Basis and the Cost of Carry

A future rarely trades at exactly the spot price. Learn the basis (the gap between future and spot) and the cost of carry that explains it, plus what a premium or discount is telling you.

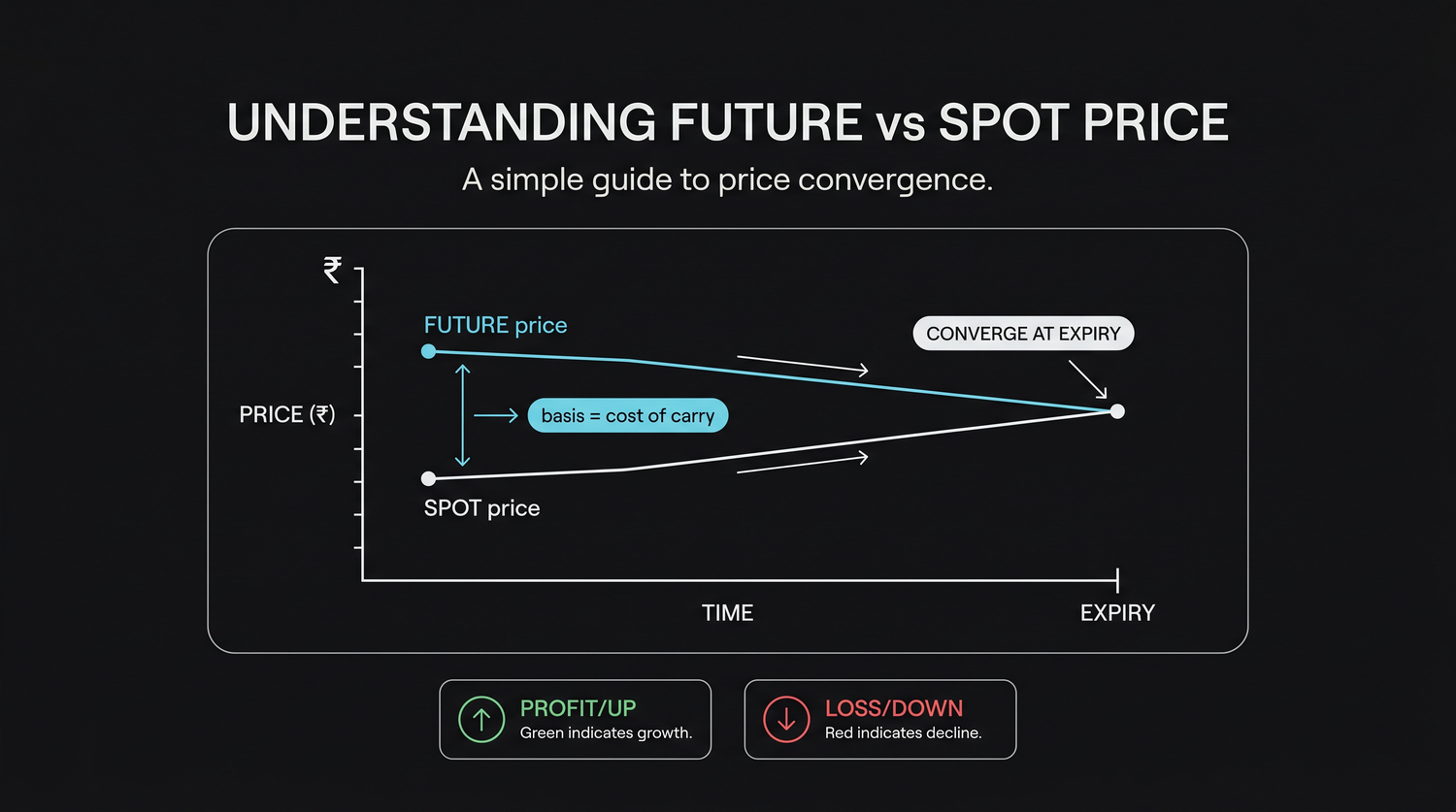

- ·Future price vs spot price

- ·The basis explained

- ·Cost of carry

- ·Premium and discount

- ·Convergence at expiry

- ·What the basis signals

Look up RELIANCE on a quote screen and you will notice something that puzzles every newcomer. The share itself shows one price, around Rs 1,318, while the RELIANCE future for the coming expiry shows a slightly different price, perhaps Rs 1,326. Same company, same day, same moment, yet two prices. Nobody made a mistake. The future is supposed to trade away from the spot price, and the small gap between them is one of the most informative numbers in the whole market. Learn to read that gap and you gain a quiet window into financing costs, time, and the mood of other traders.

That gap has a name, the basis, and the force that creates it has a name too, the cost of carry. Neither idea requires any mathematics beyond simple arithmetic, and both are worth understanding deeply. They explain why a future is priced the way it is, why that price drifts toward the spot as expiry nears, and what a premium or a discount is quietly telling you.

A future rarely trades at spot

The price of the underlying right now, the price at which you could buy or sell the actual share this instant, is called the spot price. For RELIANCE that is about Rs 1,318. The future is a contract to settle that same share at a fixed date in the future, in our example 28 July 2026, roughly 32 days away.

Because the future settles later, it almost never trades at exactly the spot price. There is a sound reason. Owning the future for the next 32 days is not quite the same as owning the share for the next 32 days, and the market prices that difference in. Most of the time the future trades a little above spot. Sometimes it trades a little below. The point to absorb first is simply this: a small gap between future and spot is normal and expected, not a glitch.

The spot price is what the underlying costs right now. The futures price is what it will settle for at expiry. They are almost never identical, and the gap between them carries real meaning.

The basis is the gap

