The IPO: How a Company Goes Public

The Initial Public Offering, step by step, the RHP, book-building, price band, lot size and listing day, using recent Indian IPOs as live examples.

- ·What an IPO is

- ·The RHP & DRHP

- ·Book-building & price band

- ·Lot size & applying via UPI

- ·Listing day & listing gains

- ·Reading IPO jargon

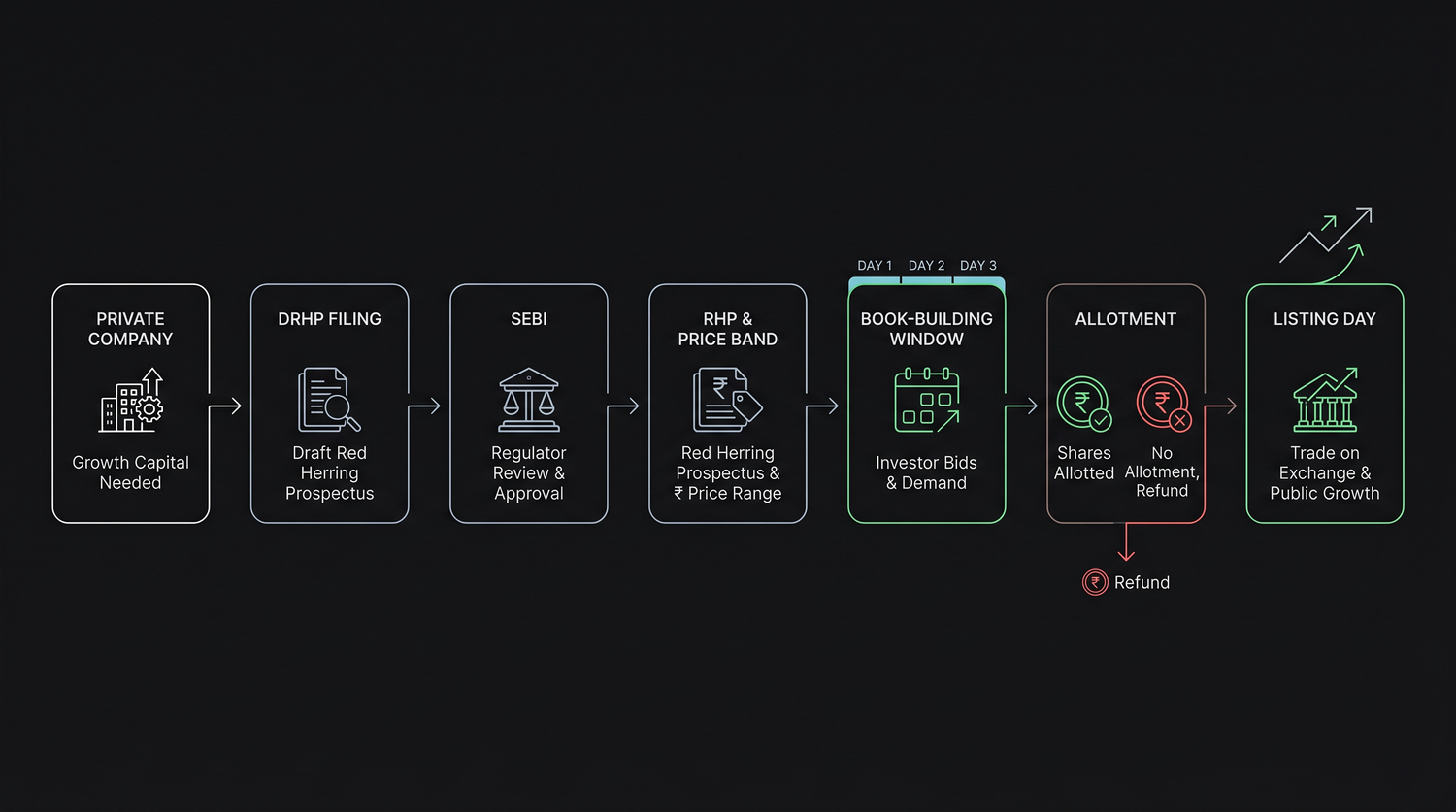

You have almost certainly ridden in a Hyundai car, ordered dinner on Swiggy, or walked through a Vishal Mega Mart. For years each of these was a private company, owned by its founders and a small circle of investors, its shares impossible for an ordinary person to buy. Then, on one specific morning, that changed: their shares appeared on the NSE and BSE, and anyone with a demat account could own a slice. That morning is called a listing, and the months-long journey that leads up to it has a name you have surely heard, the IPO, or Initial Public Offering.

