The Right, Not the Obligation

The single idea that makes options special: the buyer can walk away. Learn why a buyer's loss is capped at the premium while a seller takes on a duty, and why that asymmetry matters.

- ·The buyer can choose not to act

- ·Capped loss for the buyer

- ·The seller's obligation

- ·Why the seller is paid upfront

- ·Exercise and expiry worthless

- ·The core asymmetry

There is one feature that makes options different from almost everything else you can trade, and it hides inside that small phrase we keep repeating: the right, not the obligation. It sounds like a legal nicety. It is actually the whole reason options exist. That single asymmetry, where one side gets to choose and the other side must comply, shapes how every option behaves, why a buyer's loss is capped, why a seller demands payment up front, and why the two sides see the same contract so differently. This chapter slows right down on that one idea, because once you truly feel it, the rest of options falls into place.

Two sides, two very different deals

Every option has two people behind it. There is the buyer, also called the holder, who pays the premium and receives the right. And there is the seller, also called the writer, who collects the premium and takes on the obligation. The same contract gives one of them a choice and binds the other.

- The buyer holds a right. After paying the premium, the buyer can act or walk away. Nothing forces the buyer to do anything.

- The seller holds a duty. Having pocketed the premium, the seller must do as the buyer decides. If the buyer chooses to transact, the seller has to honour it.

This is not a fair, symmetric bet like a coin toss where both sides face the same outcomes. It is deliberately lopsided. The buyer has paid for the privilege of choosing, and the seller has been paid to give up that choice. Everything else about options flows from this lopsidedness.

An option is a one-sided deal. The buyer pays the premium and gets to choose. The seller receives the premium and must comply. That asymmetry is the defining feature of every option.

Exercise, or let it expire worthless

When expiry arrives, the buyer faces a simple decision with only two answers. This is where the right either gets used or thrown away.

To exercise an option means to use the right. A call buyer exercises by buying at the strike; a put buyer exercises by selling at the strike. You exercise only when it pays to, that is, when the locked strike beats the open market.

To let it expire worthless means to do nothing and let the right lapse. You choose this when exercising would be pointless, because the open market offers a better deal than your strike. The option simply dies and you keep whatever is left of your life, having lost only the premium.

Walk it through with the RELIANCE 1320 call, bought for a premium of about Rs 31 a share.

- RELIANCE finishes at 1400. Your right to buy at 1320 is precious. You exercise, effectively buying 80 rupees a share below the market. The right was worth using.

- RELIANCE finishes at 1290. Your right to buy at 1320 is useless, because the open market sells it cheaper. You let the option expire worthless and lose only the Rs 31 a share you paid, about Rs 15,590 for the lot.

For an index option this settlement happens in cash, the difference simply paid to you. A single-stock option like RELIANCE is instead settled by delivery of the shares if it is carried to expiry in-the-money, but the economic logic is the same: your gain is the gap between the strike and the market. Either way, most traders simply close the option in the market before expiry rather than go through settlement. The point is the freedom: you never have to exercise a losing option. That freedom is what caps your loss.

The buyer of the 1320 call never loses more than the premium. Whether RELIANCE finishes at 1300, 1200 or 1000, the answer is identical: let it expire, lose Rs 15,590, walk away. The downside is fenced off by the simple right to do nothing.

