the day's scary headline.

- Rupee-cost averaging, the same fixed amount buys more units when prices are low and fewer when high, smoothing out your average purchase price over time.

- You can start tiny, many SIPs begin at just Rs 500 a month, so there is no excuse to wait.

This is not a fringe idea. By late 2025, Indians were pouring a record Rs 31,000 crore a month (approximate) into mutual funds through SIPs, across nearly 10 crore SIP accounts, the steady domestic tide we met in the macro chapter.

| Direct stocks | Index-fund SIP | |

|---|---|---|

| What you own | Specific companies you pick | A slice of the whole index |

| Diversification | You must build it yourself | Instant, in one purchase |

| Effort | High, research each stock | Low, automated monthly |

| Risk | Concentrated, higher | Spread across many stocks |

| Best for | An active role, once you've learned | Almost every beginner, hands-off |

For most beginners, the wisest start is a small, automated index-fund SIP, instant diversification, almost no effort, very low cost, and then adding a few direct stocks slowly, as your knowledge and confidence grow. The two paths are partners, not rivals.

Form your own point of view first

Before you buy any individual stock, you should be able to explain, in your own plain words, three things:

- What the business actually does, and how it makes money.

- Why you believe it will be larger or more profitable in five to ten years.

- What could go wrong with that story.

If you cannot explain the "why" yourself, you are not investing, you are gambling on a tip. Everything in the earlier chapters (what moves a stock, the macro forces, how earnings work) existed to help you form your own view, rather than borrowing one from a stranger.

Never buy a stock simply because someone told you to, a WhatsApp group, a flashy social-media "tip," a confident voice on TV. Borrowed conviction collapses the instant the price dips, and that is when beginners panic-sell at a loss. We will dig into these traps and outright scams in a later chapter. (Index funds are the honourable exception: you do not need a view on any single company, which is part of why they suit beginners so well.)