The basis is simply the difference between the futures price and the spot price. If the future trades at 1326 while spot sits at 1318, the basis is 8 points. Conventions differ on which way to subtract, and some traders quote it the other way around, but the idea is the same in both directions: the basis measures how far the future sits from the cash market.

Two words describe the two situations you will meet:

- When the future trades above spot, the market is at a premium. In our example the 8 point gap is a premium of 8 points.

- When the future trades below spot, the market is at a discount. A future at 1310 against a spot of 1318 would be a discount of 8 points.

For most Indian stock and index futures, in normal conditions, a premium is the usual state. So seeing the RELIANCE future a handful of points above the share is exactly what you would expect. The interesting questions are why that premium exists and what it means when the gap is unusually large, unusually small, or flips into a discount.

| Basis state | Future versus spot | What it usually reflects |

|---|---|---|

| Premium | Future above spot | Normal cost of carry, calm to slightly bullish positioning |

| Discount | Future below spot | A large upcoming dividend, or bearish short positioning |

| Near zero | Future close to spot | Expiry approaching, the carry has almost run out |

Cost of carry: why a future trades at a premium

The reason a future usually trades above spot is the cost of carry, the cost of holding the underlying until expiry. Imagine someone who wants to own RELIANCE shares at expiry. They have two routes. They could buy the shares today and hold them for 32 days, or they could buy the future and settle later. To make those two routes fairly priced against each other, the future has to account for what holding the shares actually costs.

The biggest part of that cost is financing. Money used to buy the shares today is money that could otherwise sit earning interest, or money that has to be borrowed at an interest rate. Tying it up in shares for 32 days has a cost, and that cost is built into the futures price. The longer the time to expiry and the higher the interest rate, the larger the carry, and so the larger the premium.

You can sketch the size without any code. Take RELIANCE spot at 1318, a financing rate in the region of seven percent a year, and 32 days to expiry. Seven percent for a full year on 1318 would be about 92 points, but you are only carrying for 32 days, which is roughly a twelfth of a year, so the carry works out near 8 points. That is why a future at about 1326 looks fair. The premium is just the spot price plus the cost of holding it to expiry.

