Selling Options (Short Call and Put)

The other side of the trade: collecting the premium. Learn the short call and short put payoffs, the capped profit, the large or unlimited risk, and why sellers must respect that risk.

- ·Selling to collect premium

- ·Short call: unlimited risk

- ·Short put: large risk

- ·Capped profit (the premium)

- ·Margin for sellers

- ·Reading the real payoffs

So far you have always been the buyer, paying a premium for a right. But every option that is bought is sold by someone else, and that someone collects the premium you hand over. This chapter takes you to the other side of the table, where you become the option seller, also called the writer. Instead of paying the premium, you receive it upfront. Instead of holding a right, you take on a duty. It can feel like easy money, and that is exactly the danger, because the seller's reward is capped while the seller's risk can be enormous. We will read both short payoffs on the real RELIANCE numbers, and we will be blunt about the risk, because selling options without respecting it is one of the fastest ways a beginner can blow up an account.

Flipping the trade around

When you sell an option, you collect the premium today and accept an obligation in return.

- Selling a call means you receive the premium and take on the duty to deliver, or to settle, as if you had to sell RELIANCE at the strike if the buyer exercises. You want the stock to stay below the strike so the call expires worthless and you keep the premium.

- Selling a put means you receive the premium and take on the duty to buy, or to settle, as if you had to buy RELIANCE at the strike if the buyer exercises. You want the stock to stay above the strike so the put expires worthless and you keep the premium.

In both cases your best outcome is the same: the option expires worthless, the buyer walks away, and you keep every paisa of the premium you collected. For the RELIANCE 1320 strike, that premium is about Rs 31 per share, or about Rs 15,590 for one lot of 500. That figure, the premium received, is the most you can ever make on the trade. Your profit is capped on day one.

Selling an option flips the deal. You collect the premium upfront, and that premium is the maximum you can make. In return you accept an obligation, and that obligation is where the large risk lives. Capped reward, uncapped or very large risk.

