How to Choose a Strike and an Expiry

Two decisions decide most of your outcome. Learn how to pick a strike (ITM, ATM or OTM, and the delta-based shortcut), why a far OTM option is a lottery ticket, and how to choose weekly versus monthly while respecting theta and events.

- ·ITM, ATM or OTM, which and why

- ·Delta as a strike guide

- ·The far-OTM lottery trap

- ·Weekly vs monthly expiry

- ·Near vs far expiry and theta

- ·Liquidity and event filters

Two decisions shape most of what happens to an option trade, and you make both of them before the stock has moved a single rupee. The first is which strike you buy. The second is which expiry you buy. You can read the direction right and still lose, because you picked a strike too far away to ever catch up, or an expiry too short to give your idea room to breathe. Get strike and expiry sensible and a modest, correct move can pay you handsomely. This chapter is about making those two choices on purpose, instead of by accident.

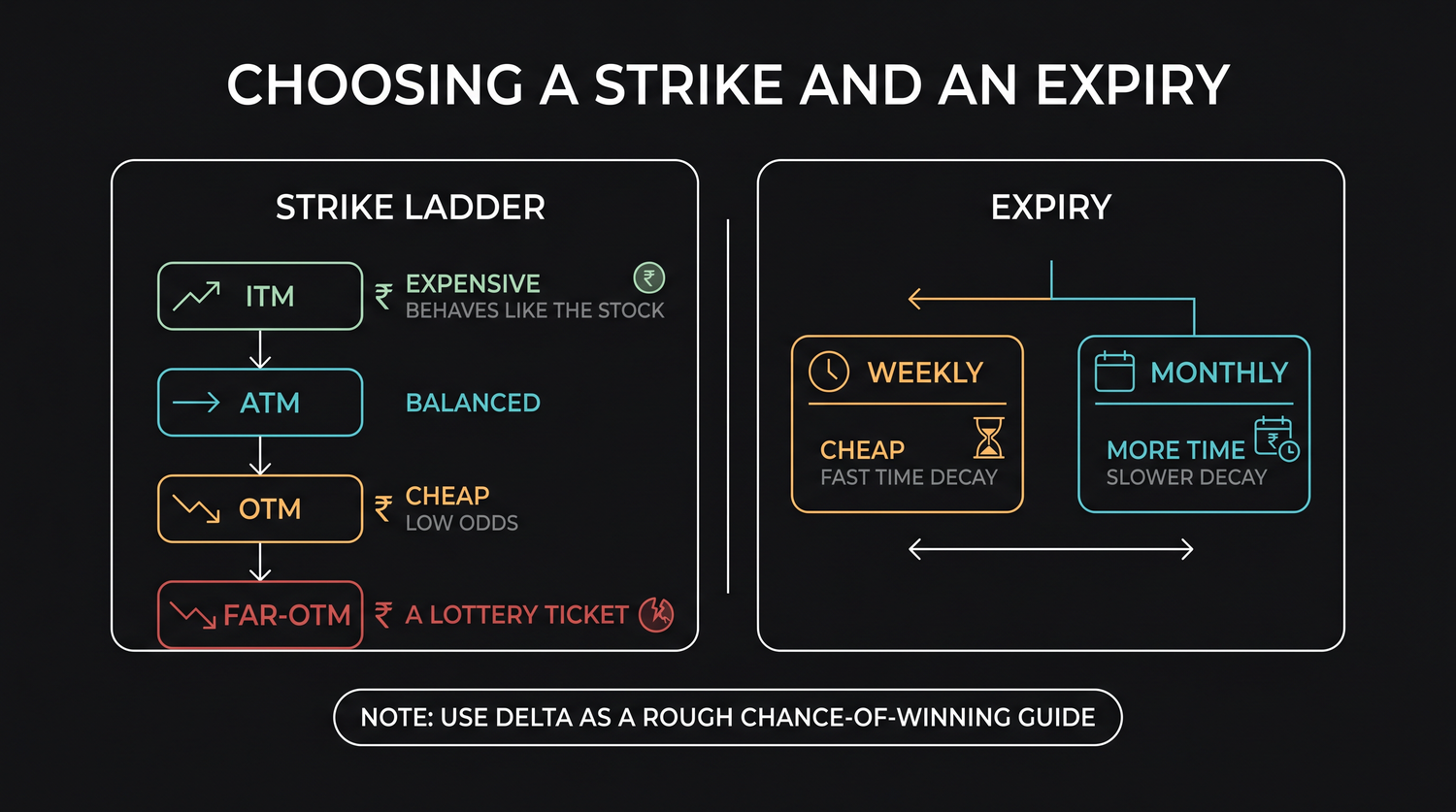

The strike decides your trade-off

When you buy a call on RELIANCE, with the stock near Rs 1,318 and the nearest strike at 1320, you are not stuck with that one strike. The option chain offers a whole ladder of strikes above and below. Where you stand on that ladder decides three things at once: how much you pay, how strongly the option tracks the stock, and how likely it is to be worth anything at expiry.

There are three broad zones to know.

- An in-the-money (ITM) call has a strike below the spot, so it already holds real, settle-now worth. It is the most expensive to buy, because you are paying for that built-in value plus a little time value. In return it behaves almost like the stock itself: when RELIANCE rises one rupee, a deep ITM call rises close to a rupee too. There is little hope premium to melt, so time decay bites it less.

- An at-the-money (ATM) call has a strike near the spot, here the 1320 call at about Rs 31 a share, which is about Rs 15,590 for one lot of 500. It is the balanced choice. Roughly half of any move flows into the premium, the time value is at its thickest, and the odds are close to even.

- An out-of-the-money (OTM) call has a strike above the spot. It is cheap, because it holds no intrinsic value at all, only hope. It moves lazily when the stock moves a little, and it needs a clear, committed move to pay off. The further out you go, the cheaper it gets and the longer the odds become.

A cheaper option is not a better option. The price falls as you move out-of-the-money precisely because the chance of it ever being worth something falls too. You are not getting a bargain, you are buying a longer shot.

