Why You Must Invest

Inflation quietly eats idle cash. See how saving differs from investing, why compounding rewards those who start young, and why a beginner's real edge is not predicting the market, but patiently building assets early.

- ·Saving vs investing

- ·How inflation erodes cash

- ·The magic of compounding

- ·Why you can't (and needn't) predict the market

- ·Start young: time beats timing

- ·What real returns look like

Ask your parents what a plate of idli or a litre of petrol cost when they were your age, and you will hear a number that sounds like a joke today. That quiet, relentless rise in prices has a name, inflation, and it is the single most important reason this course exists. Money left sitting still does not stay still in value; it slowly shrinks. Learning to invest is simply learning to grow your money faster than prices rise, so that your future self is richer than your present self, not poorer.

Here is the good news, and the surprising part: you do not need to be a genius, predict the next crash, or pick the next multibagger to do this well. You need two unglamorous things, time and patience, and the earlier you start, the less of either you need. This first chapter is about why. Everything else in the course is about how.

Saving is not the same as investing

Most people are taught to save, to not spend. That is a good habit, but saving alone is only half the job. Money parked in a regular savings account earns around 3% a year, while prices rise by roughly 5-6% a year. So a "safe" savings account is, in real terms, a slow leak.

- Saving is setting money aside. It protects the rupee amount.

- Investing is putting that saved money to work in assets that grow. It protects (and grows) the rupee's buying power.

The difference sounds small. Over a lifetime it is the difference between scraping by and being comfortable.

Saving keeps your money the same number of rupees. Investing aims to keep, and grow, what those rupees can actually buy. Beating inflation is not optional; it is the whole point.

The silent thief: inflation

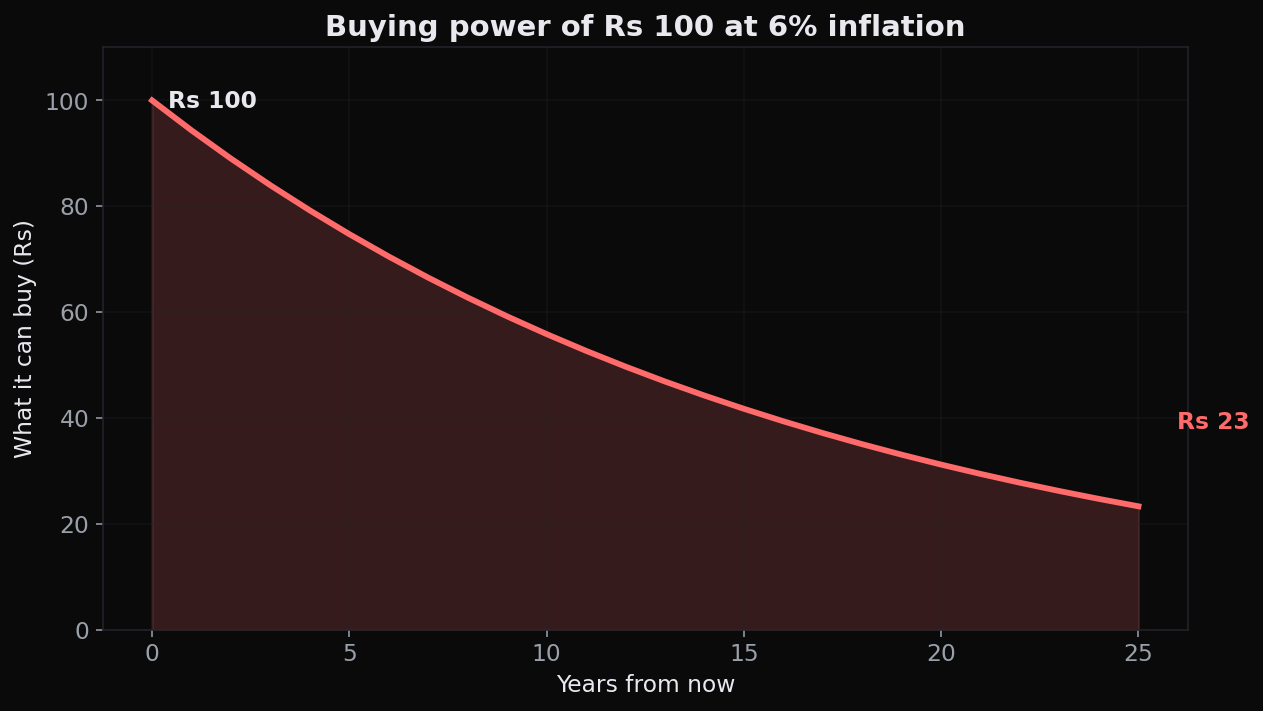

Imagine you tucked Rs 1,00,000 under a mattress in the year 2000. The number on the notes never changed. But at about 6% average inflation, what that Rs 1,00,000 could buy shrank year after year, until, around 25 years later, it buys what roughly Rs 23,000 bought back then. You lost over three-quarters of your purchasing power without spending a single rupee. That is the silent thief at work.

This is why "playing it safe" with only cash and savings accounts is, paradoxically, one of the riskiest things you can do with money you will not need for many years. The risk is not that the number drops, it is that the number stands still while the world gets more expensive.

