Buying a Put (Long Put)

The mirror image: profiting from a fall with limited risk. Learn the long put payoff, the breakeven below the strike, and how a put can act as insurance on a holding.

- ·When you buy a put

- ·Limited loss, the premium

- ·The breakeven below strike

- ·Large but capped profit

- ·A put as insurance

- ·Reading the real payoff

A call is the trade for when you expect a stock to rise. But markets fall too, sometimes hard and fast, and you want a way to profit when they do, or at least a way to protect what you own. That is the job of the long put, a put option you have bought. It is the exact mirror of the long call. Where the call gives you the right to buy at the strike, the put gives you the right to sell at the strike. You buy a put when you think RELIANCE is heading down, and the lower it goes, the more your put is worth. As with the call, your loss is capped at the premium you pay, while your reward grows as the stock falls. This chapter reads the real RELIANCE put payoff and then shows you the put's second, quieter job: insurance.

What you actually own

When you buy the RELIANCE 1320 put expiring 28 July, you pay about Rs 31 per share, the same modelled premium as the call. One lot is 500 shares, so the lot costs about Rs 15,590. The symbol reads RELIANCE28JUL261320PE, where PE marks it as a put.

That premium buys you the right, but never the obligation, to sell 500 shares of RELIANCE at 1320 at expiry. If RELIANCE crashes, that right becomes valuable, because you can sell at 1320 while the market trades far below, and before expiry you can also exit at any time by selling the put back in the market. If RELIANCE instead climbs, you let the put expire and lose only the premium. The most you can lose is the Rs 15,590 you paid, and not one rupee more.

A long put is the bought right to sell at the strike. You profit as the stock falls, your maximum loss is the premium you paid, and you never owe more than that. It is the mirror image of the long call, pointing down instead of up.

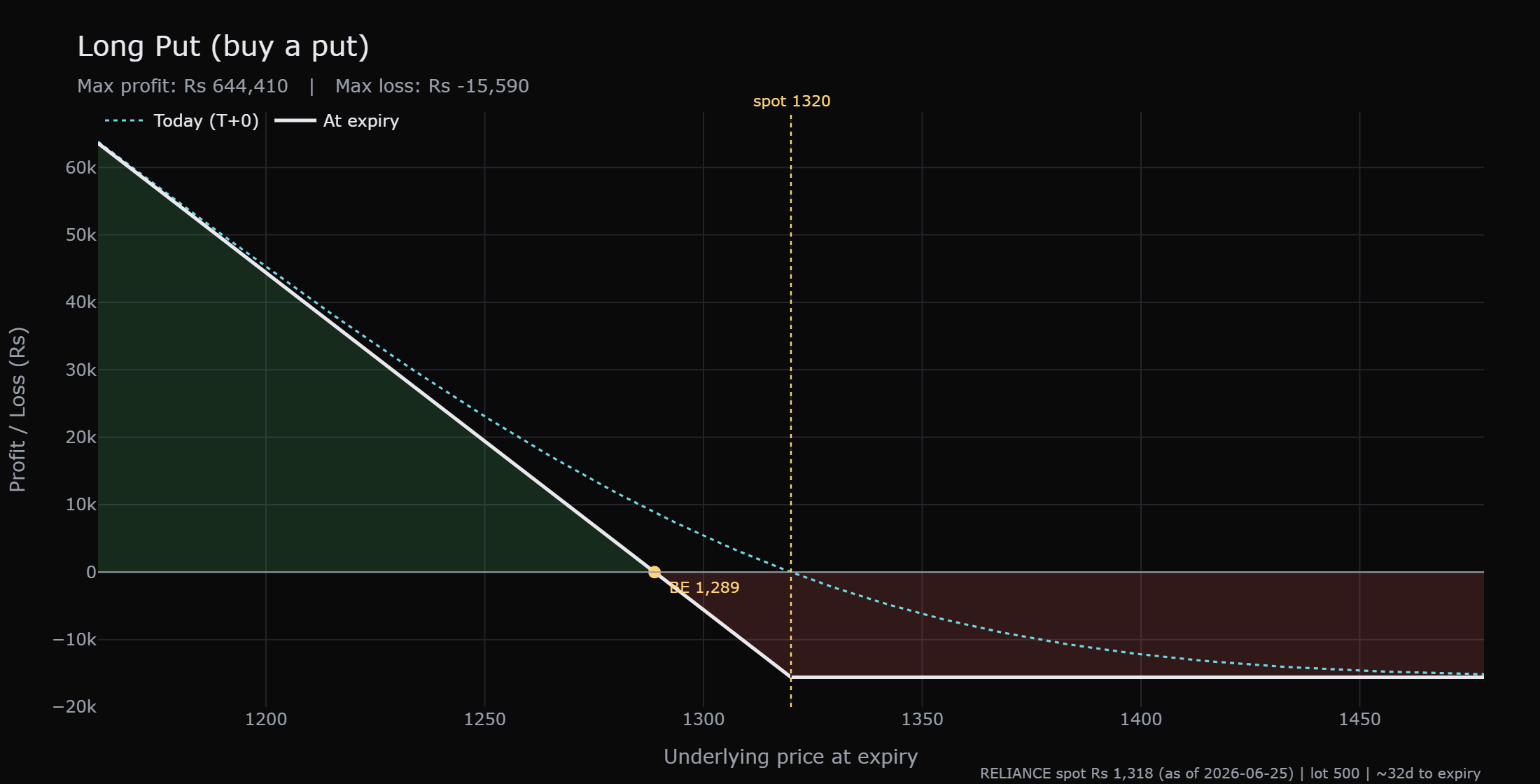

Reading the real payoff

The diagram below is the genuine payoff for this trade, from OpenAlgo's strategy maths on RELIANCE at spot Rs 1,318, strike 1320, lot 500, about 32 days to expiry, premium near Rs 31 a share. The solid line is the value at expiry on 28 July. The dotted cyan line is the value today, before time decay has run its course. We walk the solid line, this time from right to left, because a put rewards falling prices.

