Intrinsic Value and Time Value

An option's premium is built from two parts. Learn intrinsic value (the real, here-and-now worth) and time value (the hope premium that melts away as expiry nears).

- ·Intrinsic value defined

- ·Time value defined

- ·Premium = intrinsic + time

- ·Why OTM is all time value

- ·Time decay as expiry nears

- ·Why this matters for buyers

When you pay about Rs 31 a share for the RELIANCE 1320 call, you are not buying one thing. You are buying two things bundled into a single price tag. One part of that Rs 31 is hard, here-and-now worth that you could collect today. The other part is pure hope, a bet that the stock will move your way before the option dies on 28 July. Learning to see those two parts separately is one of the biggest jumps a new option trader can make, because it explains why an option can lose money even when the stock barely moves. This chapter pulls the premium apart into its two pieces and shows you why one of them is quietly working against you every single day.

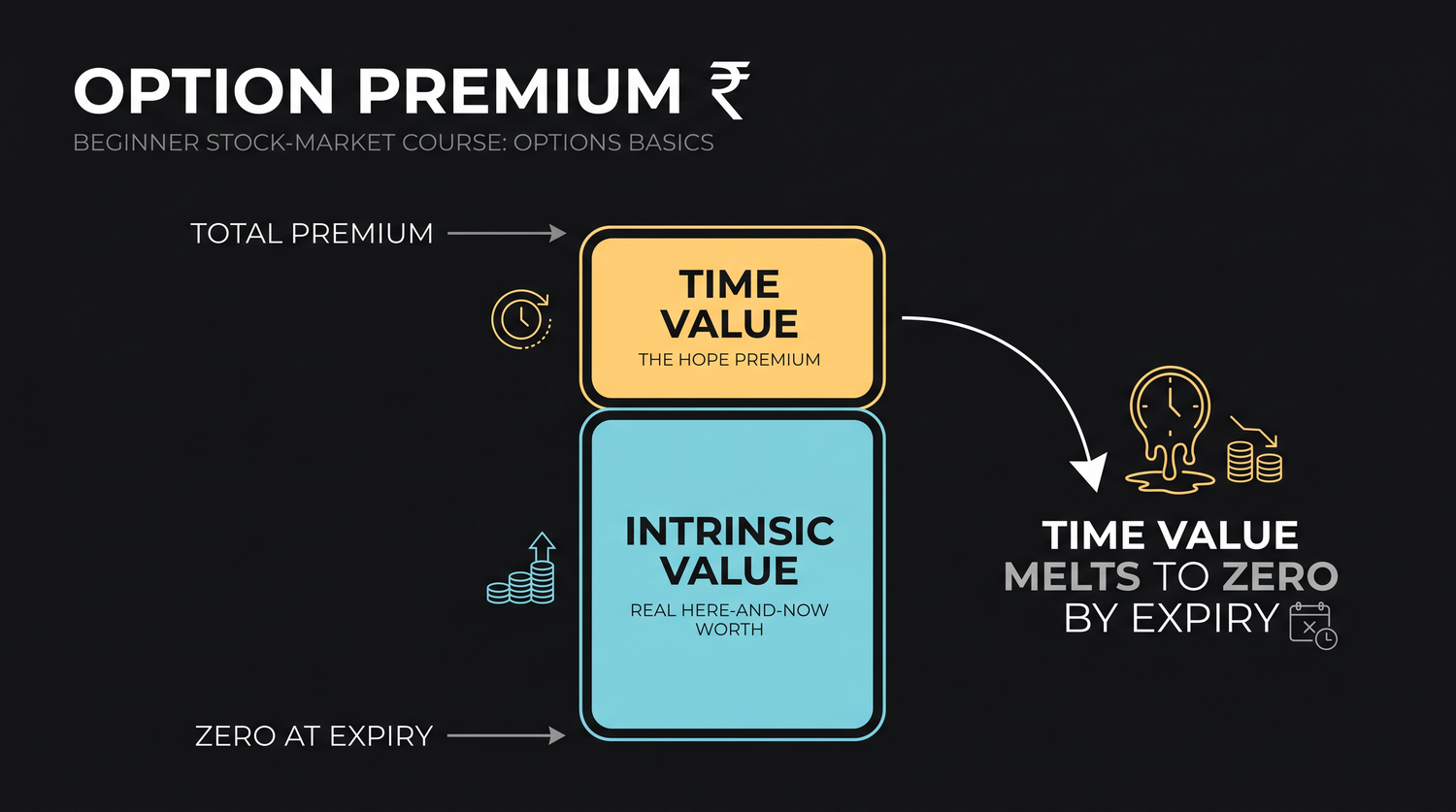

The premium is made of two parts

Every option premium splits cleanly into two components that always add up to the price you pay.

- Intrinsic value is the real, settle-now worth of the option. It is the money you would pocket if the option were settled this instant. For a call, intrinsic value is how far the spot price sits above the strike. For a put, it is how far the spot sits below the strike. Intrinsic value can never be negative, because an option that finishes against you is simply left to expire rather than settled at a loss. The worst it can be is zero.

- Time value is everything else. It is the part of the premium you pay purely for the chance that the stock moves further in your favour before expiry. Some people call it the hope premium, and that name is honest. Time value is the market charging you for time and possibility.