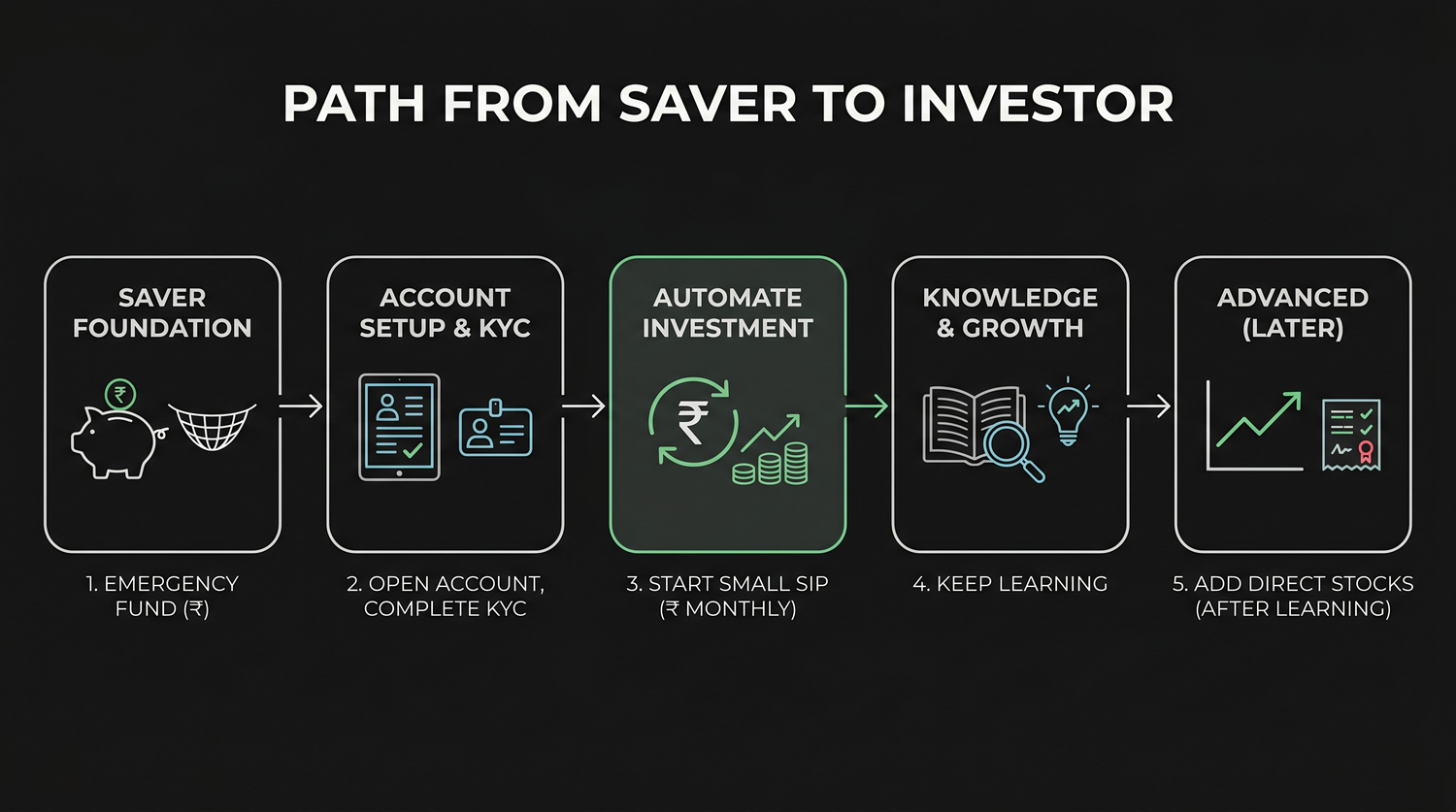

A sensible beginner roadmap

Here is a calm order of operations, the boring sequence that quietly works:

- Build an emergency fund first, three to six months of expenses in a safe, liquid place, so you never have to sell investments during a crisis.

- Clear costly debt, credit-card balances and expensive personal loans cost far more than markets are likely to return.

- Open your demat and trading account and finish KYC.

- Start a small, automated SIP into a broad index fund, even Rs 500 to Rs 1,000 a month. Build the habit before chasing the returns.

- Keep learning, read the results of companies you find interesting, follow the macro mood, understand what you own.

- Add direct stocks slowly, only with money you can afford to lose, only once you can form your own view, and only with a small slice at first.

- Stay consistent and patient, then let compounding, the lesson from the very first chapter, do the heavy lifting over the years.

Your first goal is not returns, it is building the habit and learning your own temperament with very little at stake. A steady Rs 1,000 SIP that you never stop will, over decades, almost always beat a clever Rs 50,000 bet you made once and panicked out of.

Start small, start safe

You do not need a fat bank balance or perfect knowledge to begin, just an amount that will not hurt if it falls, and the willingness to start. The early years are tuition: you are learning how you react when prices wobble, worth far more than any single year's gains. Begin small, automate the boring part, keep reading, and let time compound both your money and your understanding.

Nothing here is a recommendation to buy any particular stock, fund or product, and no one can promise you returns. It is a map of how the journey usually begins. The specific choices, which provider, which fund, how much, are yours to make once you understand the trade-offs.

Quick recap

- To invest you need a demat account (holds shares) and a trading account (places orders), opened online after a simple KYC with PAN, Aadhaar and a bank link.

- Beginners face two paths: direct stocks (more control, more research, more risk) or mutual / index funds (instant diversification, hands-off).

- An index fund mirrors an index like the Nifty 50 cheaply; a SIP automates a fixed monthly investment, building discipline and averaging your cost.

- Before buying any single stock, form your own point of view, understand the business and the "why", and never act on borrowed tips.

- Follow a sensible roadmap: emergency fund, clear costly debt, open the account, automate a small SIP, keep learning, add direct stocks slowly.

- Start small and safe, the first goal is the habit and the lessons, not the returns; this is education, not advice.

You now know how to take your first real steps. But the biggest obstacle to investing well is not the market, it is the mind that watches it. Next, we turn to risk, psychology and the common mistakes that quietly defeat most investors, and how to beat them.