In, At and Out of the Money

ITM, ATM, OTM are the labels you will see everywhere. Learn what in-the-money, at-the-money and out-of-the-money mean for calls and puts, with a clear picture.

- ·At-the-money (ATM)

- ·In-the-money (ITM)

- ·Out-of-the-money (OTM)

- ·Moneyness for calls vs puts

- ·Why OTM options are cheap

- ·How moneyness changes with price

Open any option chain and you will see the same strike described in three different moods. Some options are already worth using right now. Some sit balanced exactly at the current price. And some are pure hope, worth nothing today but cheap enough to dream on. These three moods have names, in the money, at the money and out of the money, and together they are called moneyness. Moneyness is the first thing experienced traders read about an option, because it tells you instantly whether a strike is a real, here-and-now deal or just a bet on the future. Once you can sort any option into these three buckets, the option chain stops being a wall of numbers and starts telling a story.

The three buckets

Moneyness compares the strike against where the underlying is trading right now. With RELIANCE at Rs 1,318, the strike of 1320 is our reference point, and every other strike is judged against the current price.

- At-the-money, or ATM, is an option whose strike sits right at, or very close to, the current price. With RELIANCE at 1,318, the 1320 strike is the at-the-money strike. It is balanced on the knife edge, not yet worth using but ready to tip either way.

- In-the-money, or ITM, is an option that already has real, settle-now worth. If it were settled this instant, you would gain. That built-in worth has a name, intrinsic value, the part of the premium that reflects a deal already worth doing.

- Out-of-the-money, or OTM, is an option with no intrinsic value at all. Settling it now would gain you nothing, so its entire premium is hope that the stock moves before expiry. OTM options are the cheap lottery tickets of the market.

The whole idea rests on intrinsic value, the real here-and-now worth. An in-the-money option has some. An out-of-the-money option has none. An at-the-money option sits right on the boundary with essentially none.

Moneyness sorts options by their real worth right now. In-the-money has intrinsic value you could cash today. Out-of-the-money has none and is all hope. At-the-money sits on the line between them.

Moneyness is mirror-image for calls and puts

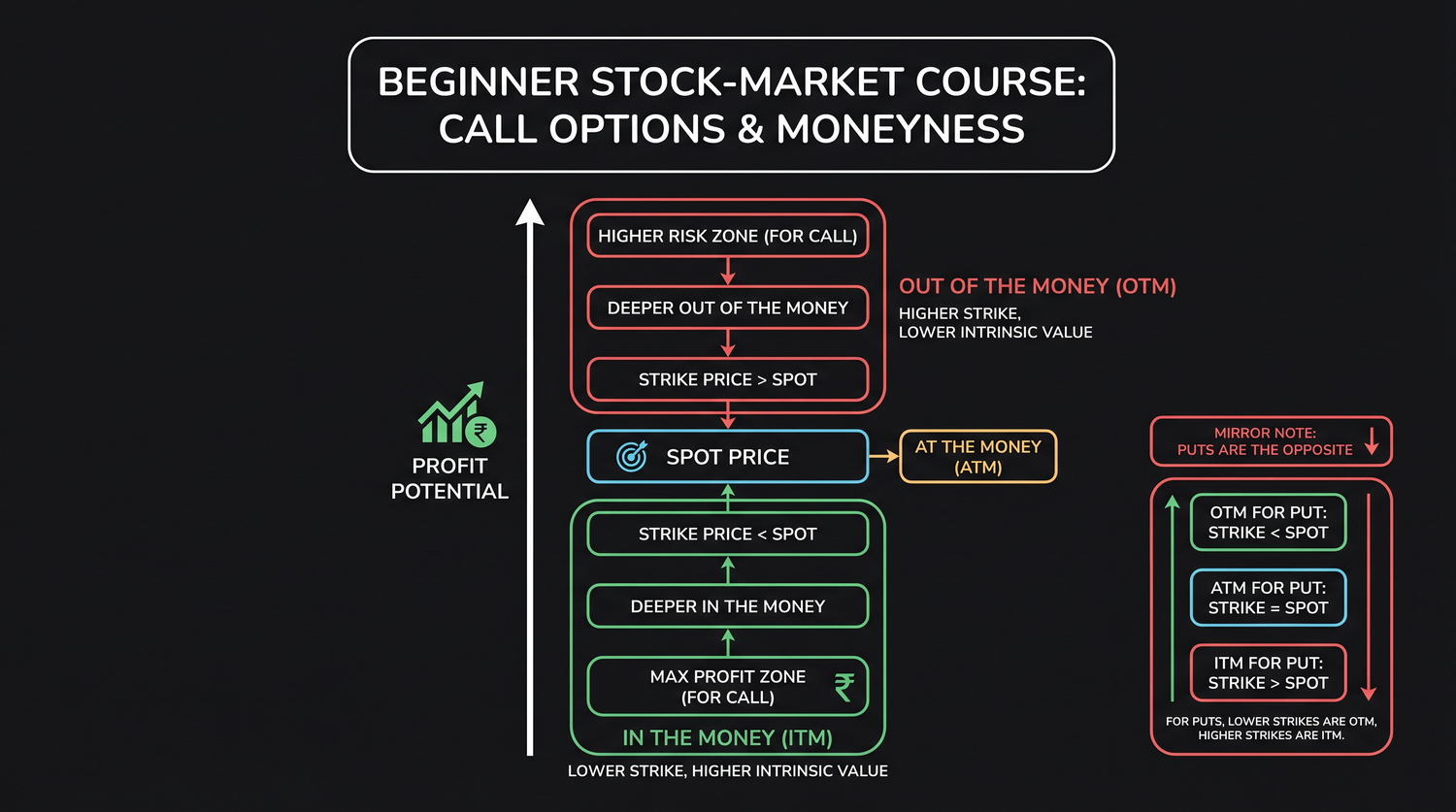

Here is the part that confuses beginners, so take it slowly. Whether a strike is in or out of the money depends on whether you are holding a call or a put. The two are mirror images, because a call profits when the price rises and a put profits when the price falls.