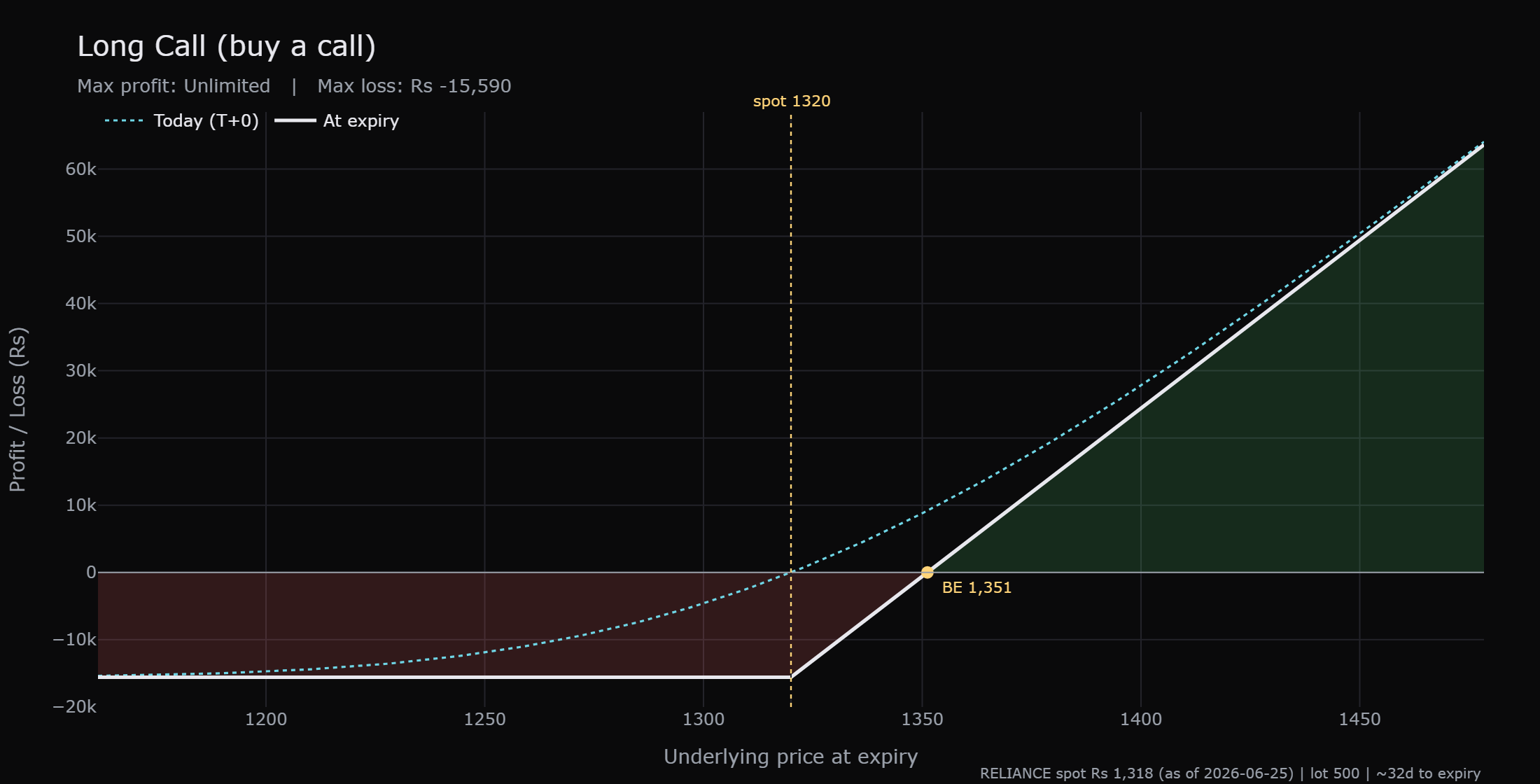

Reading the buyer's capped loss on the payoff

A payoff chart draws an option's profit or loss against where the underlying finishes at expiry. The horizontal axis is the stock price; the vertical axis is your rupee result. Learning to read one is a core skill, and the long call is the friendliest place to start.

Read it left to right.

- On the left, where RELIANCE finishes below the strike, the line is flat. It sits at a loss of about Rs 15,590, the full premium for the lot, and it does not get any worse however far left you go. That flat floor is the capped loss in picture form. No matter how badly the stock falls, the buyer's pain stops at the premium.

- The line then slopes up and crosses zero at 1351. This is the breakeven, the strike of 1320 plus the premium of about Rs 31 a share. The stock must clear 1351 just for the buyer to get the premium back. Below 1351 the trade is still a net loss, even if the option finished with some value.

- Above 1351 the line keeps climbing with no ceiling. The buyer's profit grows rupee for rupee as RELIANCE rises, which is the unlimited upside that makes calls attractive.

The whole shape is the asymmetry drawn out. Flat and capped on the downside, open and rising on the upside. That is exactly what the right, not the obligation, buys you.

The flat capped loss is comforting, but notice where breakeven sits. RELIANCE must climb from 1318 all the way past 1351, more than 30 rupees, before the buyer makes a single rupee, and it must do so before 28 July. The right protects you from disaster, but it does not make profit easy. Most call buyers still lose, because the stock fails to clear breakeven in time.

Why the seller collects the premium

Now flip to the other side. If the buyer has all this freedom, capped losses and open upside, why would anyone sell the option? The answer is the premium, and it is collected up front for a clear reason.

The seller is being paid to take on a duty with an unpleasant shape. Sell that 1320 call and you receive about Rs 15,590 the moment the trade is done, and it is yours to keep. In return you have promised to deliver at 1320 if you are assigned at expiry. If RELIANCE finishes well above 1320, you are assigned and you bear that loss. The seller's reward is capped at the premium received, while the risk runs the other way.

So the premium is not a gift. It is compensation for accepting an obligation that the buyer was glad to pay to avoid. The seller is, in effect, the insurance company. They collect steady premiums and, in exchange, they carry the risk of a large payout if the market moves hard against them.

- The buyer pays a small, certain amount and may gain a large, uncertain one.

- The seller takes a small, certain amount and may lose a large, uncertain one.

This is why time is the seller's friend. Every quiet day that passes brings the seller closer to keeping the whole premium, while it brings the buyer closer to a worthless, expired right. We will study that grind in detail in the chapter on time-value.

A useful way to remember it: the buyer rents optionality and pays for the privilege; the seller sells optionality and gets paid for the burden. Neither side is foolish. They simply hold opposite views on whether the move will be big enough to matter before expiry.

What to carry forward

The asymmetry at the centre of every option is now yours.

- The buyer pays the premium and holds the right. The buyer's loss is capped at the premium, about Rs 15,590 for the RELIANCE 1320 lot, while the upside stays open. This is the flat floor on the long call payoff.

- The seller collects the premium and holds the obligation. The seller's gain is capped at that premium, while the risk runs large in the direction the buyer hopes for.

- At expiry the buyer simply chooses: exercise when the strike beats the market, or let it expire worthless when it does not.

- Breakeven for the long call sits at 1351, the strike plus the premium per share. Capped loss does not mean easy profit, and most buyers still lose by failing to clear breakeven in time.

Next we sort options into the three families of moneyness, in, at and out of the money, which tells you at a glance whether a strike is already worth using, sitting right at the current price, or still pure hope.

Because the seller carries open-ended risk, selling options requires posting margin, a deposit the market holds against potential losses. Buyers post no margin beyond the premium itself, since the premium is already the most they can lose. The mechanics differ because the risks differ.