- A longer time to expiry means more days of carry, so a wider premium.

- A higher financing rate means a more expensive carry, so a wider premium.

- As expiry approaches, fewer days of carry remain, so the premium naturally shrinks.

One detail trims the carry the other way. If the underlying pays a dividend before expiry, the holder of the actual shares receives that cash while the futures holder does not, which reduces the net cost of carrying the shares. A large upcoming dividend can therefore shrink the premium, and around a heavy dividend a future can even slip into a discount for sound, mechanical reasons rather than any view on direction.

RELIANCE spot at 1318, a financing cost near seven percent a year, and 32 days to the 28 July 2026 expiry give a carry of roughly 8 points. Add that to spot and a fair futures price lands near 1326, which is exactly the kind of premium you see on the screen.

What a discount can signal

If a premium is the normal state, a discount, where the future trades below spot, stands out. Sometimes it is purely mechanical, the dividend effect just described. But when there is no large dividend to explain it, a discount often carries a message about sentiment.

A future falls to a discount when sellers are willing to sell the future below the cash price, which usually means traders are leaning bearish and pressing short positions in the future. The futures market, being leveraged and easy to short, is often where a negative view shows up first. So a stock or index future drifting into discount, or a premium that suddenly collapses, can be an early hint that traders expect weakness, even while the spot price still looks calm.

The signal is never a certainty, and it should never be traded on by itself. But a basis that behaves oddly is worth noticing. A premium widening sharply suggests eager buyers paying up for leveraged exposure. A premium shrinking or flipping to a discount suggests the opposite mood is creeping in.

A futures premium is the ordinary state for most Indian stocks and indices. A persistent discount that a dividend cannot explain often reflects bearish positioning, traders shorting the future below the cash price.

Convergence: the basis must vanish at expiry

Here is the anchor that ties the whole idea together. However wide the basis is today, it must shrink to zero by expiry. This is called convergence, and it is not a tendency or a probability. It is a certainty built into the contract.

The reason is simple. On the expiry date the future stops being a promise about the future and becomes a settlement at that day's actual price. At that final moment there is no time left to carry, no financing cost to add, no days remaining. So the future can only settle at the spot price. The two lines that started apart are forced to meet. An 8 point premium today must melt away to nothing over the next 32 days, a little each day as the carry runs down.

This convergence is what makes the basis trustworthy as a measure. You are not watching a random wobble. You are watching a gap that has a known destination of zero on a known date, drifting toward it as expiry nears.

- The premium is widest when expiry is far away and the most carry remains.

- It narrows steadily as the days count down.

- At expiry the future and the spot are the same price, the basis is zero.

Do not mistake the everyday narrowing of the premium for the stock falling. As expiry nears, a long futures position loses a little to convergence even if the spot price holds perfectly steady, simply because the premium you bought is decaying toward zero. Factor the basis into what you expect to earn.

What the basis tells you

Pull the threads together and the basis becomes a small instrument panel for the futures trader. The size of the premium tells you roughly how much carry is priced in, which depends on time and interest rates. The direction tells you about mood. A healthy premium signals normal, slightly bullish positioning. A shrinking premium or an unexplained discount signals caution or bearishness. And convergence reminds you that whatever the gap is today, it is on a guaranteed path to zero at expiry.

When you compare a future against its spot, do not just note the numbers. Ask why the gap is the size it is. Is it ordinary carry for the days remaining, an upcoming dividend, or a shift in sentiment? That single habit turns the basis from a curiosity into a genuine read on the market.

The basis and the cost of carry explain why a future lives a few points away from its spot, why that distance is usually a premium, why a discount can hint at bearishness, and why the gap always closes to zero at expiry. None of it needs a formula to grasp. It needs only the picture of two prices, drawn apart by the cost of holding the underlying through time, and drawn back together as that time runs out.