On the right, the line is flat. For any expiry price above the strike of 1320, the put finishes out-of-the-money and worthless. You lose the whole premium, about Rs 15,590, and that loss does not grow no matter how high RELIANCE climbs. Whether the stock ends at 1330 or rockets to 1500, your loss is the same capped Rs 15,590. This flat ceiling on the right is the put buyer's capped risk.

In the middle, the line hinges and starts to rise as price falls. Once RELIANCE drops below 1320, the put gains intrinsic value rupee for rupee. But you must first earn back the premium, so you are not yet in profit. The line crosses zero at the breakeven price of 1289, which is the strike of 1320 minus the Rs 31 premium per share. At exactly 1289 your gains on the right to sell cancel the premium you spent.

On the left, the line keeps climbing as RELIANCE falls. Below 1289 you are in real profit, and every further rupee the stock loses adds Rs 500 to your position, because you control 500 shares. If RELIANCE finishes at 1250, you are up roughly 39 rupees a share below breakeven, around Rs 19,500. If it falls to 1200, the profit grows further. The gain keeps building all the way down. The only natural limit is that a share price cannot fall below zero, so the put's profit is very large rather than truly infinite, but for any realistic move it behaves like the call's upside turned upside down.

Three endings for the 1320 put. RELIANCE at 1330 on expiry: the put is worthless, loss about Rs 15,590, the most you can lose. RELIANCE at 1289: you break even. RELIANCE at 1250: profit of roughly Rs 19,500, and it keeps growing the further the stock falls.

The same honest catch

Everything that made the long call hard applies just as firmly to the long put, only pointed downward. Most put buyers lose money too, and for the same reasons.

The stock must clear the breakeven, not just the strike. RELIANCE dipping below 1320 is not enough. It must fall past 1289 before expiry just for you to recover the premium. And time decay grinds against you the entire time. This at-the-money put is almost all time value, so its premium melts a little every day and fastest in the final week. You are betting on a fall, racing a shrinking clock. RELIANCE could slide from 1318 to 1295, a real drop, and the put buyer would still finish at a loss, because 1295 sits above the 1289 breakeven and time value bled away in the meantime. As with the call, you can be right on direction and still lose.

A long put can lose money even when RELIANCE falls. The stock must clear 1289 by expiry, and it must do so before time decay eats the premium. Buying far out-of-the-money puts and hoping for a crash is, like its call cousin, a slow way to lose capital.

The put's second job: insurance

Here is where the put earns its keep for ordinary investors, not just speculators. A put is insurance on shares you already own. This use is often called a protective put, and it is one of the most sensible things a beginner can understand.

Suppose you own 500 shares of RELIANCE, currently worth about Rs 6,59,000 at 1318. You are nervous about a fall over the next month, perhaps because of an upcoming event, but you do not want to sell your shares and trigger tax or miss a rebound. So you buy one 1320 put for about Rs 15,590. Now think about what you hold.

- If RELIANCE crashes to 1200, your shares lose value, but your put gains. The right to sell at 1320 while the market trades at 1200 offsets most of the fall. Your put has acted exactly like an insurance payout.

- If RELIANCE climbs to 1400, your shares profit handsomely, and you simply let the put expire. The Rs 15,590 you spent was the cost of the insurance, the premium you paid for a month of protection that you happily did not need.

That is the honest framing. A protective put behaves like an insurance policy on your holding. It costs a premium, it expires, and you hope you never collect on it, just as you hope never to claim on a motor policy. The cost is real and it repeats each time you renew, but the peace of mind and the capped downside can be worth it through a worrying patch.

Think of a protective put as a one-month insurance policy on your RELIANCE holding. The premium is the cost of the cover, the strike is the price floor it guarantees, and the expiry is when the policy lapses. You buy it hoping the stock rises and the policy goes unused.

When a long put makes sense

Beyond insurance, a speculative long put is a reasonable tool in the same disciplined situations as the call, just inverted.

- You expect a sizeable fall, soon. A put rewards a move that is large and reasonably quick, enough to clear the breakeven before decay bites.

- You want defined, capped risk on a bearish view. Unlike short selling shares, your loss on a long put can never exceed the premium. That hard cap of Rs 15,590 is known the moment you buy.

- You are risking only money you can afford to lose entirely, because the whole premium can decay to nothing.

At expiry the long put is pure intrinsic value: how far it finished below the strike, multiplied by 500, minus the premium you paid. Above 1320 it is worthless. The dotted today line sits above the solid expiry line by the time value the option still holds now and will surrender by 28 July.

You can rehearse all of this, the speculative put and the protective put, in sandbox trading (analyzer mode in OpenAlgo) before committing real money, watching the premium react as RELIANCE moves and as the days tick down.

So the long put gives you a capped loss of about Rs 15,590, a breakeven at 1289, and a large and growing profit as RELIANCE falls. As a speculation it carries the same honest catch as the call, so buy it for a real, sizeable, timely move and not on vague gloom. As insurance on shares you own, it is one of the most sensible uses of an option there is. We have now met both sides of buying. Next we cross to the other side of the table and become the seller, where the premium comes to us, but so does a far heavier kind of risk.