Compounding: the eighth wonder

Now the magic that works in your favour. When you invest, you earn a return. Next year you earn a return on your original money plus last year's return. The year after, on all of that again. Your money starts earning money, which earns money. This snowball is called compounding, and over long stretches it does things that feel almost unfair.

Consider a simple, real-world habit: investing Rs 5,000 every month into an index fund that compounds at about 12% a year (close to the Nifty 50's long-run average).

| Years invested | You put in | It could grow to (approx.) |

|---|---|---|

| 10 years | Rs 6,00,000 | Rs 11.6 lakh |

| 20 years | Rs 12,00,000 | Rs 50 lakh |

| 30 years | Rs 18,00,000 | Rs 1.76 crore |

Look closely. Tripling the time (10 to 30 years) did not triple the result, it multiplied it more than fifteen times. That is compounding's signature: the longest years do the heaviest lifting, and they are always the last ones. Which leads to the most important lesson in this entire course.

Albert Einstein is often quoted as calling compound interest "the eighth wonder of the world, he who understands it, earns it; he who does not, pays it." Whether he truly said it or not, every long-term investor eventually learns he was right.

Start young: time beats timing

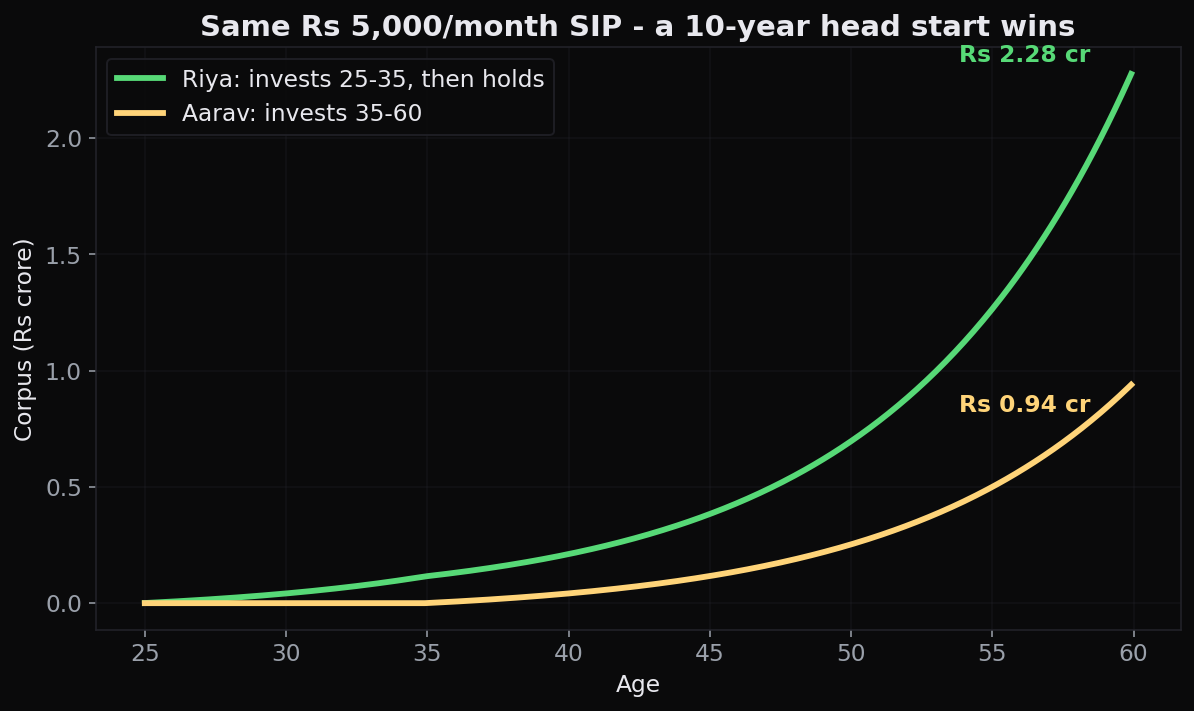

Picture two friends. Riya starts investing Rs 5,000 a month at age 25 and stops at 35, just ten years, Rs 6 lakh in total, then never adds another rupee, letting it compound until she is 60. Aarav does nothing until 35, then invests the same Rs 5,000 a month diligently for the next 25 years, Rs 15 lakh in total. Who ends up with more at 60?

Riya does, comfortably, despite investing less than half as much money. Her secret was not skill or luck. It was a ten-year head start that let compounding run longer. Time in the market did what no amount of clever timing could.

Your single biggest advantage as a young investor is time, not intelligence. Starting at 22 instead of 32 can matter more than every stock you will ever pick. The best day to start was years ago; the second best is today.

Why you can't (and needn't) predict the market

Here is the trap nearly every beginner falls into: believing the goal is to predict what the market will do next week, guess the bottom, and time the perfect entry. Stop. The honest truth is that nobody, not fund managers, not TV experts, not the person with the loudest YouTube channel, can reliably predict short-term market moves. Markets are driven by millions of people reacting to news that has not happened yet. They are, in the short run, genuinely unpredictable.