An IPO is one of the most exciting and most misunderstood events in the market. Newspapers shout about "listing gains," WhatsApp groups whisper about "grey market premium," and beginners pile in hoping for a quick double. This chapter walks you calmly through the whole process, from the first thick document a company files to the moment the stock starts trading, so you understand what you are actually applying for.

What an IPO actually is

A company "goes public" when it sells its shares to the general public for the first time. Until then it raised money privately, from founders, angels, venture capital, private equity (the journey we traced last chapter). An IPO opens that ownership to everyone and, in return, the company joins the stock exchange with all the scrutiny, disclosure and discipline that brings.

There are two distinct things that can happen inside an IPO, and they matter a great deal:

- Fresh issue. The company creates brand-new shares and sells them, so the money comes into the company to fund growth, repay debt or build factories.

- Offer for Sale (OFS). Existing owners, founders, early investors, sell some of their shares, so the money goes to them, not the company. The business gets nothing new; the seller simply cashes out.

Many IPOs are a mix of both. It is worth knowing which is which: a fresh issue funds the company's future; a pure OFS is older investors heading for the exit.

An IPO happens in the primary market, shares sold for the first time. Every trade after listing happens in the secondary market, between investors, with no money going to the company at all. Buying on listing day is already the secondary market.

The paperwork: DRHP and RHP

Before a company can ask for your money, it must tell you almost everything about itself. It does this in a thick document filed with SEBI.

- The DRHP (Draft Red Herring Prospectus) is the draft version, filed first and put online for public comment. SEBI reviews it and sends back questions.

- The RHP (Red Herring Prospectus) is the near-final version filed just before the issue opens, now carrying the price band and dates.

The phrase "red herring" survives because the document deliberately omits one key fact until the last moment, the final price. That missing price is the "red herring."

You do not need to read all 600 pages. Skim these sections:

- Objects of the issue, exactly where the money goes (real growth, or mostly an OFS exit?).

- Risk factors, the company's own honest list of what could go wrong.

- Financials, is revenue growing? Is it actually profitable, or burning cash?

- Promoter holding, how much skin the founders keep after listing.

- Basis for the issue price, the valuation, and how its P/E compares with listed peers.

Read the risk factors first, not last. They are written by the company's own lawyers to protect the company, so they are unusually frank. If a risk there genuinely worries you, no amount of listing-day hype should change your mind.

Book-building and the price band

Most large IPOs use book-building: instead of fixing one price, the company offers a price band, say Rs 700 to Rs 740 a share (the real band for HDB Financial Services in 2025), and lets demand discover the final number. Over a three-day window, investors place bids at prices within the band. Once it closes, the company sets the single cut-off price at which shares are allotted.

As a retail investor you can simply bid "at cut-off," meaning you agree to pay whatever final price is decided. That way your application stays valid even if the price is fixed at the top of the band.

Lot size, UPI and the money that gets blocked

You cannot apply for a single share. IPOs are sold in a lot, a fixed bundle. SEBI keeps one retail lot worth roughly Rs 14,000-15,000 (approximate), so a Rs 740 share might come in a lot of 20. That is your minimum application; you can apply for more lots, up to the Rs 2 lakh retail ceiling.

Here is the part beginners love once they understand it. You apply through ASBA, Application Supported by Blocked Amount. Using a UPI mandate, your application blocks the money in your own bank account; it is not debited. The cash sits frozen, still earning your savings interest, until allotment is decided.

Because the money is only blocked, not paid, applying for an IPO costs you nothing if you do not get shares. If you are not allotted, the block is simply released and the money is yours again. If you are allotted, only then is it debited. No allotment, no loss.

