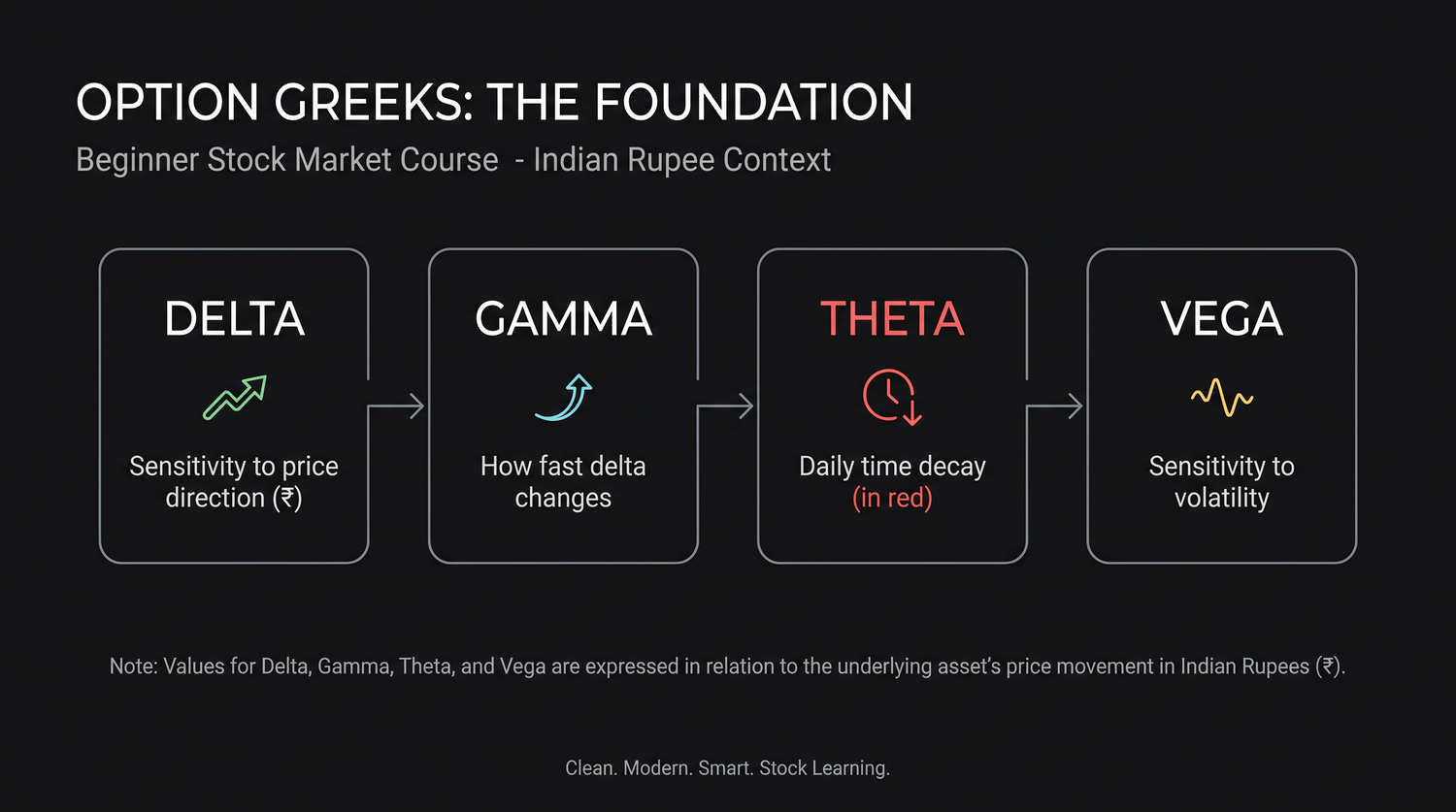

The Greeks: Delta, Gamma, Theta, Vega

The Greeks measure what moves an option's price. Learn delta (direction), gamma (acceleration), theta (time decay) and vega (volatility) in plain words, no formulas.