And the beautiful part is that you do not need to predict anything. The wealth-building engine is not forecasting; it is owning good assets and staying invested through the ups and downs. Studies repeatedly show that investors who try to jump in and out, selling in fear, buying in greed, badly underperform those who simply kept investing steadily and did nothing.

Beware anyone who promises to tell you where the market is heading next week, or guarantees returns. Prediction sells confidence, not results. A beginner's job is not to forecast the market, it is to participate in it patiently, building assets month after month, decade after decade. We return to this discipline in a later chapter on risk and the investor's mind.

Real returns: the number that actually matters

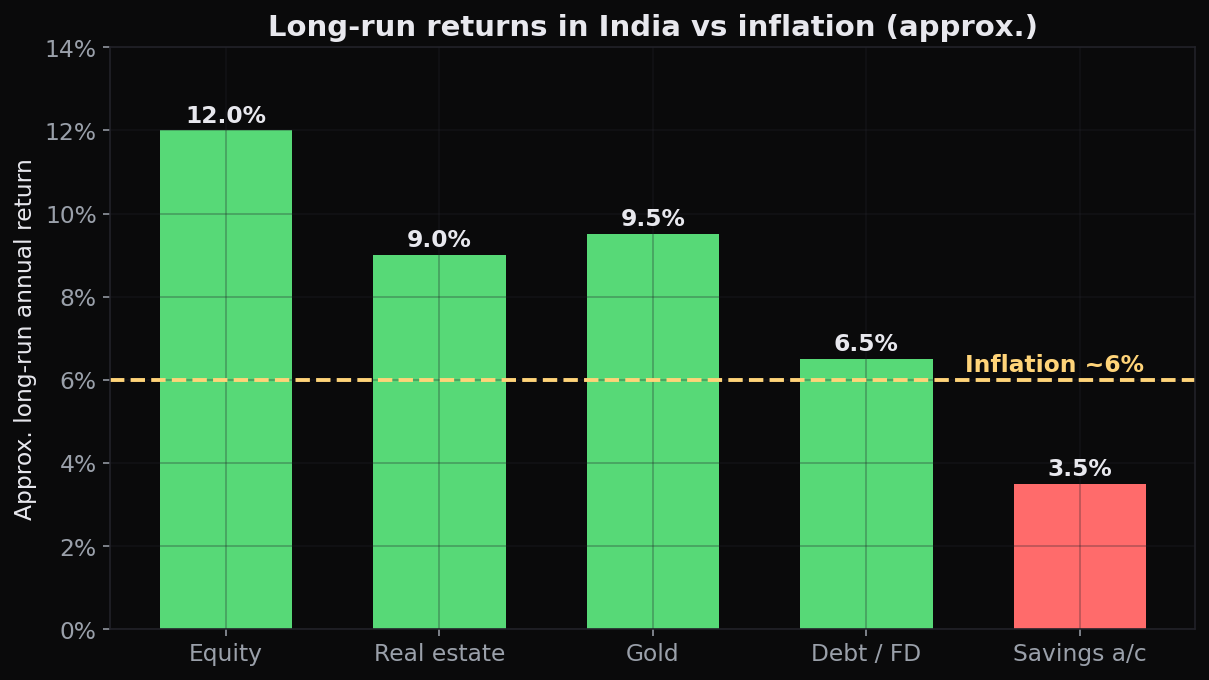

When someone says an investment "gave 9%", always ask: 9% before or after inflation? The headline figure is the nominal return. Subtract inflation and you get the real return, the only one that grows your actual buying power.

- A fixed deposit at 7% with inflation at 6% gives a real return of just ~1%.

- Equities averaging ~12% with the same inflation give a real return of ~6%, six times more useful growth, in exchange for accepting ups and downs along the way.

That trade, accepting short-term bumpiness in return for far higher long-term real growth, is the central bargain of investing in stocks. Over a few months, equities are a roller-coaster. Over a few decades, they have been India's most powerful wealth-builder.

India is investing like never before

This is not a niche pursuit any more. India has crossed 21 crore demat accounts, and monthly SIP contributions into mutual funds run well above Rs 25,000 crore, records that keep breaking. A whole generation of young Indians has realised that a salary alone does not build wealth; invested savings do. You are joining that shift at exactly the right time, with exactly the right idea: start early, stay patient, let compounding work.

Throughout this course, "the market" means the Indian stock market, the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE), and the figures use rupees and Indian examples. Nothing here is investment advice; it is education to help you understand how it all works and make your own informed decisions.

Quick recap

- Inflation silently erodes the buying power of idle cash, "safe" savings quietly lose value over time.

- Saving preserves rupees; investing grows what those rupees can buy. You need both.

- Compounding makes money earn money, and its biggest gains come in the final, longest years.

- Starting young is a beginner's greatest edge: time in the market beats timing the market.

- You cannot and need not predict short-term moves, patient participation, not forecasting, builds wealth.

- Judge investments by real (after-inflation) returns, and accept short-term bumpiness for long-term growth.

Next, we look at where you can actually put your money, the major asset classes, from equity and debt to gold and crypto, and why equities have historically built the most wealth of all.