Reading the short call payoff

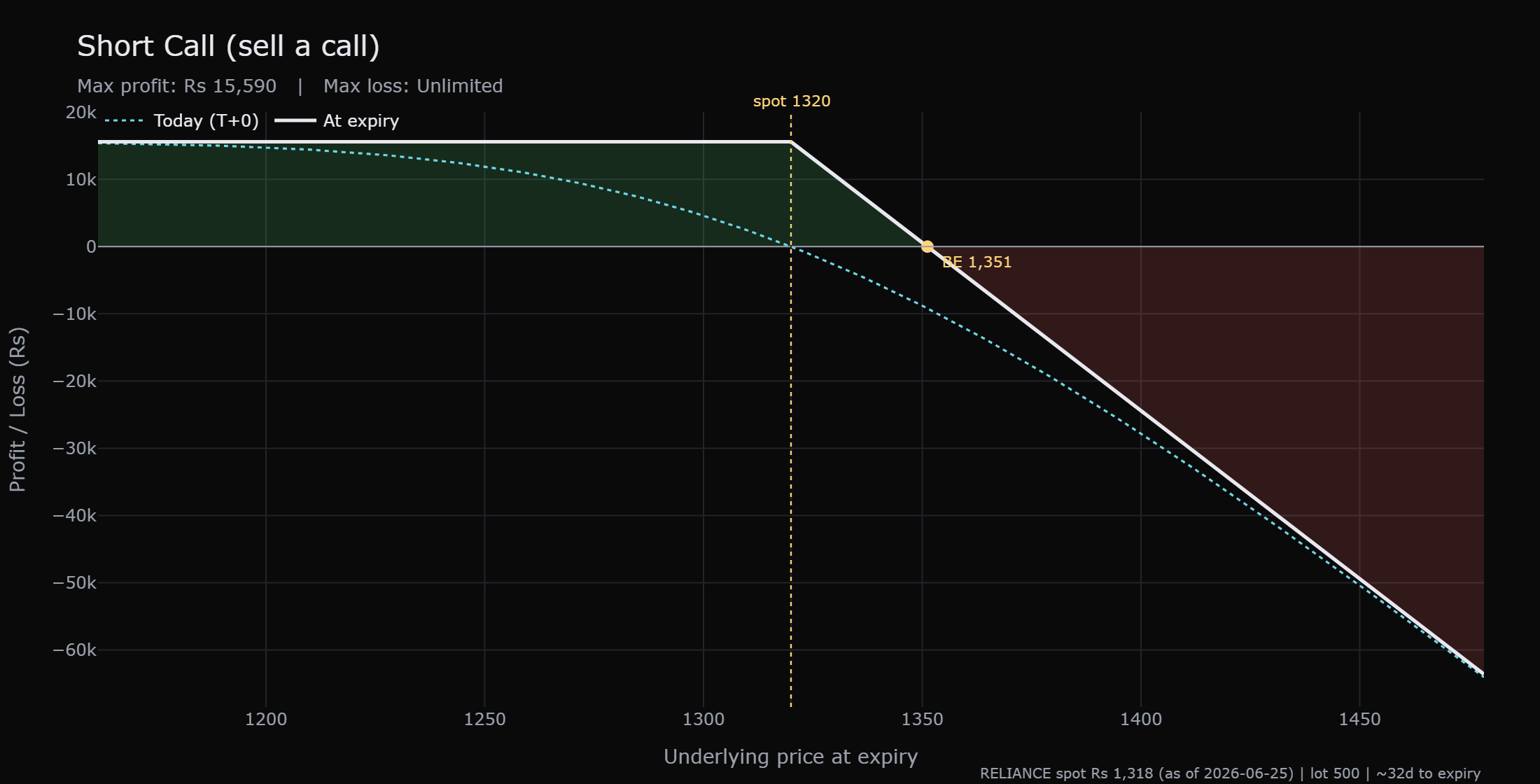

Here is the genuine payoff for selling the RELIANCE 1320 call, from OpenAlgo's strategy maths at spot Rs 1,318, strike 1320, lot 500, about 32 days out, premium near Rs 31. The solid line is the value at expiry; the dotted cyan line is the value today. Notice it is the long call payoff from an earlier chapter flipped upside down, which makes sense, because the seller wins exactly what the buyer loses.

On the left, the line is flat at a profit. For any expiry price below the strike of 1320, the call you sold expires worthless. You keep the full premium, about Rs 15,590, and that is your maximum gain. Whether RELIANCE ends at 1300 or 1100, you make the same Rs 15,590, no more.

Through the middle, your profit erodes. Above 1320 the call you sold starts to have value, value the buyer can claim from you. You still keep part of the premium until the breakeven at 1351, which is the strike of 1320 plus the Rs 31 premium per share. At 1351 the loss you owe the buyer exactly cancels the premium you collected.

On the right, the line falls with no floor. Above 1351 you are in real loss, and every further rupee RELIANCE rises costs you Rs 500, because the position is on 500 shares. If RELIANCE finishes at 1400 you lose roughly Rs 24,500. At 1450, far more. There is no level at which the loss stops growing, because there is no ceiling on how high a stock can go. This is the unlimited loss of a naked short call, and it is the single most dangerous payoff a beginner can stumble into.

A short call carries unlimited loss. If RELIANCE gaps up on news, the call you sold can cost you far more than the Rs 15,590 you collected, with no upper limit. A single sharp rally can wipe out the premiums from many winning months. Never sell a call casually thinking the premium is yours to keep.

