Buyer vs Seller: Who Has the Edge?

Buyers have limited risk; sellers have the odds. Learn the honest trade-off between the two sides, why time decay favours the seller, and why neither is a free lunch.

- ·Buyer: limited risk, low odds

- ·Seller: high odds, large risk

- ·Time decay favours the seller

- ·Probability vs payoff

- ·Why most buyers lose

- ·Choosing a side honestly

Every option that exists has two people attached to it. One paid the premium to hold a right, the other received the premium and took on a duty. We have now stood in both pairs of shoes. We have bought the RELIANCE 1320 call and watched the loss stay capped at about Rs 15,590. We have sold it and watched the loss run off the bottom of the chart. So now we can ask the question that every options trader eventually has to answer honestly for themselves. If buying caps your risk but selling collects the premium and the help of time, which side actually has the edge? The answer is not a slogan. It is a genuine trade-off, and understanding it is what separates a thoughtful trader from a hopeful gambler.

The honest trade-off

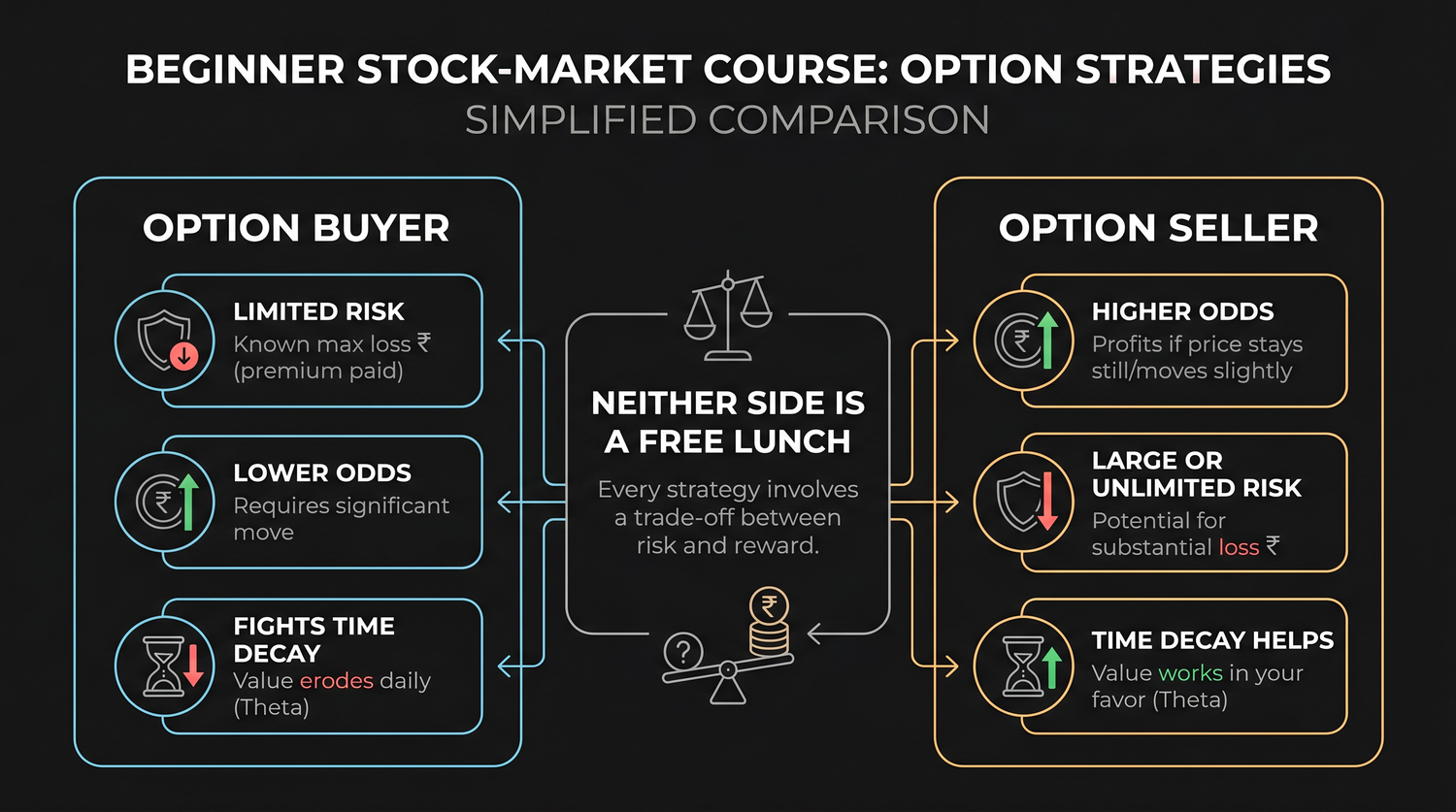

There is no free lunch hiding anywhere in an option. The two sides are mirror images, and every advantage one side enjoys is paid for by a matching disadvantage.

- The buyer has limited risk. The most a call or put buyer can lose is the premium paid, about Rs 15,590 for one RELIANCE lot. But the buyer fights the odds. For the trade to win, RELIANCE must move far enough, and fast enough, to clear the strike plus the premium before 28 July, all while time decay quietly drains the premium every day.

- The seller has the odds and the calendar on their side. Most options expire worthless, so the seller wins more often, and each passing day hands them a little more of the time value they collected. But the seller's reward is capped at the premium received, while the risk behind it is large on a short put and unlimited on a short call.

