Margin for Sellers, and Transaction Costs

Selling options is not free money. Learn why a seller must post a large SPAN plus exposure margin, how a hedge reduces it, and the full stack of charges, brokerage, STT, exchange fees, GST and stamp duty, that move your real breakeven.

- ·Why selling needs large margin

- ·SPAN and exposure in plain words

- ·How a hedge cuts the margin

- ·Pledging collateral, a caveat

- ·Brokerage, STT and the charges

- ·Your true cost-adjusted breakeven

Sell an option and the premium lands in your account the moment the trade fills. It can feel like free money: you did nothing, the stock has not moved, and there is cash sitting there. That feeling is the most expensive illusion in options. Selling is not free money, for two hard reasons. First, the exchange makes you post a large margin against the risk you have just taken on, because that risk can be far bigger than the premium you collected. Second, every trade, whether you buy or sell, drags a stack of charges behind it that quietly reshapes your real breakeven. This chapter walks through both, so the number on your screen is not the number that fools you.

Selling is not free money: the margin

When you sell, or write, an option, you take on an obligation. A naked short call carries unlimited risk above the strike. A naked short put carries very large risk as the stock falls. The exchange knows this, so before it lets you sell, it blocks a chunk of your capital as margin, a security deposit it holds against the chance the trade goes against you.

For one naked short index option, that margin runs to roughly Rs 1.5 lakh to Rs 1.8 lakh per lot. It is built from two pieces. SPAN margin is the exchange's risk-based core requirement, calculated from how much the position could lose under a range of moves. On top of that sits an exposure margin, an extra buffer. Together they are deliberately large, because the risk being covered is large. That premium you collected, often a few thousand rupees on one lot, is sitting against a margin block many times its size. Seen properly, selling is not free money, it is renting out a large amount of capital to carry a real and sometimes unlimited risk.

The premium a seller collects is small next to the margin blocked and the risk carried. A naked short call has unlimited loss above the strike, a naked short put very large loss as price falls. The margin is big because the danger is real. Respect it, or it will eventually find you.

A hedge cuts the margin sharply

There is a disciplined way to bring that margin down, and it is the same move that brings your risk down. If you buy a further option against the one you sold, you cap your worst case. The exchange can see that your loss is now bounded, so it recognises the smaller risk and the margin falls sharply, often to a small fraction of the naked figure.

This is the idea behind a defined-risk position: the bought option acts as a backstop on the sold one, so a runaway move can only hurt you so much. We do not build named strategies here, that is the job of the strategies course, but the principle matters now. A hedge is not only safer, it is far cheaper to hold, because the margin shrinks once your maximum loss is fixed and known.

Collateral can be pledged, with a caveat

You do not always have to post that margin in cash. You can pledge holdings you already own, shares or certain funds, as collateral, and the exchange counts their value toward your margin. For someone holding a portfolio, this lets the same capital do two jobs at once.

But read the caveat carefully. Pledged collateral comes with a haircut: you receive less than the full market value as usable margin, because the collateral itself can fall in price. The exchange also insists that a portion of your total margin, commonly around half, be held as actual cash, not just pledged shares. And crucially, pledged collateral does not pay your day-to-day losses. If the position moves against you, the resulting mark-to-market loss must be settled in real cash. A seller who pledged shares and kept no cash buffer can be forced to sell at the worst possible moment, or face a penalty, simply because the losing position demanded cash the collateral could not supply.

Pledging collateral frees up capital, but it is not a free pass. There is a haircut on the value, a part of the margin must still be cash, and running losses are settled in cash regardless. Keep a cash buffer, not just pledged shares.