Reading the short put payoff

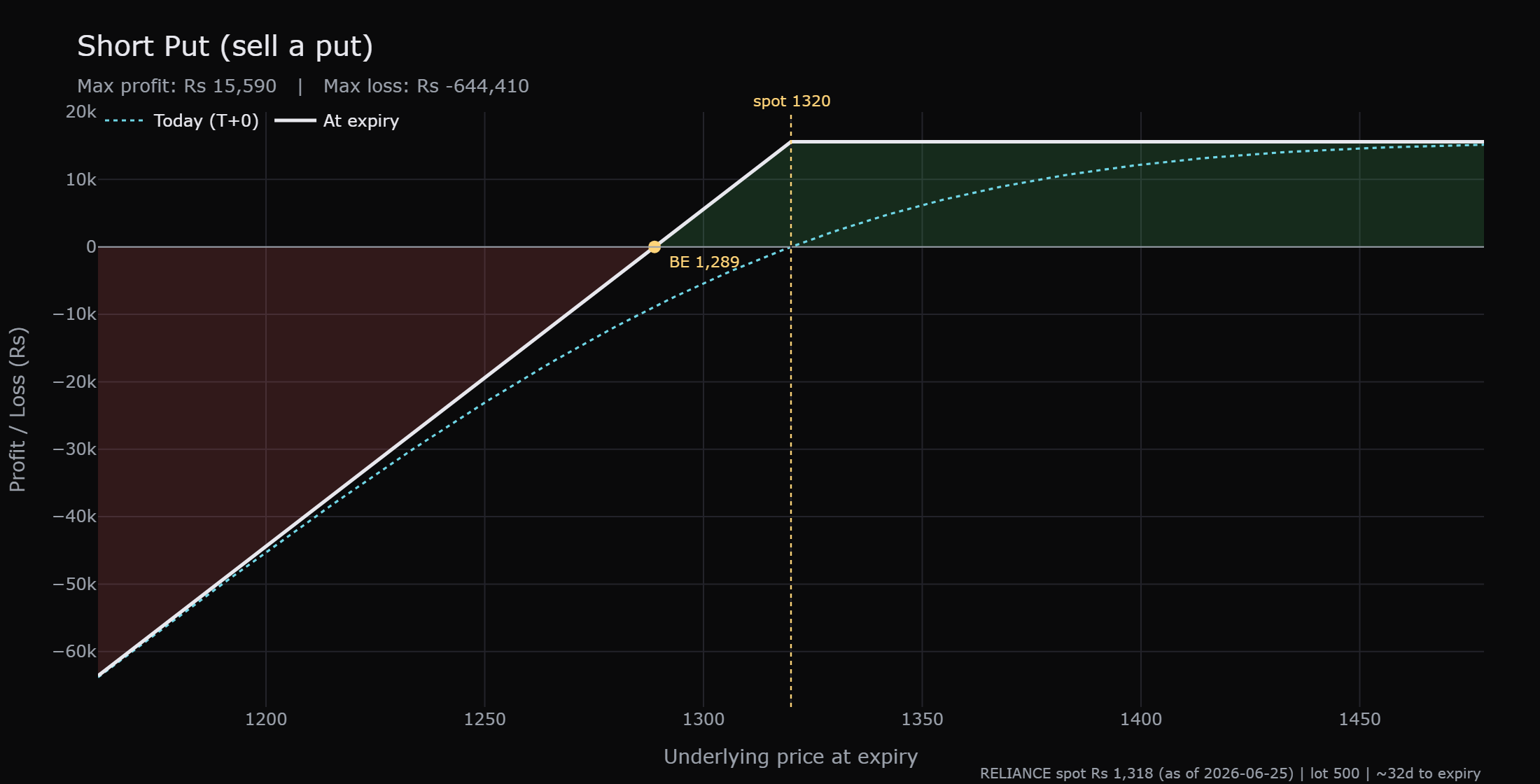

Now the short put, again the real RELIANCE numbers, the long put payoff turned upside down. You sold the 1320 put and collected about Rs 31 a share, hoping RELIANCE stays above the strike.

On the right, the line is flat at a profit. For any expiry price above the strike of 1320, the put you sold expires worthless and you keep the full premium, about Rs 15,590. That is your maximum gain, the same cap as before.

Through the middle, your profit erodes until the breakeven at 1289, the strike of 1320 minus the Rs 31 premium per share. Below 1289 you are in real loss.

On the left, the line falls into very large loss as RELIANCE drops. Every rupee below the strike costs you Rs 500. The loss is not literally unlimited, because a share cannot fall below zero, but the worst case is enormous. If RELIANCE collapsed all the way toward zero, the loss on that single short put would reach about Rs 6,44,000, against the Rs 15,590 you collected. You took on the duty to buy 500 shares at 1320 even if they become nearly worthless, and that duty is what you are paid the small premium to accept.

A short put carries very large risk. To collect Rs 15,590 you accept the obligation to buy 500 RELIANCE shares at 1320 even if the stock crashes. In the worst case that loss runs to roughly Rs 6,44,000. The premium is small; the risk behind it is not.

Why sellers must post margin

Because the seller's risk is so large, you cannot sell an option for free the way a buyer simply pays a premium. The exchange demands a deposit called margin, money blocked in your account as security against the loss you might owe. Selling one RELIANCE option lot ties up a substantial sum, far more than the Rs 15,590 you receive, and that margin can rise if the position moves against you, forcing you to add more or close out.

This margin requirement is not red tape. It is the system's honest acknowledgement that the seller can lose far more than they collect. A buyer pays a premium and that is the end of their commitment. A seller receives a premium but must post margin and keep it funded, because the obligation can grow, and the size of that margin is a rough mirror of the size of the risk you are taking on. If the margin feels uncomfortably large for the small premium on offer, that discomfort is telling you something true about the trade.

You can see the exact number before you commit. The exchange sets the seller's margin as a SPAN component, which covers a worst-case one-day move, plus an exposure buffer on top, and OpenAlgo includes a margin calculator that returns both parts and their total for any contract and quantity. Run it before writing an option so the blocked amount, and the risk it reflects, are never a surprise.

This is not free income

Selling options is often dressed up as a way to earn steady income, and it is true that most options expire worthless, so a seller wins more often than they lose. That is exactly what makes it seductive and exactly why beginners get hurt. You can collect Rs 15,590 month after month and feel like a genius, and then one violent move can hand back many months of premium in a single afternoon. The wins are small and frequent; the losses are rare and large. Respecting that shape is the whole craft of selling.

The trap in numbers. Sell the 1320 call and pocket Rs 15,590. Do it for six calm months and collect about Rs 93,540. Then RELIANCE gaps to 1450 on news and the short call costs you around Rs 49,500 in one go, erasing more than three months of premium. Frequent small wins, occasional large losses. This is why selling demands respect, not casualness.

If you do explore selling, do it with eyes open. Sellers who survive tend to define their risk in advance, often by holding the underlying shares behind a call or by pairing the short option with a bought option that caps the loss, structures you will meet in the next course. They size positions small, they keep cash for margin, and they never treat the premium as money already earned. And they rehearse first in sandbox trading (analyzer mode in OpenAlgo), watching how a short position behaves when the stock moves the wrong way, before risking real capital.

If you ever sell an option, decide your exit before you enter. Know the price at which the loss becomes unacceptable and act on it without arguing with the market. The seller's enemy is not the small, frequent loss; it is the one large move they refused to respect.

So selling is the mirror of buying in every way. The seller's reward is the premium, capped at about Rs 15,590, while the buyer's reward was open-ended. The seller's risk is unlimited on a short call and very large on a short put, while the buyer's risk was capped. Neither side is free money. The buyer pays the odds for a big payoff; the seller takes the odds for a small one and carries the heavy tail. In the next chapter we put the two sides face to face and ask the honest question every options trader must answer for themselves: buyer or seller, who really has the edge?