- ·Delta: sensitivity to price

- ·Gamma: how delta changes

- ·Theta: the daily time decay

- ·Vega: sensitivity to volatility

- ·Why theta is the buyer's enemy

- ·Reading the Greeks simply

You have probably heard traders throw around words like delta and theta as if they were secret code. They are not. The Greeks are simply four plain questions about how an option's premium reacts to the world around it. When RELIANCE moves a rupee, how much does my option move? When a day passes, how much do I lose just to the calendar? When the market gets nervous, what happens to my premium? Each Greek answers one of these questions with a single number. You do not need any mathematics to use them, and in this chapter there will be none. We will keep every Greek in plain English, anchored to the real RELIANCE 1320 option, so that by the end you can read an option the way you read a weather forecast.

Delta: how much the premium moves

Delta answers the most basic question of all. If RELIANCE moves up by one rupee, how much does my option premium move? Delta is the answer, quoted as an amount between zero and one for calls, and between zero and minus one for puts.

Take the RELIANCE 1320 call, sitting at-the-money with the spot near 1318. An at-the-money option has a delta of about 0.5. That means if RELIANCE rises by one rupee, the call premium rises by roughly fifty paisa per share. If RELIANCE falls by one rupee, the premium falls by about the same. The put behaves as the mirror. A 1320 put has a delta of about minus 0.5, so it gains about fifty paisa when RELIANCE falls a rupee and loses about that when RELIANCE rises.

Delta also shifts as the option moves in and out of the money.

- A deep in-the-money option has a delta near one. It moves almost rupee for rupee with the stock, because it behaves almost like holding the shares themselves.

- An at-the-money option has a delta near 0.5. It captures about half of each move.

- A far out-of-the-money option has a delta near zero. The stock can wander and the premium barely flickers, because the strike is so far away.

There is a second, very useful way to read delta. It gives you a rough feel for the chance the option finishes in-the-money. A delta of about 0.5 on the at-the-money call says, loosely, that the market sees roughly even odds of the call expiring with intrinsic value. A delta of 0.15 on a far out-of-the-money call whispers that the odds of it paying off are slim. This is not an exact probability, but as a gut feel it is genuinely useful.

Delta is how much the premium moves for each one rupee move in RELIANCE. About 0.5 at-the-money, near one deep in-the-money, near zero far out-of-the-money. It also gives a rough feel for the chance the option finishes with intrinsic value.

Gamma: how fast delta itself changes

Delta is not fixed. As RELIANCE moves, the delta of your option changes too, and gamma is the Greek that measures how fast that happens. If delta tells you your current speed, gamma tells you how quickly that speed is changing.

This matters because an at-the-money option has the highest gamma. Around the strike of 1320, a small move in RELIANCE can swing the delta noticeably. A call that had a delta of 0.5 can jump towards 0.6 after a modest rally and slip towards 0.4 after a modest fall. So the option's sensitivity to the stock is itself lively and shifting exactly where the spot sits now.

Deep in-the-money and far out-of-the-money options have low gamma. Their deltas are already pinned near one or near zero, so they have little room to change. Gamma is strongest near the strike and strongest as expiry approaches, which is why options can feel calm for weeks and then suddenly whip around in the final days near the money.

For a beginner, the practical takeaway is simple. High gamma means your option's behaviour can change quickly, so a position that felt sleepy can come alive fast near the strike close to expiry. You do not need to calculate gamma. You just need to respect that delta is a moving target, and gamma is the reason.

Gamma is the rate of change of delta. It is highest for at-the-money options near expiry. That is why an option sitting right at the strike a day or two before 28 July can swing in value far more sharply than the same option did a month earlier.

Theta: the daily rupee bleed

Theta is the Greek every option buyer learns to fear. It measures the time decay we met in an earlier chapter, expressed as the amount of premium your option loses each day purely because one more day has passed, with everything else held still.

