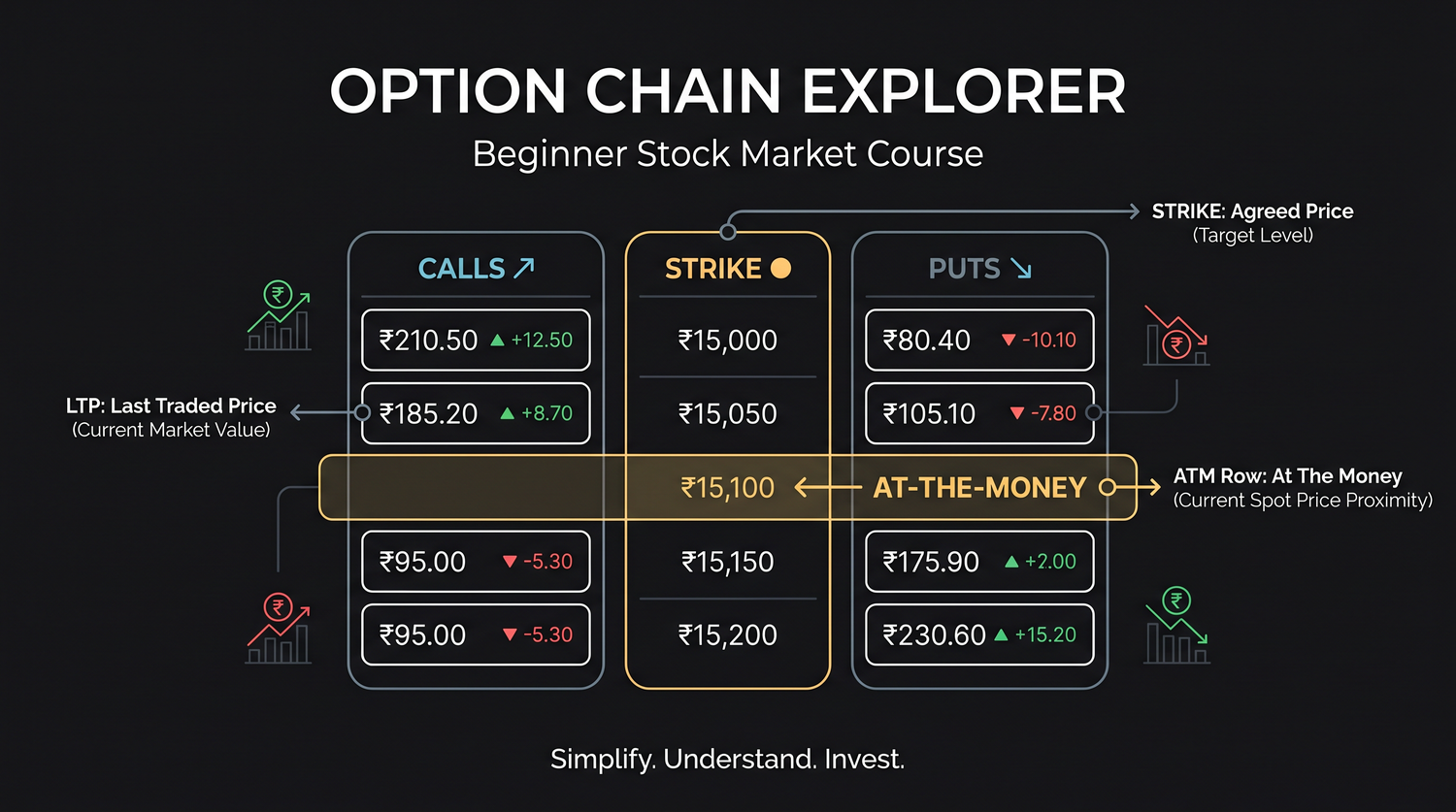

Reading the Option Chain

The option chain is the menu of every strike and its price. Learn to read it row by row, calls on one side, puts on the other, and find the at-the-money strike at a glance.

- ·The layout of a chain

- ·Calls, strikes and puts

- ·LTP, bid and ask

- ·Open interest and volume

- ·Finding the ATM strike

- ·What a chain tells you

Open any options screen and the first thing that hits you is a wall of numbers. Rows and rows of strikes, two columns of prices on either side, a scatter of figures you have never seen before. It looks like a cockpit dashboard, and beginners often close it in a panic. But the option chain is really just a menu. It lists every option available on RELIANCE for a given expiry, with calls down one side, puts down the other, and the strike prices running down the middle like a spine. Once you know which way to read it, the wall of numbers turns into a simple, organised list. This chapter teaches you to read that menu with confidence.

The shape of the chain

Picture a table split into three zones. The strike prices sit in the centre column, climbing from low at the top to high at the bottom. On the left side are all the calls, one row per strike. On the right side are all the puts, again one row per strike. So a single row gives you the call and the put that share the same strike and the same expiry. Read across the row to compare a call and a put at one strike; read down a column to compare the same type across different strikes.

The chain is always tied to one expiry at a time. For our examples that is 28 July 2026, about 32 days out from the 25 June close. If you switch the expiry, the whole chain refreshes with a different set of prices, because options with more time left cost more.

The option chain is a menu, not a maze. Calls on the left, puts on the right, strikes down the middle. One row is one strike, showing its call and its put side by side for the same expiry.

