Risk Management and the Classic Mistakes

How beginners actually blow up, and how to not. Learn position sizing by the premium at risk, knowing your max loss before entry, stop-loss versus defined-risk thinking, and the recurring mistakes from far-OTM lottery buying to selling naked without understanding margin.

- ·Sizing by premium at risk

- ·Know your max loss before entry

- ·Stop-loss vs defined risk

- ·Avoiding revenge trades at expiry

- ·The classic beginner mistakes

- ·When NOT to trade options

Nobody blows up an account by being wrong once. People blow up by being wrong in a way that was too large to survive, or by repeating a small mistake until it became a large one. Almost every beginner who loses badly at options does it through the same short list of avoidable errors, and almost every one of those errors is about risk, not about direction. You can be a poor forecaster and still survive for years if your risk is controlled. You can be a brilliant forecaster and be wiped out in a month if it is not. This chapter is the one to reread, because it is less about being right and more about staying alive long enough to get good.

Size the position by the premium at risk

The first discipline is the simplest and the most ignored. Position sizing means deciding, before anything else, how much money this single trade is allowed to lose. For a long option, that number is easy and brutal: the entire premium you pay can go to zero. An option that finishes out-of-the-money on expiry is worth nothing at all, so the full premium is genuinely at risk, every time.

That changes how you should think about a single lot. One RELIANCE 1320 option costs about Rs 31 a share, which is about Rs 15,590 for one lot of 500, and all of it can vanish. If your trading account is Rs 2 lakh, that one lot already puts nearly eight percent of your whole account on a single option that can expire worthless. Put on three lots and you have risked almost a quarter of your account on one bet that has to be right on direction, size and timing all at once.

A sane rule is to cap the premium you put into any one option at a small fraction of your account, often in the region of two to five percent, so that a total loss on that trade is a bruise and not a wound. The exact number is yours to choose. The point is that you choose it deliberately, before you enter, and not in a panic afterward.

For a long option, your position size is your maximum loss, because the premium can go to zero. Decide what you are willing to lose on the trade first, then work out how many lots that allows. Never reverse the order by buying the lots you want and discovering the risk later.

Know your maximum loss before you enter

Tied to sizing is a habit that separates traders from gamblers: you should be able to state your maximum loss out loud before you click the buy. For the structures in this course it is not hard to know.

| Position | What you do | Maximum loss before entry |

|---|---|---|

| Long call or long put | Pay the premium | The premium paid, about Rs 15,590 per RELIANCE lot, and no more |

| Short call (naked) | Collect the premium | Large and effectively unlimited as the stock rises |

| Short put (naked) | Collect the premium | Very large as the stock falls toward zero |

The buyer's side is comforting and the seller's side is sobering, and that is the honest picture. A naked seller does not just risk the premium collected. A naked short index option blocks roughly Rs 1.5 lakh to Rs 1.8 lakh of margin per lot precisely because the loss can run far past the premium received. If you cannot say your maximum loss in a single sentence before you enter, you are not ready to take the trade.

Selling options naked because the premium looks like easy income is how beginners take a small, steady credit and one day hand back many times that amount on a single gap. The premium you collect is tiny next to the loss you have accepted. Never sell naked until you genuinely understand the margin and the risk you are carrying.

Stop-loss thinking versus a defined-risk structure

Most traders are taught to use a stop-loss, an order to exit once the loss reaches a set level. Stops are useful, but options punish naive stops harder than stocks do. Option prices gap, especially on illiquid strikes and around events, so your stop may not fill anywhere near the level you set. A stop at a certain premium is a wish, not a guarantee, when the market jumps straight through it.

The stronger idea is to build the risk limit into the trade itself. A defined-risk structure is one where the worst outcome is fixed by the position, not by an order that has to fill in time. The plainest defined-risk trade you already know is simply buying an option: your loss cannot exceed the premium no matter how violently the stock moves, because you owe nothing beyond what you paid. The next course builds on this idea with spreads, where a bought option caps the loss of a sold one, so that even a naked-looking sale becomes a trade with a known, capped maximum loss. The lesson for now is that structure beats willpower. A loss that is capped by the position cannot be widened by a fast market or a slow finger.

