From Startup to Stock: How Companies Get Funded

Every listed giant started small. Follow the funding ladder, bootstrapping, angels, venture capital, private equity, and how valuations balloon along the way.

- ·The origin of a business

- ·Bootstrapping & angels

- ·Venture capital & PE

- ·Funding rounds & valuation

- ·Dilution explained

- ·Why companies eventually list

Every towering company whose share price scrolls across your screen, Infosys, Zomato, Reliance, was once something almost laughably small: a few people, an idea, and not nearly enough money to make it real. Nobody is born a Rs 1-lakh-crore company. They climb there, one funding round at a time, trading slices of ownership for the cash to grow. By the time a company's shares land on the NSE or BSE for you to buy, it has usually already lived a long, dramatic financial life that you never saw.

This chapter traces that hidden journey, the funding ladder a business climbs from idea to IPO. Understanding it does two things. It demystifies where listed companies actually come from. And it explains why a company eventually decides to sell shares to the public at all, which is, after all, the moment you get to own a piece of it.

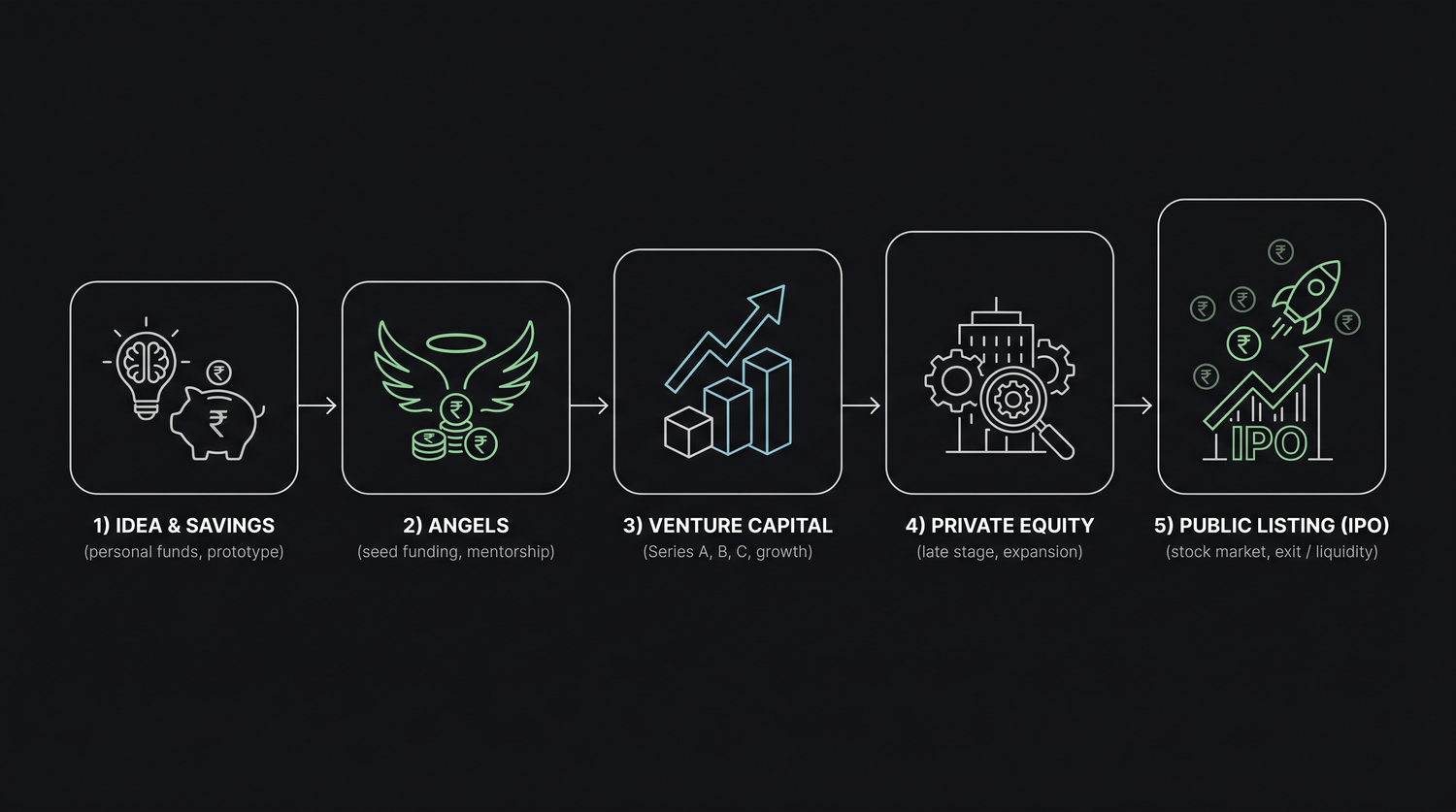

The funding ladder

Picture a ladder. At the bottom is an idea with no money; at the top is a company selling shares to the public. Each rung raises a bit more money from a slightly bigger, more professional source, and at each rung, the founders give up a slice of ownership in exchange. Here is the climb.