Delta is your rough chance of finishing in-the-money

Here is a practical shortcut the chain hands you for free. Every option has a delta, a number between 0 and 1 for a call, that tells you roughly how much the premium moves for each one rupee move in the stock. A delta of 0.50 means the option gains about 50 paise when the stock gains a rupee. But delta carries a second, very useful reading: it is a rough guide to the chance the option finishes in-the-money at expiry.

An ATM option sits near a delta of 0.50, which is close to a coin flip. A deep ITM option with a delta near 0.80 is whispering that it has roughly an 80 percent feel of finishing in-the-money. A far-OTM option with a delta of 0.10 is telling you it has only about a one-in-ten chance of finishing with any value at all. The number is not a promise, and it shifts as the stock and the calendar move, but it is an honest gut-check on the odds you are taking.

| Strike (RELIANCE call) | Where it sits versus spot 1318 | Premium | Delta (rough) | Rough chance of finishing in-the-money | How it behaves |

|---|---|---|---|---|---|

| In-the-money | strike below the spot | most expensive | about 0.70 to 0.90 | high | tracks the stock almost rupee for rupee |

| At-the-money (1320) | strike near the spot | about Rs 31 a share | about 0.50 | roughly a coin flip | balanced, thickest time value |

| Out-of-the-money | strike above the spot | cheap | about 0.30 | below even | needs a clear move to pay off |

| Far out-of-the-money | strike far above the spot | very cheap | about 0.10 or less | low | a long shot, usually expires worthless |

Read the delta before you buy. If a strike shows a delta of 0.15, you are looking at something with roughly a one-in-seven chance of paying off. That can still be a deliberate bet, but make it knowing the odds, not because the premium happened to look small.

The far-OTM lottery trap

The cheapest options on the screen are the far-out-of-the-money ones, and they are the ones beginners reach for first, because a few rupees a share feels affordable and the dream is a ten-bagger. This is the single most common way new buyers bleed their capital away.

A far-OTM option is almost all time value sitting on a tiny delta. For it to pay, the stock has to make a big move, in your direction, and soon, all before time decay drains the little premium it holds. Most of the time none of that lines up, and the option quietly expires worthless. You were not investing, you were buying a lottery ticket, and like most lottery tickets it paid nothing. Buying ten of them does not improve the odds, it just buys you ten losing tickets.