Prefer a structure whose worst case is fixed before you enter over a stop-loss order that has to execute in a fast market. The best risk control is the one that does not depend on you reacting correctly under pressure.

Avoid revenge trades, especially on expiry day

The most expensive trades are emotional ones. A revenge trade is the one you take to win back a loss you just suffered, sized too big and chosen too fast, because you are angry rather than analytical. The market does not know or care that you are down, and trying to force it to pay you back is how a manageable loss becomes a ruinous day.

Expiry day is where this turns lethal. On the last day, cheap out-of-the-money options are everywhere, time value is collapsing by the hour, and the temptation to double down on a lottery ticket to recover a loss is enormous. It is precisely the wrong moment. Theta is at its most brutal, the odds on a far option are at their worst, and your judgment is at its weakest after a loss. The discipline is plain: when you feel the urge to immediately make it back, that is the signal to stop trading for the day, not to size up.

Chasing a loss with a bigger, faster trade is the single most common way a bad day becomes a blown account. This is at its most dangerous on expiry day, when cheap options and collapsing time value tempt you to gamble your way back to flat. Walk away from the screen instead.

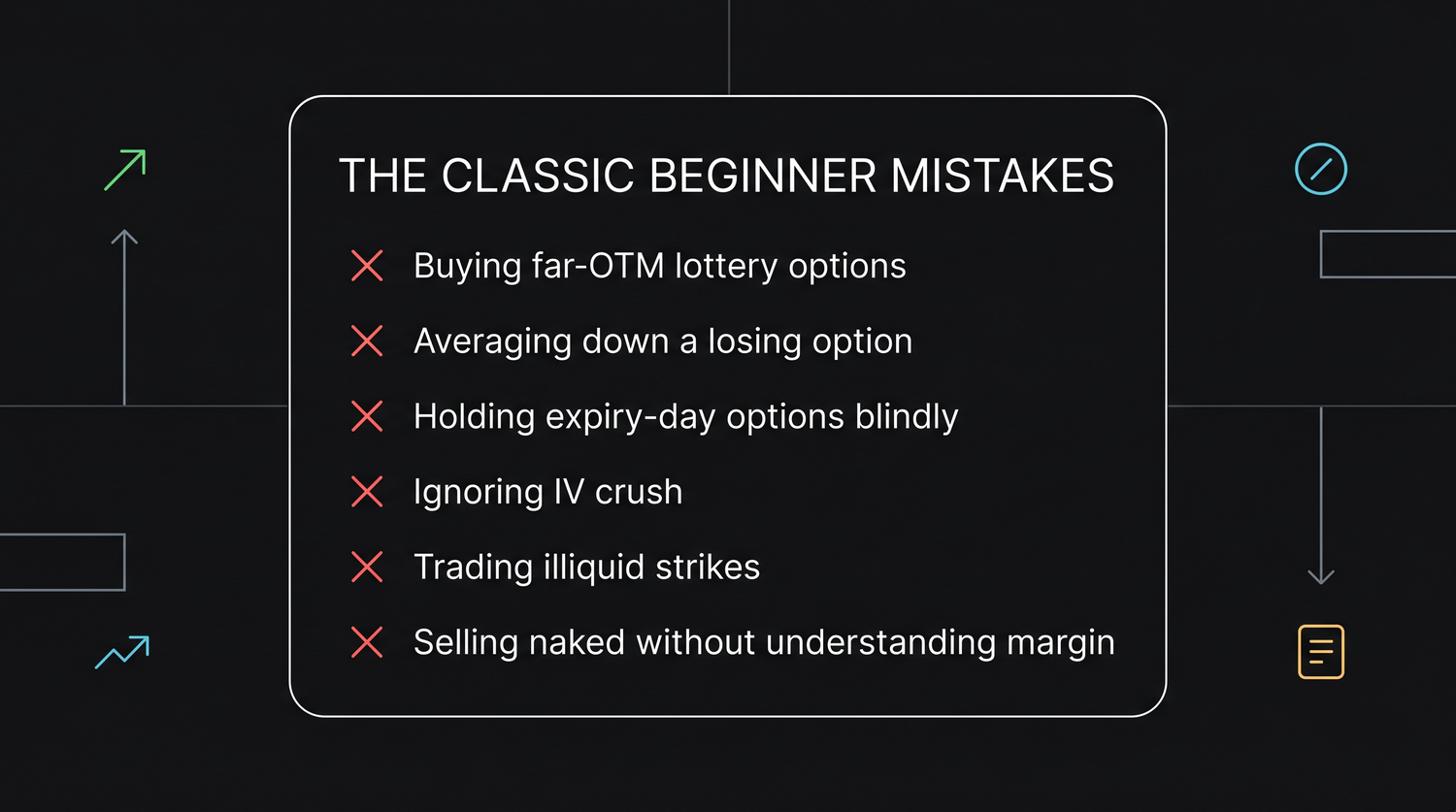

The recurring mistakes

Almost every beginner disaster is one of a handful of repeating errors. Learn to recognise them by name and you will catch yourself in the act.

- Buying far-out-of-the-money lottery options. They are cheap because they are unlikely. The premium is all time value and hope, and the great majority expire worthless. The occasional jackpot story hides a long line of quiet total losses.

- Averaging down on a losing option. Adding more to an option that is falling is adding money to a melting, time-decaying asset. Unlike a share, an option has an expiry, and if it is out-of-the-money at the end it is worth nothing no matter how low your average price is.

- Holding an expiry-day option blindly. Time value is gone, an out-of-the-money option dies worthless, and a stock option that finishes in-the-money can hand you an unwanted delivery or assignment obligation worth several lakh. Square off in time rather than hoping into the close.

