Event Risk: Results, Policy and Budgets

Options live and die around events. Learn how implied volatility expands before a known event like results, an RBI policy, the Budget or a Fed meeting, and crushes right after, so a correct directional call can still lose money.

- ·What counts as an event

- ·IV expansion before the event

- ·IV crush right after

- ·Why buyers get hurt on events

- ·How sellers use events

- ·Trading around an event safely

Most of what you have learned so far treats an option's price as a smooth thing. It drifts with the stock, it bleeds a little time value each day, and the picture feels orderly. For long stretches that is exactly how an option behaves. But the calendar is not smooth. Scattered through it are dates that everyone can see coming: results day for a company, an RBI policy meeting, the Union Budget, a national election result, a US Fed decision. Around those dates an option's premium does something violent that has very little to do with whether you guessed direction right. It swells beforehand and collapses afterward. Learning that rhythm is the difference between using events and being quietly destroyed by them.

Options live on a calendar of events

An event, for an option trader, is a scheduled moment when a large lump of new information hits the market all at once. The key word is scheduled. Everyone can see the date in advance, so the market does not wait to be surprised. It prepares.

These are the events that move Indian options the most.

- Company results. RELIANCE reports its quarterly numbers on a known date. The stock can gap sharply when those numbers and the management commentary land.

- RBI monetary policy. The interest-rate decision and the central bank's tone move banks, rate-sensitive stocks and the index together.

- The Union Budget. A single afternoon that can re-price entire sectors at once.

- Elections. National or state results are a binary lump of news, and the index can swing hard on the outcome.

- Global events such as a US Fed meeting. A foreign central bank decision still ripples into NIFTY through global risk sentiment.

The common thread is that the date is public and the outcome is unknown. That combination, a known date with an unknown result, is exactly what an option's price is built to react to.

An event is a scheduled drop of big news on a date the whole market already knows. Because the date is public, the option market prepares for it in advance, and most of the damage to a buyer happens through the premium, not through the direction of the stock.