Allotment and oversubscription

Good IPOs attract far more demand than there are shares, this is oversubscription. An IPO "subscribed 40 times" received bids for forty times the shares on offer. When that happens, retail investors cannot all be satisfied, so allotment is done by a computerised lottery: each applicant is treated as one entry per lot, and a random draw decides who gets the minimum one lot. Applying for ten lots does not improve your odds of that first lot, everyone competes as equals for it.

Listing day and "listing gains"

On listing day the stock starts trading, and the gap between the issue price and the opening price is the famous listing gain (or loss). The headlines that follow are real, but so is the risk.

| IPO (issue price -> listing price) | Listing day move (approx.) |

|---|---|

| Bajaj Housing Finance (Rs 70 -> Rs 150) | about +114% |

| LG Electronics India (2025) | about +50% |

| Vishal Mega Mart (Rs 78 -> Rs 112) | about +44% |

| HDB Financial Services (Rs 740 -> Rs 835) | about +13% |

| Swiggy (listed near Rs 420) | about +8% |

| Hyundai Motor India (Rs 1,960 -> Rs 1,934) | about -1% (a flop) |

Hyundai Motor India's 2024 IPO was the largest in Indian history at roughly Rs 27,860 crore, and it fell on listing day. Meanwhile Bajaj Housing Finance more than doubled on debut, then drifted down around 26% over the following months. The lesson sits in the same table: a big name is no guarantee of a pop, and a pop is no guarantee it lasts.

The grey market premium, handle with care

Before listing, an unofficial grey market quotes a GMP (Grey Market Premium), a rumoured price at which the not-yet-listed shares are "trading." It is whispered across Telegram groups as a crystal ball for listing gains.

The grey market is unofficial, unregulated and not monitored by SEBI. There is no exchange, no settlement guarantee, no grievance redressal, just trust between anonymous dealers. GMP figures are easily rigged to manufacture hype, and SEBI has repeatedly warned investors against trading unlisted shares on unauthorised platforms. Treat GMP as gossip, never as a reason to invest. SEBI is even building an official "when-listed" trading window precisely to replace this murky corner.