- Ignoring the IV crush. Buying expensive premium right before a known event, then watching implied volatility collapse afterward, loses money even when you are right on direction. Respect the event calendar.

- Trading illiquid strikes. A far, thinly traded strike has a wide gap between the bid and the ask, so you overpay to enter and get a poor price to exit, and in a fast market you may not be able to get out at all.

- Selling naked without understanding the margin. Collecting a small premium while carrying large, undefined risk and a heavy margin block is the seller's classic trap, and one gap can erase months of credits.

Notice that none of these mistakes are about predicting the wrong direction. Every one of them is a risk-management failure: too much hope, too much size, too little liquidity, or too little respect for time and events. Fix the risk and most of the losing fixes itself.

When NOT to trade options

Discipline is as much about the trades you skip as the ones you take. Step away from the option screen entirely when any of these are true.

- You cannot state your maximum loss and your breakeven, after charges, before you enter.

- You are trying to win back a loss you just took. That is the worst possible reason to trade.

- The strike is illiquid, with a wide bid-ask gap and thin volume and open interest. You may not be able to exit.

- A known event is about to crush implied volatility and you would be buying inflated premium into it.

- It is expiry afternoon and you are tempted by cheap out-of-the-money options as a way to get lucky.

- You would be selling naked without understanding the margin, the assignment risk and the delivery obligation on a stock option.

- The money at risk is money you actually need, for living costs, for a loan, or for anything that cannot be lost.

None of this is meant to frighten you away from options. Used with control, an option is one of the few instruments that lets you take a sharp, defined-risk view with a known worst case. The danger is never the tool. It is the unsized bet, the revenge trade, the lottery ticket and the naked short taken without respect. Get the risk right and you buy yourself the one thing that actually makes traders good over time, which is survival. The final chapter turns toward that future: how spreads let you define risk on purpose, and a simple checklist to run before every trade you ever place.