Implied Volatility: The Market's Fear Gauge

Implied volatility is the market's expectation of how much price will move, baked into the premium. Learn why high IV makes options expensive and why buying before a known event can backfire.

- ·What implied volatility is

- ·IV and the premium

- ·High IV vs low IV

- ·IV crush after an event

- ·Why expensive options disappoint buyers

- ·Reading IV practically

Here is a puzzle that confuses almost every new trader. Two RELIANCE call options, same strike of 1320, same expiry of 28 July, can be worth very different premiums on two different days even when the stock is sitting at exactly the same price. Nothing about the strike changed. Nothing about the time left changed much. Yet one day the call costs Rs 31 a share and another day a similar option costs far more or far less. The missing ingredient is implied volatility, the single most misunderstood number in all of options trading. It is the market's fear gauge, and once you can read it, you stop overpaying for hope and you understand why being right on direction sometimes still loses money.

What implied volatility actually is

Implied volatility, usually shortened to IV, is the market's expectation of how much RELIANCE will move between now and expiry, expressed as a percentage and baked straight into the option's premium.

That is the whole idea. When traders expect RELIANCE to swing around wildly in the coming weeks, they are willing to pay more for options, because a bigger expected swing means a better chance the option finishes deep in-the-money. When traders expect RELIANCE to drift along quietly, they pay less, because a small expected move means options are less likely to pay off. The premium, in other words, contains a forecast of turbulence, and IV is that forecast pulled back out of the price.

A few things make IV easy to misread, so let us be precise.

- IV is forward looking. It is not a measure of how much RELIANCE has moved in the past. It is the market's guess about the future, which can be wrong.

- IV is implied, meaning it is reverse engineered from the price people are actually paying, not read off the stock directly. If the premium is high relative to the time and the strike, IV is high, by definition.

- IV is quoted as an annual percentage. Our RELIANCE anchor carries an IV of about 20 percent, a fairly calm reading. A frightened market on a single stock can push IV far higher.

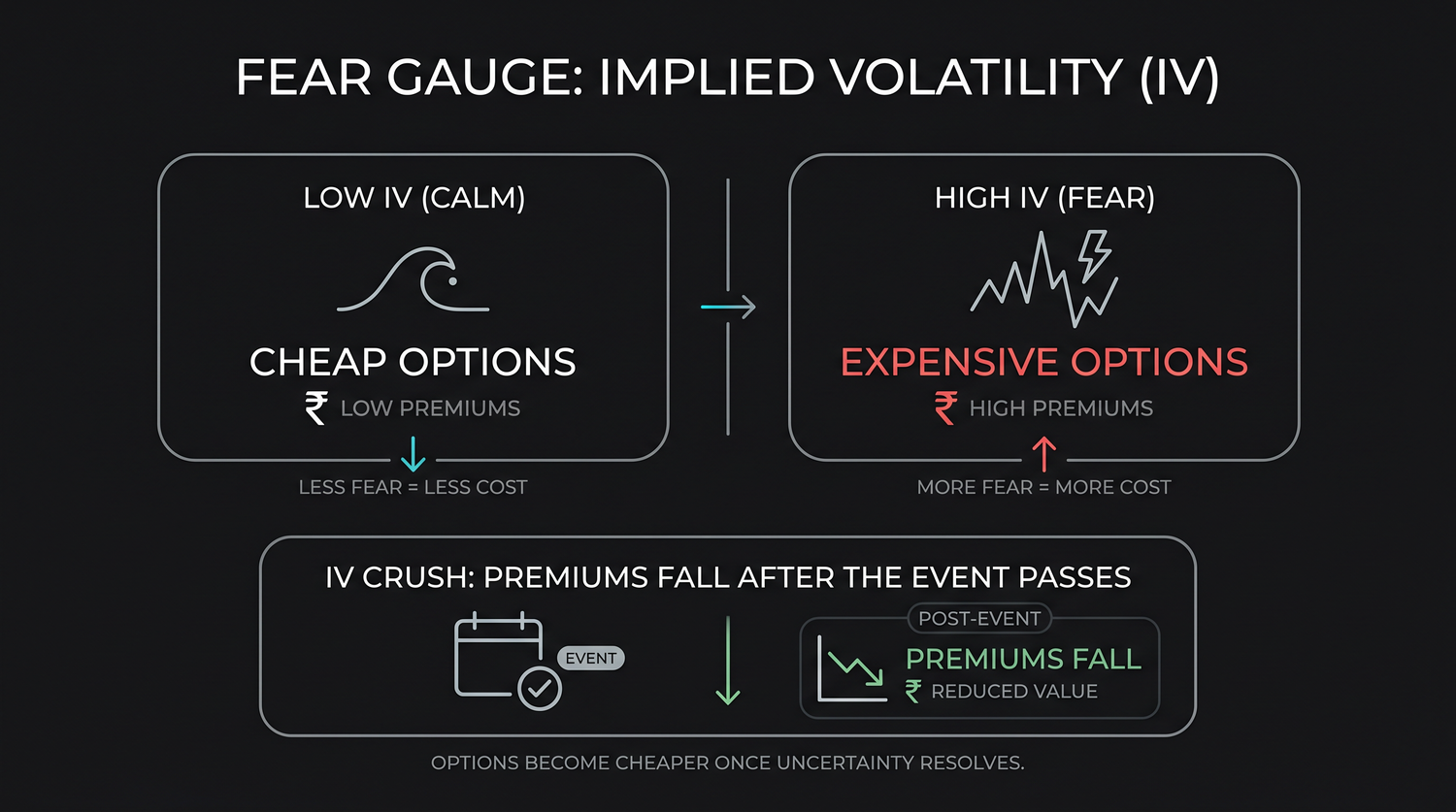

Implied volatility is the market's expectation of how much RELIANCE will move, baked into the premium. High IV means the market expects a big move and options are expensive. Low IV means the market expects calm and options are cheap. It is a forecast of turbulence, not a measure of the past.