For a call, the right to buy at the strike:

- The call is in-the-money when the strike is below the current price. Your right to buy cheap is already worth something. A 1300 call with RELIANCE at 1,318 lets you buy 18 rupees below the market.

- The call is out-of-the-money when the strike is above the current price. Your right to buy at 1340 is useless while the stock sits at 1,318, because the open market is cheaper.

For a put, the right to sell at the strike, flip every direction:

- The put is in-the-money when the strike is above the current price. Your right to sell high is already worth something. A 1340 put with RELIANCE at 1,318 lets you sell 22 rupees above the market.

- The put is out-of-the-money when the strike is below the current price. Your right to sell at 1300 is useless while the stock sits at 1,318, because the open market pays more.

The trick to remember it: a call wants the strike low so it can buy cheap, a put wants the strike high so it can sell dear. In-the-money always means the strike gives you a better deal than the market does right now.

Whenever you get lost, ask one question: if I exercised this option this second, would I gain? If yes, it is in-the-money. If no, it is out-of-the-money. That single test works for both calls and puts every time.

A moneyness table around 1320

Let us lay it out concretely. RELIANCE is at 1,318, and here is a ladder of strikes with the moneyness of the call and the put at each one. Read across each row and watch the mirror.

| Strike | Call moneyness | Put moneyness |

|---|---|---|

| 1260 | In-the-money | Out-of-the-money |

| 1300 | In-the-money | Out-of-the-money |

| 1320 | At-the-money | At-the-money |

| 1340 | Out-of-the-money | In-the-money |

| 1380 | Out-of-the-money | In-the-money |

Notice the clean symmetry. Below the current price, calls are in-the-money and puts are out-of-the-money. Above it, the roles swap. And the 1320 strike, sitting right next to the 1,318 price, is at-the-money for both. The same ladder reads in opposite directions depending on which side, call or put, you hold.

Take the 1300 call with RELIANCE at 1,318. Exercising it means buying at 1300 when the market is 1,318, an instant worth of 18 rupees a share. That 18 rupees is its intrinsic value, so the call is in-the-money. The matching 1300 put would let you sell at 1300 into a 1,318 market, which is pointless, so the put is out-of-the-money with zero intrinsic value.

Why out-of-the-money options are so cheap

Beginners are often drawn to out-of-the-money options for one reason: they are cheap. A far out-of-the-money RELIANCE call might cost only a few rupees a share. The temptation is obvious. Small outlay, and if the stock makes a big move, the percentage gain can be huge.

But understand what you are buying. An out-of-the-money option has no intrinsic value. Its entire premium is hope, the market's price on the chance that the stock travels far enough before expiry to make the strike useful. There is nothing solid underneath it.

That hope is fragile in two ways.

- The stock must move far enough to reach and pass the strike, and then keep going to beat the premium you paid, before the option pays a single rupee.

- The clock is running. The hope a premium contains, called time-value, melts away as expiry nears, and it melts fastest in the final days. An out-of-the-money option that never reaches its strike simply bleeds to zero and expires worthless.

This is exactly why most out-of-the-money buyers lose. They pay for hope, the stock fails to travel far enough in time, and the premium they paid quietly drains away. Cheap is not the same as good value. We give time-value and this slow bleed their own chapter next, because it is the single most important force working against an option buyer.

The cheapness of out-of-the-money options is the trap, not the bargain. You are buying pure hope with a deadline. Most far out-of-the-money options expire worthless, and the buyers who chase them lose steadily. Be honest with yourself about how far the stock really has to move, and how soon.

How moneyness shifts as the stock moves

Moneyness is not a permanent label. It changes the moment the underlying moves, because the strike is fixed while the current price is not. Watch what happens to our 1320 strike as RELIANCE wanders.

- RELIANCE is at 1,318. The 1320 call and put are both at-the-money, balanced right at the strike.

- RELIANCE rises to 1,360. Now the 1320 call is in-the-money, because the right to buy at 1320 is worth 40 rupees against a 1,360 market. The 1320 put has slipped out-of-the-money.

- RELIANCE falls to 1,280. Now the 1320 put is in-the-money, worth 40 rupees against a 1,280 market, while the 1320 call has gone out-of-the-money.

So an option you bought at-the-money can drift into the money as the stock moves your way, gaining real intrinsic worth, or drift out of the money as it moves against you, becoming pure hope again. Watching a position cross from out-of-the-money into in-the-money, picking up intrinsic value as it goes, is exactly what a winning option buyer is hoping to see before 28 July arrives.

At the exact moment of expiry, only intrinsic value survives. Every in-the-money option settles for its intrinsic worth, and every out-of-the-money option expires at zero. All the hope priced into time-value has run out, so on expiry day moneyness is the whole story.

What to carry forward

You can now place any option into its bucket and know what that bucket means.

- In-the-money options have real intrinsic value you could cash today. Calls are in-the-money below the current price; puts are in-the-money above it.

- At-the-money options sit right at the current price, the 1320 strike with RELIANCE at 1,318, balanced on the edge.

- Out-of-the-money options have no intrinsic value. They are all hope, cheap for a reason, and most of them expire worthless.

- Moneyness is a mirror image for calls and puts, and it shifts as the stock moves, since the strike is fixed and the price is not.

The natural next question is what makes up a premium. We have hinted at the answer twice now: intrinsic value, the real worth, plus time-value, the hope. The next chapter splits every premium into those two parts and shows you the slow, steady bleed of time-value that is the option buyer's quiet enemy.