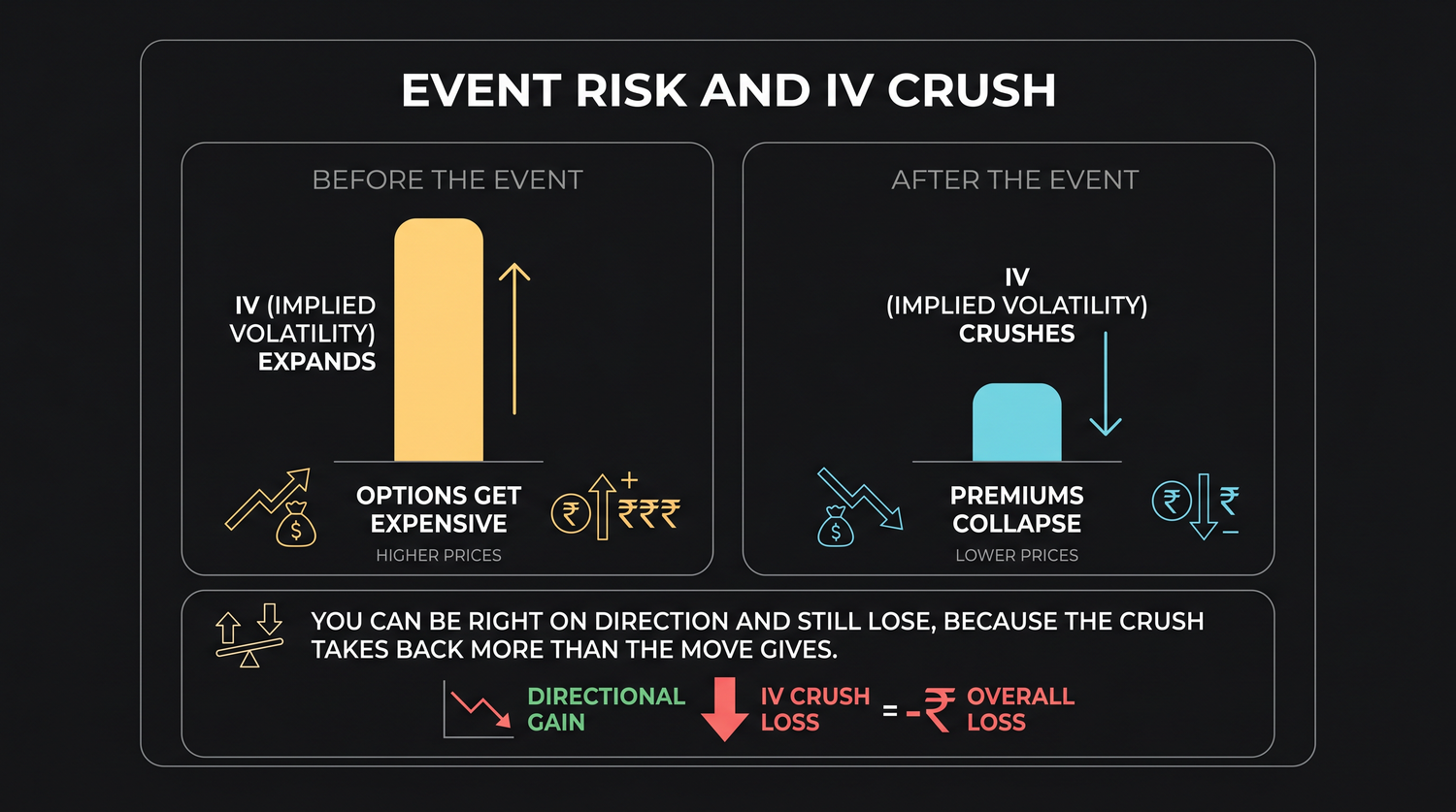

Before the event: implied volatility expands

You met implied volatility earlier as the market's fear gauge, the expected size of the move baked into the premium. An event is the purest example of that gauge climbing. In the days before a known event, traders crowd into options to position for the possible jump, and that demand, together with the genuine uncertainty, pushes implied volatility higher. The premium fattens.

Watch it on the RELIANCE anchor. In a calm market the 1320 call costs about Rs 31 a share, which is about Rs 15,590 for one lot of 500. Walk into the week before results and that same call, same strike, same expiry, can cost far more, perhaps Rs 50 a share or higher, not because the stock moved but because the market is now pricing in a large possible move on results day. You are being asked to pay a fat fear premium for the same strip of hope.

The index tells the same story through its straddle. With NIFTY near 24,056 and the 24,050 strike, the at-the-money call is about Rs 426 a share and the put about Rs 295, so the at-the-money straddle is roughly Rs 720 a share. That straddle is the market's quick estimate of the expected move, about plus or minus 720 points by 28 July. Before a big event, that straddle widens, which is the index version of options getting expensive. The market is openly telling you it expects a bigger swing.

The straddle price is the market's own estimate of the event. If the at-the-money call plus put is fat, the market has already priced in a large move. To profit as a buyer, the real move has to beat that priced-in expectation, not merely point the right way.

After the event: the IV crush

Then the event happens. The numbers are out, the policy is announced, the result is known. The single biggest source of uncertainty, the not-knowing, vanishes in an instant. Implied volatility collapses back toward its normal level almost immediately, and because so much of the pre-event premium was pure fear, the premium falls hard the moment that fear drains away. This sudden collapse is the IV crush.

The crush is not a glitch and it is not unfair. It is the market correctly removing a risk premium that is no longer needed. The trouble is that beginners buy into the expensive, high-IV moment, drawn in by the excitement, and then hold straight through the crush.

| Stage | What the market is doing | Implied volatility | The premium |

|---|---|---|---|

| Days before the event | Pricing in a big unknown move | Expands, climbs higher | Swells, hope gets expensive |

| The moment the news lands | The uncertainty is resolved | Crushes, falls fast | Collapses toward intrinsic value |

| After the dust settles | Back to a normal expectation | Near its usual range | Reflects only the real move and the time left |

Right on direction, still in the red

Here is the cruel part, the one that makes traders distrust their own eyes. You can be correct about the direction and still lose money, because the crush takes back more than the move gives.