High IV makes options expensive, low IV makes them cheap

The practical consequence of IV is the most important thing in this chapter, so let us make it concrete on the RELIANCE 1320 option. Hold the stock still at 1318, hold the expiry at 28 July, and change only the level of fear in the market.

| Market mood | Implied volatility | The 1320 call roughly costs |

|---|---|---|

| Calm and quiet | About 15 percent | Less than our anchor premium |

| Our anchor case | About 20 percent | About Rs 31 a share, Rs 15,590 a lot |

| Nervous before news | About 35 percent | Well above the anchor premium |

| Fearful, event looming | 50 percent or more | Far above the anchor premium |

Read down that table and notice what is happening. The stock has not moved. The strike has not changed. The expiry is the same. The only thing that changed is the market's expectation of movement, and the premium swelled or shrank with it. The same option that costs about Rs 31 a share in a calm market can cost two or three times that just before a nervous event, purely on fear.

This is why two traders can buy the very same RELIANCE call and have wildly different outcomes. The one who bought when IV was low got their hope cheaply. The one who bought when IV was high overpaid for the same hope, and now needs an even bigger move just to break even, because so much of the premium was fear that can evaporate.

Before buying any option, ask whether implied volatility is high or low right now. Buying when IV is high means you are paying a fear premium that can drain away on its own. The cheapest hope is bought when the market is calm, not when everyone is already scared.

IV crush: the trap that catches beginners

The most painful lesson IV teaches has a name: IV crush. It is the experience of buying an expensive option just before a known event, being right about the direction, and still losing money because the premium collapses after the event passes.

Here is how it unfolds. RELIANCE has a major announcement coming, perhaps quarterly results. Everyone knows the date. In the days before, traders pile into options expecting a big move, and that demand drives implied volatility sharply higher. The 1320 call that would cost about Rs 31 a share in calm conditions might now cost far more, because it is stuffed with fear premium. A beginner sees the excitement, expects the stock to jump, and buys the inflated call.

Then the announcement comes out. The uncertainty is gone, the event is now known, and implied volatility collapses back to normal almost instantly. This collapse is the crush. Because so much of the premium was fear, the premium falls hard the moment the fear disappears. And here is the cruel part. RELIANCE might actually rise on good results, exactly as the beginner hoped, and the call can still lose money, because the gain from the stock's move was smaller than the loss from the vanishing IV.

Buying an option just before a known event is one of the most common beginner traps. You pay an inflated, high IV premium, the event passes, implied volatility collapses, and the premium falls even if you were right on direction. The market already priced the expected move into what you paid. To win, the actual move must beat that priced in expectation, not just point the right way.

The lesson is not that events are untradeable. It is that the market is not naive. When everyone expects a big move, that expectation is already in the price, and you are paying for it. The option only rewards you if the real move is larger than the one the crowd already paid for. Most of the time it is not.

Reading IV practically

You do not need to model volatility to use it. You need a few habits of mind that keep you from overpaying.

- Check whether IV is high or low for this stock right now. OpenAlgo reports the implied volatility for each RELIANCE strike. A reading well above the stock's usual range is a warning that options are expensive and a fear premium is present.

- Be cautious buying before known events. Results, policy decisions and major announcements pump IV up beforehand and crush it afterwards. If you must take a view through an event, know that you are paying inflated prices and the crush is coming.

- Remember that low IV cuts both ways. Cheap options are appealing, but low IV also means the market expects little movement, so the move you are betting on may simply not arrive. Cheap is not the same as likely.

- Sellers think the opposite way. A seller wants to collect premium when IV is high and rich, then profit as it falls back. This is the mirror of the buyer's trap, and it is part of why selling appeals to experienced traders, though it carries the large risk we have already met.

High IV is not automatically a reason to sell, and low IV is not automatically a reason to buy. IV tells you how expensive the hope is, not which way the stock will go. A trader still has to be right about direction. IV only decides whether the ticket to that bet is cheap or dear.

It helps to watch all of this behave in sandbox trading (analyzer mode in OpenAlgo). Pull up the RELIANCE 1320 call, note its implied volatility and premium on a calm day, then watch how both react as a busy event approaches and passes. Seeing the premium swell on fear and crush afterwards, with the stock barely moving, teaches the lesson far more deeply than any warning can.

The premium you pay already contains the market's best guess about future movement. You are never simply betting that RELIANCE will rise or fall. You are betting it will rise or fall by more than the amount the market has already priced into implied volatility. That is the real bar every option buyer has to clear.

Implied volatility is the last big concept in how options are priced, and it ties the whole picture together. Strike and expiry set the frame, intrinsic value and time value split the premium, the Greeks measure how it reacts, and IV decides how richly that reaction is priced. With all of that in hand, the final chapter turns from theory to the hard practical mechanics: lot size and the true cost of a trade, how Indian options settle at expiry, and the honest risks you must respect before you ever risk real money.