Rung 0, the idea

It starts with a problem someone wants to solve and almost no money. At this stage the "company" might just be a pitch deck and a prototype built on weekends.

Rung 1, bootstrapping

Bootstrapping means funding the business with the founder's own money, savings, a credit card, revenue scraped from the first customers. No outside investors, no dilution: the founder owns 100%. The downside is limited fuel; you can only grow as fast as your own wallet allows.

Rung 2, friends, family and angels

When personal savings run dry, founders turn to people who believe in them: friends and family first, then angel investors, wealthy individuals who back very early startups with their own money, often Rs 25 lakh to a few crore, in exchange for a small ownership stake. Angels take enormous risk (most early startups fail) in the hope that one winner pays for all the losers.

Rung 3, venture capital

This is where it gets serious. Venture capital (VC) firms are professional investors who pool money from large institutions and invest it in promising startups in stages called rounds:

- Seed, the first institutional cheque, to prove the idea works.

- Series A, to build a repeatable business once there is early traction.

- Series B, C, D..., progressively larger rounds to scale fast, enter new cities, hire armies, and crush competitors.

Each lettered round typically raises more money at a higher valuation than the last. VCs are not charities, they want the company to become hugely valuable so their stake multiplies.

Rung 4, private equity

As the company matures, even bigger private equity (PE) firms may invest, writing very large cheques into a now-established, often profitable business. PE money tends to come later, in larger amounts, at lower risk than the wild early days.

Rung 5, the IPO

Finally, the company may sell shares to the public for the first time through an Initial Public Offering (IPO), and list on the exchange. This is the top of the ladder, the moment a private company becomes a public one that you and millions of others can own. We dedicate the whole next chapter to it.

The names rise in size as you climb: angels invest lakhs to a few crore, VCs invest crores to hundreds of crore, PE firms and IPOs deal in hundreds to thousands of crore. Bigger rung, bigger cheque, bigger company.

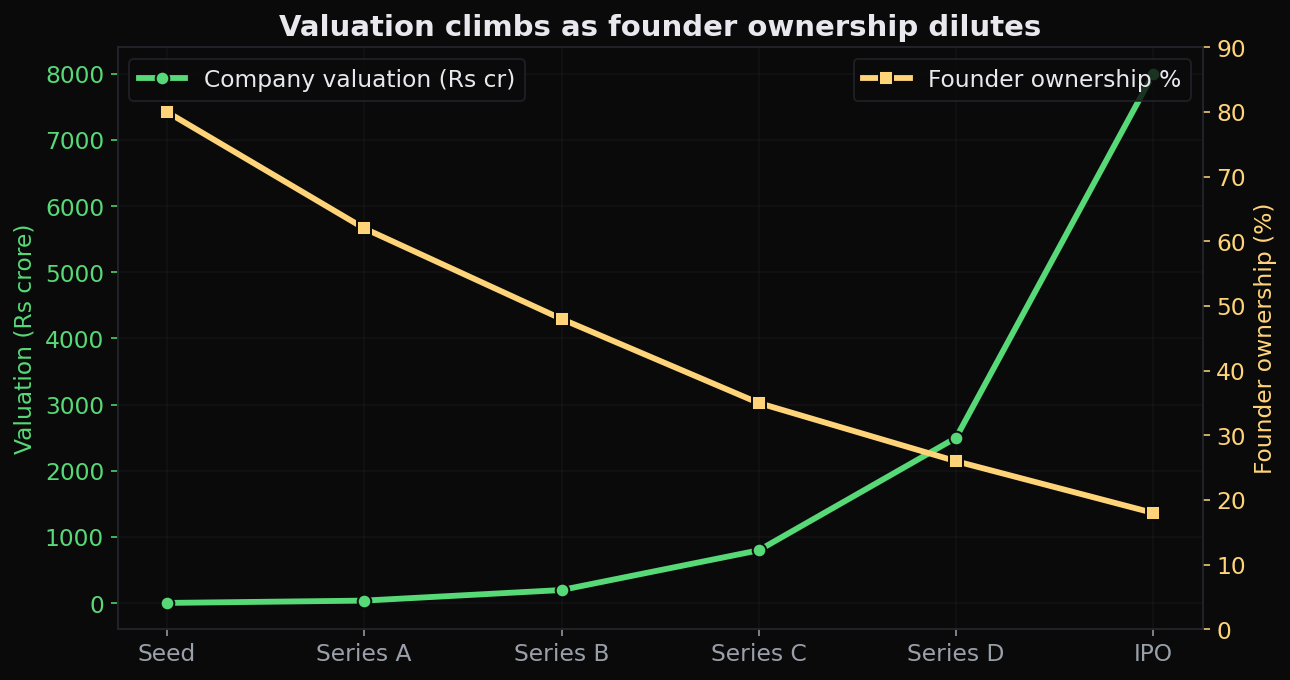

Valuation: what is a company "worth"?

At every rung, two parties haggle over one magic number: the company's valuation, an estimate of what the whole business is worth today. It is not a precise fact but a negotiated opinion, based on revenue, growth rate, the size of the market, the team, and how badly investors want in.