Suppose the RELIANCE 1320 call has a theta of about one rupee a day at this point in its life. That means, if RELIANCE simply sits at 1318 and nothing else changes, the call quietly loses about one rupee of premium per share overnight, which is about Rs 500 on a lot of 500. The next night, a little more. The stock did nothing, the news was quiet, and yet the option is worth less every morning. That steady leak is theta at work.

Two features of theta are worth burning into memory.

- Theta is largest for at-the-money options, because they carry the most time value, and time value is exactly what decays.

- Theta accelerates as expiry nears. The daily bleed is gentle with 32 days left and becomes brutal in the final week, when the last of the time value collapses towards zero.

This is why theta is the buyer's enemy and the seller's friend. The buyer owns the melting time value and pays theta every day. The seller collected that time value upfront and gets to keep a little more of it with each day that passes quietly. Theta is the rent on hope, and it always flows from the buyer to the seller.

Theta works against you every single day you hold a bought option. You can be right about direction and still lose, because the daily bleed outruns a slow or small move. The closer expiry gets, the faster the bleed, so a long option held into the final week is fighting a rising headwind.

Vega: sensitivity to fear

The last Greek measures something less obvious than price or time. Vega tells you how much your option premium changes when the market's expectation of movement, its implied volatility, rises or falls. We give implied volatility a full chapter next, so for now think of it as the level of fear and expectation baked into the price.

When implied volatility rises, options become more expensive across the board, and vega is the Greek that captures how much your particular option gains from that. When implied volatility falls, options get cheaper, and vega measures how much you lose. Crucially, this can happen even if RELIANCE itself has not moved at all. The stock can sit perfectly still while your premium swells or shrinks simply because the market grew more or less nervous about the future.

At-the-money options with plenty of time left have the highest vega, so they react most to shifts in fear. A long option held through a calming market can lose value to falling volatility even as the buyer waits patiently for a move. This is the trap behind the IV crush we will study next, and vega is the dial that measures it.

RELIANCE sits flat at 1318 for a week. The 1320 call still loses value, for two separate reasons working together. Theta bled off some time value as days passed, and a drop in implied volatility, measured by vega, shaved off more. Same stock price, lower premium, twice over. This is how a buyer can be patient, be right that the stock has not fallen, and still watch the option fade.

Reading the four together

You never trade a single Greek in isolation. They describe the same option from four angles at once, and a real position is the sum of all four. Here is the whole picture on one card.

| Greek | The question it answers | Buyer feels it as |

|---|---|---|

| Delta | How much does the premium move per one rupee in RELIANCE? | The engine of profit when right on direction |

| Gamma | How fast does delta itself change? | Why the option can suddenly speed up near the strike |

| Theta | How much premium leaks away each day? | The daily enemy, the rent on hope |

| Vega | How much does a change in implied volatility move the premium? | A hidden gain or loss even when the stock is still |

Put together, the Greeks explain almost everything strange that an option does. Why a call barely moved when RELIANCE rose, because its delta was small and far out-of-the-money. Why it lost value over a quiet week, because theta and vega both worked against it. Why it suddenly came alive near the strike close to expiry, because gamma spiked. You do not have to compute any of them by hand. OpenAlgo can report the Greeks for any RELIANCE strike, and reading them turns the premium from a mysterious blinking number into something you can actually understand.

Before buying an option, glance at its delta and theta together. Delta tells you how much you stand to gain if you are right on direction, and theta tells you how much you bleed each day while you wait. If the daily bleed looks large against the move you expect, the trade is fighting the clock harder than it looks.

The Greeks measure how an option reacts. The one thing they all quietly depend on is implied volatility, the market's expectation of how much RELIANCE will move. That single number decides whether the premium you are about to pay is cheap or expensive in the first place, and it is the subject of the next chapter.