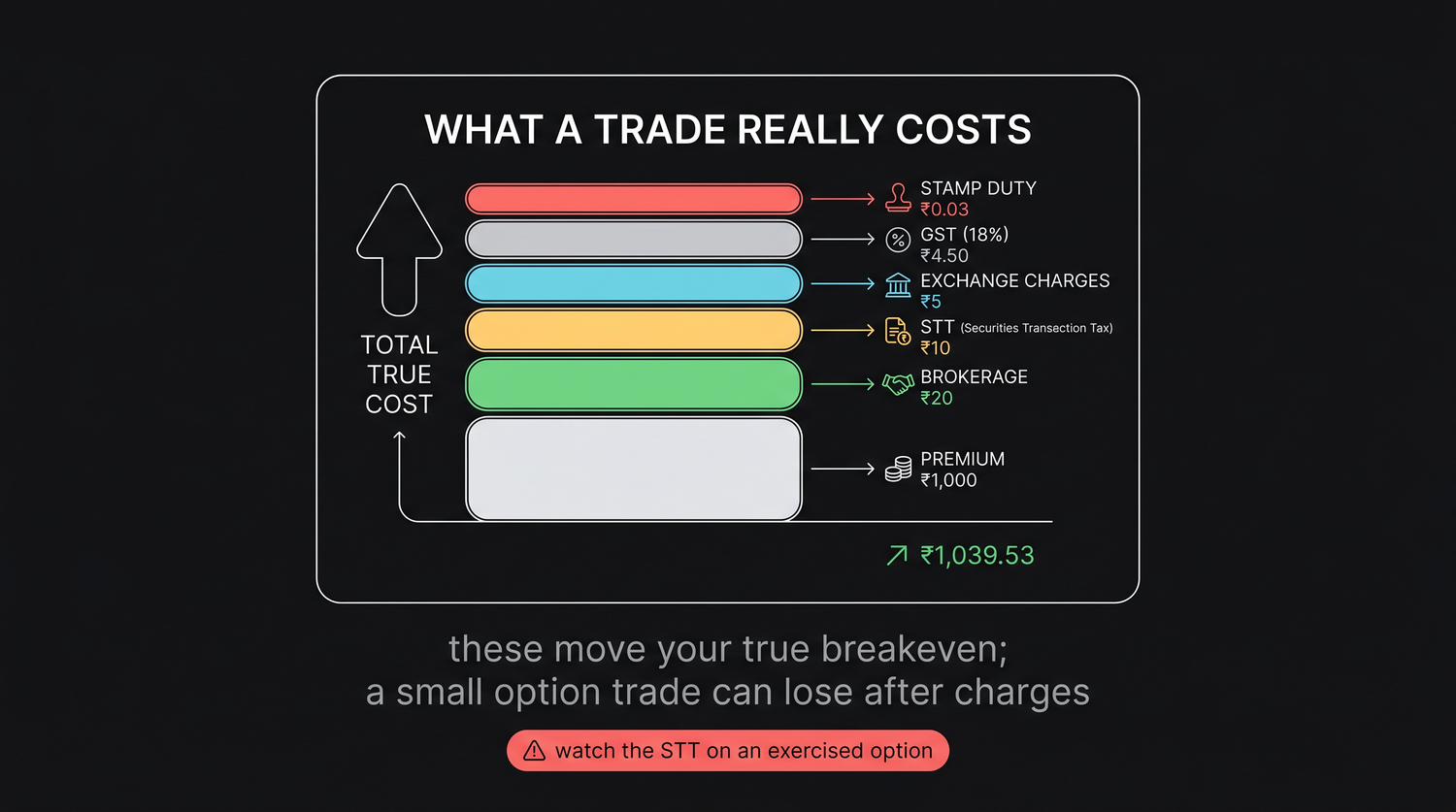

The full charges stack

Now the second reality, the one that touches every trade you ever place, buyer or seller. The premium is never the whole story. A stack of charges rides on top of, or out of, each trade, and they decide your true profit. Here is the stack for an options trade in India, with the rates that took effect on 1 April 2026 noted where they are fixed.

| Charge | When it applies | Rough basis |

|---|---|---|

| Brokerage | on every order, buy and sell | a flat fee per executed order, commonly around Rs 20, and nil at some brokers |

| STT on selling an option | when you sell or write the option | 0.15% of the premium value |

| STT on an exercised option | when an in-the-money option is exercised at expiry | 0.15% of the intrinsic (settlement) value |

| Exchange transaction charges | on every order, both sides | a small percentage of the premium turnover |

| SEBI charges | on every order, both sides | a tiny percentage of turnover |

| GST | on every order, both sides | 18% on (brokerage plus transaction charges) |

| Stamp duty | on the buy side only | a small percentage of the buy value |

None of these is large on its own. Stacked together, on a small trade, they add up to a real number, and that number comes straight out of your result.