The numbers in each cell

Each call cell and each put cell carries a few figures. These are the ones a beginner needs, in plain words.

- LTP stands for last traded price. It is the premium at which that option most recently changed hands, the figure you will roughly pay or receive. For the RELIANCE 1320 strike, both the call and the put sit near Rs 31 a share, which is about Rs 15,590 for one lot of 500.

- Bid is the highest price a buyer is currently willing to pay for that option right now. Ask is the lowest price a seller is currently willing to accept. If you buy at market, you tend to pay near the ask; if you sell at market, you tend to receive near the bid. The gap between them is the spread, and a wide spread is a cost you quietly pay on the way in and the way out.

- Volume is how many contracts of that option have traded so far today. High volume means the option is active and easy to get in and out of.

- Open interest, often shown as OI, is the number of contracts currently open and not yet closed. Think of volume as today's footfall and open interest as how many people are still in the building. A strike with heavy open interest is one the market is paying attention to.

For a beginner, the two figures that matter most are LTP, so you know the price, and open interest with volume, so you know whether the option is liquid enough to trade without a painful spread. A thinly traded strike with almost no volume can be hard to exit at a fair price.

Finding the at-the-money strike at a glance

The one strike everyone looks for first is the at-the-money strike, the one sitting closest to the current spot price. With RELIANCE near Rs 1,318, the nearest listed strike is 1320, so 1320 is the at-the-money row. It is the natural centre of the chain, and most screens highlight it or scroll to it automatically.

Why does it matter? Because the at-the-money strike is the dividing line for moneyness.

- For calls, every strike below the spot is in-the-money, and every strike above the spot is out-of-the-money. So on the call side, the rows above the 1320 line are in-the-money, and the rows below it are out-of-the-money.

- For puts, it is the mirror image. Strikes above the spot are in-the-money, and strikes below are out-of-the-money. So on the put side, the rows below the 1320 line are in-the-money.

Once you can find the at-the-money row, the whole chain orients itself around it. You instantly know which calls carry real intrinsic value and which are pure hope, just from where they sit relative to that line.

To find the at-the-money strike, look for the listed strike nearest the current spot. For RELIANCE at 1318, that is 1320. From there, calls get cheaper as you read down to higher strikes, and puts get cheaper as you read up to lower strikes.

A small RELIANCE chain to read

Here is an illustrative slice of the RELIANCE 28 July chain around the at-the-money strike. The premium figures are rounded and for teaching only, but they follow the real shape: deep strikes carry more intrinsic value, and the at-the-money 1320 row sits near Rs 31 on both sides.

| Call LTP | Call OI | Strike | Put LTP | Put OI |

|---|---|---|---|---|

| 42 | 1,80,000 | 1300 | 24 | 2,40,000 |

| 36 | 1,30,000 | 1310 | 28 | 1,60,000 |

| 31 | 3,10,000 | 1320 | 31 | 3,40,000 |

| 26 | 1,50,000 | 1330 | 37 | 1,20,000 |

| 21 | 2,00,000 | 1340 | 44 | 90,000 |

Read it slowly and the patterns jump out. The 1320 row is the at-the-money row, the centre of gravity, and notice it carries the heaviest open interest on both sides. As you move down the call column to higher strikes, the call premiums fall, because those calls need a bigger move to pay off. As you move up the put column to lower strikes, the put premiums fall, for the same reason. The 1300 call costs more than the 1320 call because it is already 18 rupees in-the-money, carrying real intrinsic value. The 1340 put costs more than the 1320 put because it is already 22 rupees in-the-money.

Reading one row. The 1320 row shows a call LTP of 31 and a put LTP of 31. Both are about Rs 15,590 a lot. The call is the right to buy RELIANCE at 1320, the put is the right to sell at 1320, and at this strike near the spot, the market prices both sides almost the same.

What the chain is telling you

The chain is not just a price list. Read as a whole, it carries information.

- Where the premiums are cheap and where they are dear. Far out-of-the-money options cost little because they are all time value and need a big move. Deep in-the-money options cost a lot because most of their price is real intrinsic value.

- Where the crowd is positioned. Strikes with unusually heavy open interest show where large numbers of traders have placed bets. Many traders watch big open-interest strikes as rough markers of where the market expects support or resistance, though this is a clue and never a guarantee.

- How liquid each strike is. Volume and open interest together tell you whether you can get in and out cleanly. Stick near the active, at-the-money strikes when you are starting out, because the far, thin strikes can trap you in a wide spread.

A word of honesty. The chain refreshes constantly with the latest market data, but no row on it predicts the future. It tells you what each right costs and how busy each strike is. It does not tell you which way RELIANCE will go. Beginners sometimes read heavy open interest as a sure signal and get burned. Treat the chain as a well-organised menu of prices and activity, not a crystal ball.

A busy strike is easy to trade, but liquidity is not direction. Heavy open interest at 1320 tells you many traders are positioned there. It does not tell you whether RELIANCE will rise, fall, or sit still by 28 July. The chain prices the options; it does not call the move.

Spend a few minutes reading a real RELIANCE chain with this map in your head. Find the at-the-money row near 1320. Notice the calls falling in price as strikes rise, the puts falling as strikes drop, and the intrinsic value hiding inside the deeper strikes. Once the menu stops looking like a wall of numbers and starts looking like an organised list, you are ready to actually buy something. In the next chapter we do exactly that, with the most intuitive trade of all: buying a call.