So neither side is getting something for nothing. The buyer buys a comfortable, capped risk and pays for it by fighting probability. The seller buys favourable probability and pays for it by carrying a heavy tail of risk. The premium is simply the price at which these two trades meet.

Buying and selling are mirror images. The buyer has limited risk and unfavourable odds. The seller has favourable odds and large or unlimited risk. Whatever one side gains in comfort, it gives up in probability, and the other way round.

Probability versus payoff

The cleanest way to see the trade-off is to separate two things that beginners constantly confuse: how often you win, and how much you win or lose when you do.

The buyer of an out-of-the-money option usually loses on any single trade. The stock fails to move enough, time runs out, and the premium goes to zero. But on the rare trade that does work, the payoff can be several times the premium, because the upside on a long call is effectively open ended and the upside on a long put is very large. So the buyer collects many small losses and occasionally one big win. This is a low probability, high payoff shape.

The seller lives in the opposite shape. They collect the premium on most trades because most options expire worthless. Win, win, win, a string of tidy Rs 15,590 collections that feel like a salary. Then, occasionally, a violent move arrives and one loss erases many months of those collections. This is a high probability, low payoff shape with a dangerous tail.

Put the two side by side and the symmetry is exact.

| Option buyer | Option seller | |

|---|---|---|

| Pays or receives | Pays the premium | Receives the premium |

| Maximum loss | Capped at the premium, about Rs 15,590 | Large (short put) or unlimited (short call) |

| Maximum gain | Large or unlimited | Capped at the premium, about Rs 15,590 |

| Helped or hurt by time | Hurt every day by decay | Helped every day by decay |

| Wins most trades? | No, usually loses the small premium | Yes, most options expire worthless |

| The catch | Must be right on direction, size and timing | One bad move can wipe out many wins |

Read that table slowly. Notice that the buyer's column and the seller's column never both look attractive at once. Every row is a swap. That is the whole lesson.

A high win rate is not the same as a profitable strategy. A seller can win nine trades out of ten and still end the year down if the tenth loss is larger than the nine wins combined. Always weigh how often you win against how much you win or lose, never one without the other.

Why most buyers lose

It is worth being blunt, because the marketing around options never is. Most option buyers lose money over time, and the reason is built into the structure, not into bad luck.

To win as a buyer of the RELIANCE 1320 call, three things all have to go right at the same time. You need direction, the stock must rise. You need size, it must rise past the breakeven of 1351, the strike of 1320 plus the Rs 31 premium per share. And you need timing, all of that must happen before 28 July, because after that the option is dead. Being right on one or two of the three is not enough. A trader who correctly guesses that RELIANCE will drift up, but only to 1335, still loses, because 1335 is below the breakeven. The direction was right and the trade still failed.

Meanwhile, the clock charges rent the entire time. Even on a day when RELIANCE rises a little, time decay can quietly cancel the gain, so the premium barely moves. The buyer is running up a down escalator. This is why so many beginners report the strange experience of being right about the market and still losing money on the option. The structure asked them to be right three ways, and the calendar took a cut every day they waited.

Buying out-of-the-money options is the most common way beginners lose money in the market. The option is cheap because it is all hope and no intrinsic value, the odds of finishing in profit are low, and time decay drains it every single day. Cheap does not mean good value.

None of this means selling is the safe answer. The seller swaps the buyer's poor odds for a poor risk shape. Collecting Rs 15,590 again and again feels effortless until the month RELIANCE gaps on news and a single short call costs more than half a year of premiums. The buyer dies by a thousand small cuts. The seller dies by one large wound. Both deaths are real.

Choosing a side honestly

So which side should you be on? The honest answer is that it depends on what you are actually trying to do, and on being truthful with yourself about your edge and your tolerance for risk.

- Lean towards buying when you have a specific, time bound view and you want your downside known to the rupee before you enter. Buying suits a beginner who wants to learn the market with a loss they can name in advance. Just size it as money you can afford to lose entirely, because total loss of the premium is the normal outcome, not the rare one.

- Lean towards selling only when you genuinely understand and can fund the risk, when you have a plan to cap the tail, and when you treat the premium as risk you are renting out, not income you have already earned. Selling rewards discipline and punishes casualness, and it demands margin, which we will return to in the final chapter.

For almost everyone starting out, the right first step is to buy small, define the loss, and learn how the premium actually behaves as RELIANCE moves and as days pass. Rehearse it first in sandbox trading (analyzer mode in OpenAlgo), where you can watch a long call decay and a short call run against you without risking a rupee. Watching the numbers move teaches more than any explanation can.

Before you place any option trade, write down which side of the trade-off you are accepting. If you are buying, accept that you will probably lose the premium and that you must be right three ways to win. If you are selling, accept the large tail and decide your exit before you enter. If you cannot state your side's catch out loud, you are not ready to place the trade.

There is no permanent edge that belongs to one side. The buyer and the seller are simply two ways of taking the same risk, priced so that, on average, neither is a gift. The edge, when it exists, comes from judgement, sizing and discipline, not from the choice of side itself. The next two chapters give you the tools that sharpen that judgement: the Greeks, which measure exactly how an option's price reacts to the world, and implied volatility, which tells you whether the premium you are about to pay is cheap or expensive in the first place.