Far-out-of-the-money options are lottery tickets. They are cheap because they usually expire worthless. Stringing together many small losses on long-shot strikes is how a lot of beginners lose everything, without ever taking one big, obvious hit.

Expiry: weekly versus monthly

The second decision is how much time you buy. Some underlyings offer a weekly expiry as well as the monthly one. NIFTY, for example, trades a weekly contract alongside the 28 July monthly, while RELIANCE trades monthly. The choice between them is really a choice about time decay.

A weekly option is cheap, because there is so little time left inside it. But that same shortness means its time value melts fast. Theta, the daily bleed of time value, is fierce in a weekly contract. A weekly buyer needs the move to happen quickly, within a day or two, or the premium drains away even when the eventual direction turns out right. Weeklies reward a precise, fast call and punish patience.

A monthly option costs more, because you are buying more time, but that time decays more gently in the early weeks. The 28 July RELIANCE option still carries a full block of time value with weeks to run, so a slow, correct move has room to work in your favour. You pay more for the privilege, but you are not racing a stopwatch from the first hour.

| Feature | Weekly option | Monthly option |

|---|---|---|

| Premium | cheaper | more expensive |

| Time left | days | weeks |

| Theta (daily decay) | fast and harsh | slower at first |

| Suits | a quick, precise move | a move with room to develop |

| Main risk | decays to nothing before the move arrives | costs more, ties up more premium |

Theta accelerates as expiry nears

Whichever expiry you pick, remember that time decay is not even across the life of the option. Time value melts slowly at first and then collapses in the final days. An option with a month to run loses only a little each session. The very same option in its last two or three days can shed its remaining time value almost overnight.

This gives a clean practical lesson. If your view needs two or three weeks to play out, buying a contract with only a week left means fighting the steepest part of the decay curve. Give a slow idea more time than you think it needs. And if you are holding a long option into its final days while the stock goes nowhere, understand that the floor is falling away under your premium faster with each passing session.

Theta is not constant. The last week of an option's life is where time value disappears fastest. Buying too little time, or holding on too long, both put you on the steep part of that curve.

Do not let an event ambush your expiry

Look at what falls inside your option's window before you buy it. Company results, an RBI policy meeting, the Union Budget, a major global central-bank decision, any of these can land between today and your expiry. Before such an event, implied volatility rises and premiums turn expensive. Right after it, that extra volatility drains out and the premium can collapse, even when the stock moved your way. This is the IV crush, which has a chapter of its own.

The lesson for choosing an expiry is simple. If you do not want to bet on an event, do not pick an expiry whose window straddles it while paying the inflated, pre-event premium. If betting on the event is the whole point, then go in with eyes open, knowing you are buying expensive volatility that will deflate the moment the news is out.

Liquidity is the filter over both choices

Finally, a filter that sits over both decisions. A strike or an expiry is only as good as your ability to get in and out of it at a fair price. Liquidity is how easily you can trade without the price moving against you. You read it in the gap between the bid and the ask, and in the volume and open interest at that strike.

The strikes near the money in a near-month, popular contract are usually liquid: tight bid-ask spreads, plenty of trades, easy exits. Wander far out-of-the-money, or into a thin far-month, and the spread widens, sometimes brutally. On an illiquid strike you can pay a wide spread just to enter, then pay another wide spread to leave, and that round-trip cost can quietly swallow whatever edge your view had. A strike that looks perfect on the payoff diagram is useless if you cannot trade it at a sensible price.

Before you commit to a strike and an expiry, check that it actually trades: a tight bid-ask spread and healthy volume and open interest. The cleanest view in the world still loses money on a strike you cannot get out of.

Put the two decisions together and a clear habit emerges. Choose a strike whose delta matches both how confident you are and how far you genuinely expect the stock to travel. Choose an expiry that gives your idea enough time without paying for time you will never use, and that does not accidentally straddle an event you did not mean to bet on. Then check that both are liquid enough to trade cleanly. Do that consistently and you have removed two of the biggest, most avoidable reasons beginners lose on options, long before the market has had any say in the matter.