The relationship is simple. Premium equals intrinsic value plus time value. If you know any two of the three, you know the third.

Premium equals intrinsic value plus time value. Intrinsic value is what the option is worth right now if exercised. Time value is what you pay for the hope of more. They always add up to the full price.

A real RELIANCE split

Let us anchor this on the real numbers. RELIANCE closed near Rs 1,318 on 25 June 2026, the nearest strike is 1320, and the modelled at-the-money premium is about Rs 31 per share, which is about Rs 15,590 for one lot of 500.

Take the 1320 call first. The spot is 1318, the strike is 1320, so the spot sits below the strike. A call only has intrinsic value when the spot is above the strike, so here the intrinsic value is exactly zero. That means the whole Rs 31 you pay is time value. Every rupee of it is hope. You are paying purely for the chance that RELIANCE climbs above 1320, and then keeps going, before 28 July.

Now take the matching 1320 put. A put gains intrinsic value when the spot is below the strike. The spot is 1318 and the strike is 1320, so the put is in-the-money by 2 rupees. Its intrinsic value is Rs 2 a share. If that put also trades near Rs 31, then its time value is Rs 29 a share, because 31 minus 2 leaves 29. So the put premium is a small slice of real worth sitting under a thick layer of hope.

The 1320 call at spot 1318: intrinsic value Rs 0, time value Rs 31. It is all hope. The 1320 put at spot 1318: intrinsic value Rs 2, time value Rs 29. Almost all hope, with a thin floor of real worth underneath. Per lot of 500, that Rs 31 call is about Rs 15,590, every paisa of it time value.

This is the pattern for any option that is at-the-money or out-of-the-money. An out-of-the-money option has no intrinsic value at all, so its entire premium is time value. That is exactly why cheap, far-out options feel like lottery tickets. You are buying nothing but hope, and hope has an expiry date stamped on it.

Time decay: the melting top band

Here is the part that catches beginners by surprise. Intrinsic value is fixed by where the stock is right now. Time value is not. Time value melts away as expiry approaches, and on expiry day it reaches zero. This steady leak is called time decay, and traders also know it by the Greek name theta.

Think of time value as an ice block sitting on top of the intrinsic value. Every day that passes, a little more of it melts. With 32 days left to 28 July, the RELIANCE 1320 option still has a full block of time value, because there is plenty of time for the stock to move. As the days tick by and nothing dramatic happens, that block shrinks. The option still exists, the stock has barely moved, yet your premium quietly drains lower.

And the melt is not even. Time decay is slow at first and brutal at the end. In the early weeks the option loses time value gently. In the final week, and especially the final day or two, the remaining time value collapses fast, because there is almost no time left for a move to rescue it. An option that is out-of-the-money on the morning of expiry will see its last few rupees of time value evaporate to nothing by the close.

Time decay is the option buyer's quiet enemy. You can be right that RELIANCE will rise, buy the 1320 call, and still lose money if the rise is too small or arrives too slowly. The clock charges you rent every day, and it charges the most in the final days before expiry.

Why this is the buyer's enemy and the seller's friend

When you buy an option, you own the melting ice block. Time decay works against you. Each morning, all else equal, your option is worth a little less than it was the night before, simply because one more day has passed. To win, the stock must move enough, and soon enough, to outrun that daily leak. This is the single biggest reason most option buyers lose money. They are right about direction but wrong about size or speed, and time decay quietly eats the rest.

The person on the other side of your trade, the option seller, holds the opposite position. They received that time value upfront, and they get to keep more of it with every day that the stock fails to make a big move. For the seller, time decay is a tailwind. We cover selling properly in a later chapter, including its serious risks, but it helps to see the symmetry now. The time value you pay as a buyer is the time value a seller is trying to collect.

Before you buy any option, ask how much of the premium is real intrinsic value and how much is time value you will have to outrun. If it is all time value, you are buying pure hope, and the clock starts draining it immediately.

How the split shifts as RELIANCE moves

The two components are not frozen. They shift in real time as the stock moves and as days pass.

- If RELIANCE rises from 1318 to 1340, the 1320 call gains intrinsic value. It is now 20 rupees in-the-money, so at least Rs 20 of the premium is hard worth, with time value sitting on top.

- If RELIANCE falls to 1300, the 1320 call moves further out-of-the-money. Its intrinsic value stays zero, and only time value remains, now smaller because the move it needs got bigger.

- If RELIANCE simply sits at 1318 for two weeks, neither call nor put gains intrinsic value, yet both lose time value to the calendar. The premium shrinks even though nothing happened.

That last point is the one to burn into memory. An option can lose value while the stock goes nowhere. A share that closes flat for a month costs a long-term shareholder nothing. The same flat month can quietly destroy most of an option buyer's premium.

On expiry day, time value is gone and only intrinsic value remains. The 28 July payoff of any option is pure intrinsic value: how far it finished in-the-money, and nothing more. Everything you paid above that was time value, and the clock has now collected all of it.

So the premium you pay is two stories in one number. Intrinsic value is the calm, factual part, the worth the option has earned by where the stock actually is. Time value is the hopeful part, the rent you pay for the chance of more, and it is melting from the moment you buy. Keep these two apart in your head and the behaviour of every option you ever trade becomes far less mysterious. When we read real payoff diagrams in the next few chapters, you will see this split come alive as the curve bends around the strike.