Walk through it with RELIANCE. Suppose results are due and the 1320 call has been bid up to about Rs 50 a share on swollen IV. You expect good numbers, you buy the call, and you are right. RELIANCE rises from 1318 to 1345 on the result. The call is now genuinely in-the-money by Rs 25 a share, which is real intrinsic value you did not have before. And yet the call might be trading at only about Rs 35 a share, because implied volatility has crushed and stripped out most of the time value that was sitting on top. You paid about Rs 50 and the option is worth about Rs 35. You were right on direction and you still lost about Rs 15 a share, which is about Rs 7,500 on one lot of 500.

That is the whole event trap in one example. The move was real, but it was smaller than the move already priced into the inflated premium. The crowd had already paid for a bigger jump than the one that actually arrived, and the crush handed that overpayment straight back to the seller.

Buying expensive premium just before a known event is one of the most reliable ways a beginner loses money while being right. You pay an inflated, high-IV price, the event passes, implied volatility crushes, and the premium falls even though the stock moved your way. The market had already priced the expected move into what you paid.

How sellers try to use the crush

If the crush punishes buyers, you might guess that sellers try to stand on the other side of it, and they do. A seller collects the fat, pre-event premium and aims to keep most of it as IV collapses afterward. Selling into rich, event-inflated volatility and buying back cheap once the fear has drained is one of the oldest plays in the book.

But this is not free money, and it must be said plainly. A naked seller who shorts an option into a binary event is exposed to the full move if the result surprises hard in the wrong direction. The crush only helps if the actual move stays within the range the market already priced. If RELIANCE gaps far beyond that range, the seller's loss from the move can dwarf the premium collected and dwarf the help from the crush. This is why careful traders harvest event premium through defined-risk structures, where a bought option caps the loss of the sold one, rather than selling naked. A naked short index option already blocks roughly Rs 1.5 lakh to Rs 1.8 lakh of margin per lot precisely because that risk is large, and an event makes it larger.

The crush rewards the seller only when the real move is smaller than the move priced in. When an event genuinely surprises the market, the seller can be run over before the crush ever helps. That is why event selling belongs in a defined-risk structure, not a naked short, and why it is not a beginner's first trade.

Trading around an event safely, or not at all

You do not have to trade every event. In fact the safest answer for most beginners is to sit on your hands through the noisiest ones. But if you do want to engage, a few habits keep you from walking into the crush.

- Know the calendar before you buy. Check whether results, an RBI policy, the Budget or an election fall before your expiry. An option whose life straddles a known event carries event risk whether you wanted it or not.

- Respect the priced-in move. If you must buy through an event, accept that you are paying inflated IV and that the real move has to beat the expected move to win, not just point the right way.

- Buy before the ramp, not at the peak. If you have a view, getting positioned while volatility is still calm is far cheaper than buying into the swollen premium the day before.

- Consider waiting for the crush. If your view survives the event, premium is cheaper and calmer afterward, once the fear has been wrung out. There is no rule that says you must be in beforehand.

- If you sell, define your risk. Never go naked into a binary event. Let a bought option cap the damage if the result surprises.

The deepest lesson of events is that the option market is not naive. When everyone expects a big move, that expectation is already sitting in the price you pay. The option only rewards a buyer if the real move is larger than the crowd already paid for, and most of the time it is not. Keep this rhythm in mind and you will stop treating earnings season and policy days as easy money, and start treating them as the high-cost, high-trap moments they really are. The next chapter gathers this and every other danger into one place: how beginners actually blow up, and the discipline that keeps you in the game.