Valuation works through a simple rule. If investors put in Rs 10 crore and receive 20% of the company, they have implicitly valued the whole company at Rs 50 crore (because Rs 10 crore is 20% of Rs 50 crore). Do this repeatedly, and a startup's valuation can balloon from a few crore to thousands of crore across rounds, as each new investor pays more per slice than the last, betting the business keeps growing.

A startup that crosses a valuation of one billion US dollars (roughly Rs 8,000-8,500 crore) earns a special nickname: a unicorn, so called because such companies were once thought as rare as the mythical beast.

The term "unicorn" was coined in 2013 because billion-dollar startups were considered almost mythically rare. They are not so rare any more, India alone is home to well over 100 unicorns as of 2026, one of the largest startup ecosystems on earth. The beast has, it turns out, multiplied.

Dilution: giving up a slice to grow the pie

Here is the trade at the heart of every funding round. To get an investor's money, founders must hand over new shares, which means their own percentage of ownership shrinks. This shrinking is called dilution.

It sounds painful, and beginners often recoil: why would founders keep giving ownership away? The answer is the wisest idea in startup finance: it is better to own a small slice of a huge pie than a big slice of a tiny one. Each round dilutes the founders' percentage but pours in fuel that (if it works) grows the company so much that the value of their smaller slice keeps rising.

Watch how it plays out for a founder who starts owning everything:

| Stage | Company valuation (approx.) | Founder's ownership | Value of founder's stake |

|---|---|---|---|

| Bootstrapped | Rs 2 crore | 100% | Rs 2 crore |

| After seed round | Rs 20 crore | 75% | Rs 15 crore |

| After Series A | Rs 100 crore | 55% | Rs 55 crore |

| After Series B | Rs 500 crore | 40% | Rs 200 crore |

| At IPO | Rs 4,000 crore | 30% | Rs 1,200 crore |

The founder's percentage fell from 100% to 30%, but the value of that stake rose from Rs 2 crore to Rs 1,200 crore. That is dilution working as intended: a smaller fraction of a vastly bigger company. (The figures are illustrative, to show the mechanism.)

Dilution shrinks your percentage but can grow your value. A founder owning 30% of a Rs 4,000 crore company is far richer than when they owned 100% of a Rs 2 crore one. Raising money is not losing the company, it is trading ownership for the fuel to make the whole thing bigger.

Why go public at all?

If venture capital and private equity already supply money, why bother with the noise and scrutiny of a public listing? Companies go public for a handful of powerful reasons:

- Raise large capital, an IPO can bring in hundreds or thousands of crore at once, far more than most private rounds, to fund expansion or pay down debt.

- Let early investors and employees exit, angels, VCs and staff with stock options finally get a public market where they can sell their shares and realise years of paper gains.

- Prestige and visibility, being listed brings credibility, media attention, and trust from customers, lenders and future hires.

The flip side is real: public companies must disclose results every quarter, answer to thousands of shareholders, and live with a share price that judges them daily. Going public is a trade of privacy for capital and liquidity.

A soaring private valuation is not a promise that an IPO will reward public investors. Several richly valued startups have listed and then seen their share price fall hard when public investors demanded profits, not just growth stories. A high last-round valuation is an opinion of insiders, not a guarantee for you. We will look at judging IPOs carefully in the next chapter.

India's startup decade

This whole ladder has come spectacularly alive in India. A wave of startups has climbed from idea to listing in a single decade. Zomato, founded in 2008, rode angel and VC money for years before its blockbuster IPO in 2021. Swiggy followed its rival onto the exchange in late 2024. The result is an ecosystem with well over 100 unicorns and a steady pipeline maturing toward the public market. For you, the investor, this matters: the private journeys of today are the listed stocks of tomorrow.

Zomato's arc in one line: a 2008 restaurant-listings website, funded round after round by angels and VCs through years of losses, listed publicly in 2021 in one of India's most-watched IPOs, turning early private backers into public shareholders and letting ordinary investors finally own a slice. The full funding ladder, climbed in public view.

Quick recap

- Every listed giant began tiny and climbed a funding ladder: idea, bootstrapping, friends/family and angels, venture capital (seed, Series A/B/C...), private equity, and finally an IPO.

- Each rung raises more money from a bigger source, angels in lakhs, VCs in crores, PE and IPOs in hundreds to thousands of crore.

- Valuation is a negotiated estimate of what the whole company is worth; it can balloon across rounds, and a billion-dollar startup is called a unicorn.

- Dilution shrinks founders' percentage but can grow the value of their stake, a small slice of a huge pie beats a big slice of a tiny one.

- Companies go public to raise large capital, let early investors exit, and gain prestige, at the cost of constant disclosure and scrutiny.

- India now has well over 100 unicorns, and recent journeys like Zomato and Swiggy show the full ladder climbed from startup to stock.

Next, we zoom in on the final rung, the IPO itself: how a company actually goes public, what the price band and lot size mean, and how you can apply for shares.