Decoding the IPO jargon

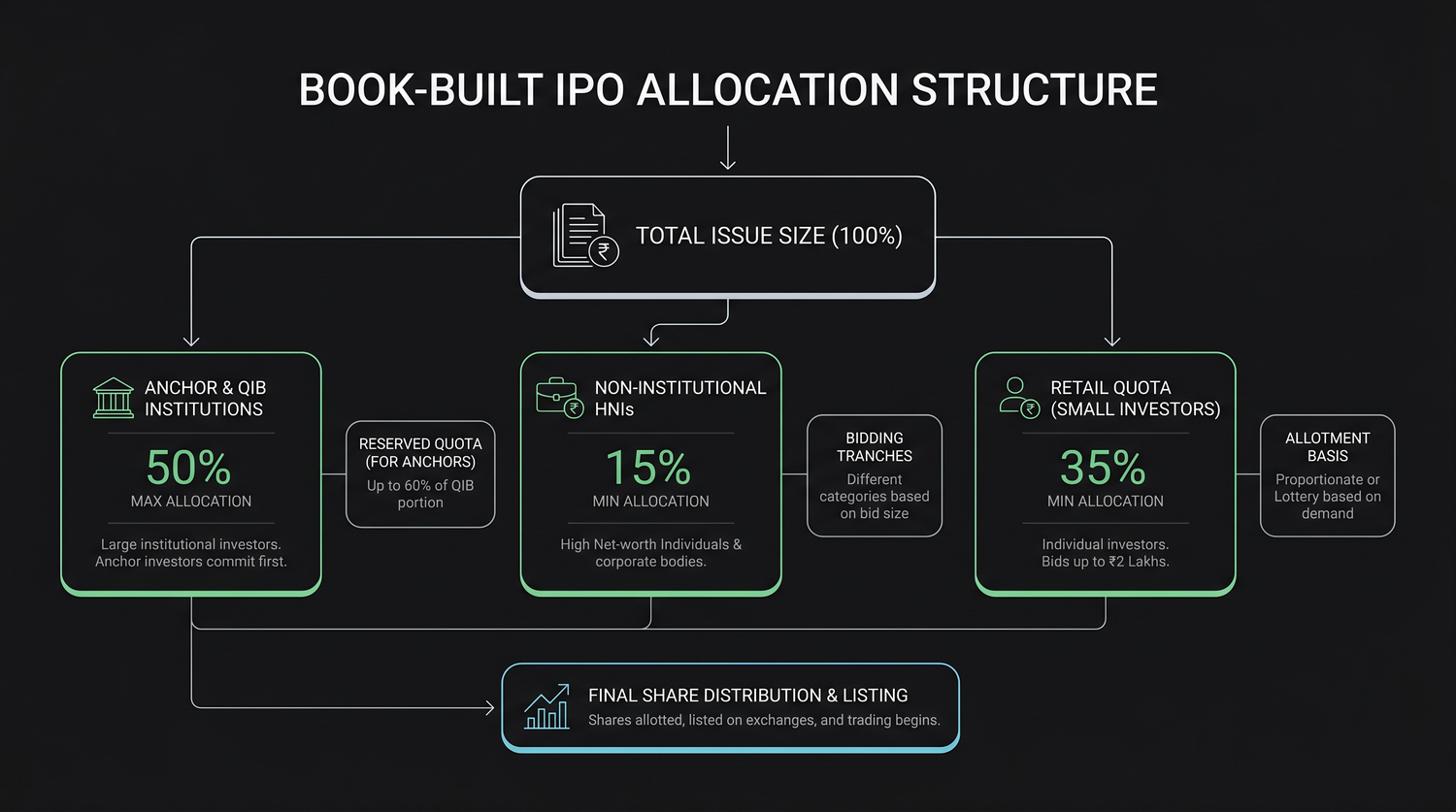

Every IPO is split into reserved buckets for different investor types. The standard book-built split looks like this:

| Category | Who they are | Typical reservation |

|---|---|---|

| QIB (Qualified Institutional Buyers) | Mutual funds, banks, insurers, FIIs | up to 50% |

| NII / HNI (Non-Institutional Investors) | Individuals applying above Rs 2 lakh | at least 15% |

| Retail (RII) | You, applications up to Rs 2 lakh | at least 35% |

Anchor investors are a special slice carved from the QIB quota (up to 60% of it). These are large, marquee institutions invited to commit the day before the IPO opens, their participation signals confidence to everyone else. To stop them flipping for a quick profit, their shares are locked in (half for 30 days, half for 90 days).

One last distinction. A mainboard IPO is a large company listing on the main NSE/BSE platforms with full disclosure. An SME IPO is a small business listing on the dedicated NSE Emerge or BSE SME platforms, with lighter rules and a much bigger minimum application (often over a lakh). SME IPOs can deliver dramatic moves, up and down, and suit experienced investors, not first-timers.

To put the frenzy in perspective: 2024 was a record year with about 91 mainboard IPOs raising roughly Rs 1.6 lakh crore, and 2025 went bigger still, with over 100 mainboard issues. When that much money chases new listings, hype runs hot, and your only real defence is the boring stuff: the RHP, the financials, and the price.

Quick recap

- An IPO sells a company's shares to the public for the first time, in the primary market; all trading after listing is secondary.

- A fresh issue funds the company; an OFS only cashes out existing owners, always check which dominates.

- The DRHP (draft) and RHP (final, with price band) tell you everything; skim the objects, risks, financials and valuation.

- Book-building discovers the price within a band; you apply in lots via UPI/ASBA, where money is blocked, not debited, until allotment.

- Listing gains are never guaranteed, even India's largest-ever IPO fell on debut, and the grey market premium is unregulated rumour.

- IPO shares are split between QIB, NII and retail, with anchor investors locked in to signal confidence.

A company does not stop touching the market after it lists. It keeps raising fresh capital and rewarding shareholders through rights issues, FPOs, OFS, bonuses, splits and buybacks, and each one moves the share price in ways that can frighten a beginner unnecessarily. Decoding those corporate actions is exactly where we go next.