The premium you pay or collect is not your cost or your income. Brokerage, STT, exchange and SEBI charges, 18% GST and stamp duty all sit on top. Your true profit is the premium move minus the whole stack.

How charges move your true breakeven

Think back to the RELIANCE 1320 call at about Rs 31 a share. At expiry its breakeven is the strike plus the premium, 1320 plus 31, which is 1351: the stock has to clear 1351 just to repay the premium. Add the charges and your real breakeven sits a little above 1351, because the stock must also cover what you hand over in costs. On a long, large move that extra slice is trivial. On a quick scalp it can be the whole game.

Picture a tiny round trip. You buy one lot of the 1320 call at about Rs 31 a share, costing about Rs 15,590, and it ticks up so you sell at Rs 31.50. On the premium alone that 50 paise gain is 0.50 times 500, which is Rs 250 of gross profit. Now stack the charges: a flat brokerage on the buy order and again on the sell order; STT on the sell side at 0.15% of the sell value, 31.50 times 500 is Rs 15,750, so about Rs 24; exchange and SEBI charges on roughly Rs 31,000 of two-way turnover, a few rupees; 18% GST on the brokerage plus those transaction charges; and stamp duty on the buy. Together these can come to roughly Rs 80 to Rs 100. Your Rs 250 gross is suddenly nearer Rs 150 net.

Now make the move thinner. Say you sell at Rs 31.10, a 10 paise gain. On premium that is 0.10 times 500, which is Rs 50 of gross profit, and the screen flashes green. But the same charge stack of roughly Rs 80 to Rs 100 is still there. The trade that looked profitable on the premium is a net loss once the costs are paid. This is the trap of the small scalp: the premium says you won, the charges say you lost, and only the second one is real.

A small option trade can show a profit on the premium and still lose after charges. The thinner the move you are trying to scalp, the more the fixed stack of costs matters. Always judge a trade by the net, never by the premium alone.

The STT-on-exercise trap

One charge in that table deserves its own warning, because it ambushes beginners on expiry day. Notice the two different STT lines. When you sell an option in the market, STT is 0.15% of the premium. But when you let an in-the-money option run to expiry and it is auto-exercised, STT is 0.15% of the intrinsic (settlement) value, the full in-the-money amount, not the small premium you originally paid.

For a deep in-the-money option, that settlement value can be large, so the STT is sized off the big number. Say a NIFTY call finishes Rs 300 a share in-the-money, on a lot of 65. The intrinsic settlement value is 300 times 65, which is Rs 19,500, and the exercise STT at 0.15% is about Rs 29, charged on that whole in-the-money value. A beginner who thought their only cost was the cheap premium they paid weeks ago is now billed off the full settlement. The deeper in-the-money the option, the bigger that base, and the bigger the surprise.

The defence is the same rule expiry mechanics already taught. Square off an in-the-money option in the market before the close on expiry day, rather than letting it be auto-exercised, unless you specifically want to take the settlement. Selling it pays STT on the premium and sidesteps the exercise charge entirely, and for a single-stock option it also avoids being pulled into physical delivery worth several lakh on one lot.

Do not let an in-the-money option drift into auto-exercise by accident. Exercise STT is charged on the full intrinsic value, a far bigger base than the premium. Squaring off before expiry keeps the tax on the premium and keeps you clear of delivery.

Put both halves together and the honest picture is clear. Selling premium is not free income, it is a margin-heavy position carrying real and sometimes unlimited risk, eased only when you hedge it into a defined-risk shape. And every trade, on either side, pays a stack of charges that shifts your breakeven and can turn a thin premium gain into an actual loss. Knowing your margin before you sell, and your full cost before you judge a profit, is not paperwork. It is the difference between a trade that looked good and a trade that was good.