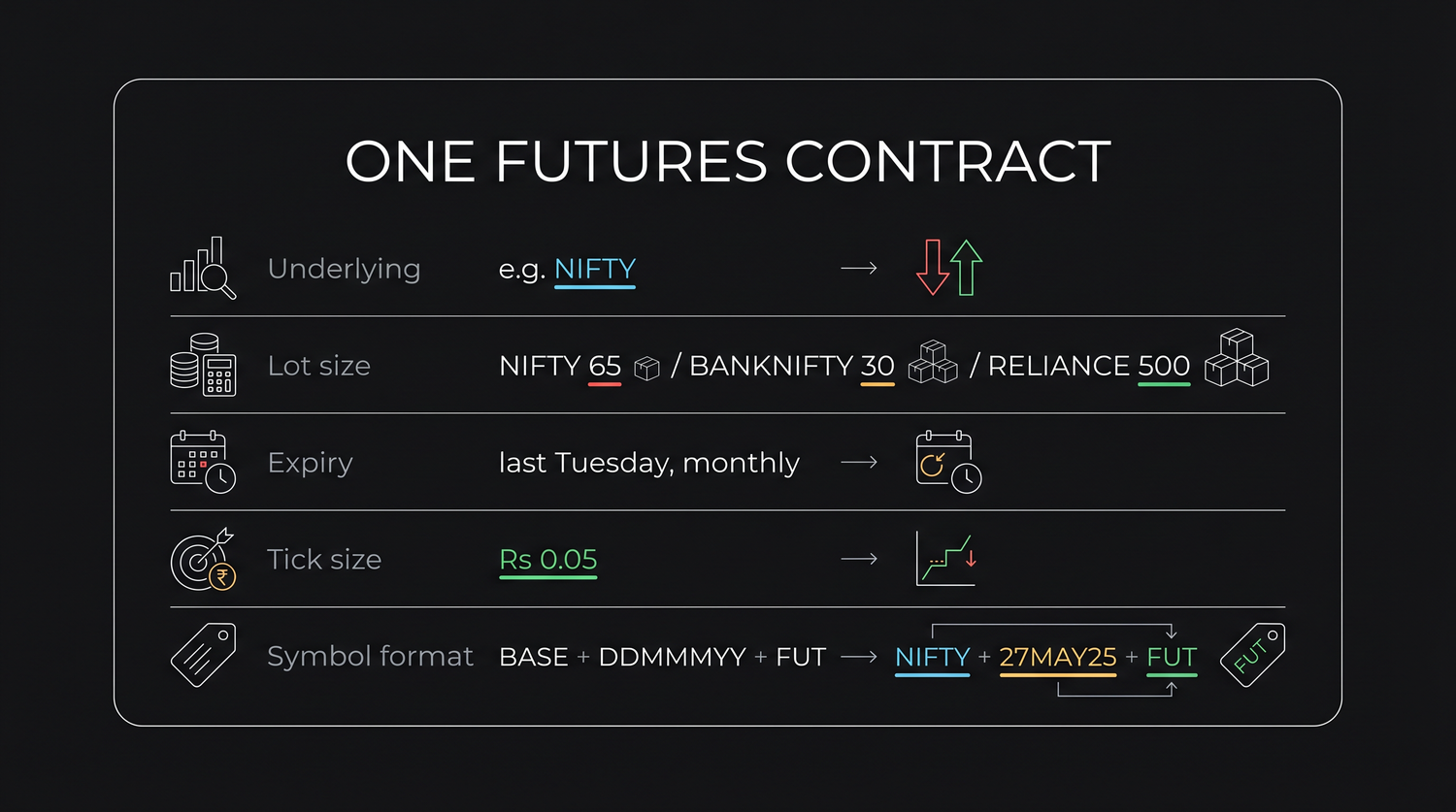

Reading a Contract: Lot Size, Expiry and Tick

Every future is standardised. Learn the lot size (NIFTY 65, BANKNIFTY 30, RELIANCE 500), the monthly expiry, the tick size and the symbol format, so you know exactly what one contract controls.

- ·Lot size and contract value

- ·Real lot sizes (NIFTY, BANKNIFTY, RELIANCE)

- ·Monthly and weekly expiry

- ·Tick size and minimum move

- ·The OpenAlgo symbol format

- ·Why everything is standardised

When you buy a share of RELIANCE, you decide everything. You choose how many shares, you pay the going price, and you can buy a single share or ten thousand. A futures contract takes most of those choices away from you, and that is deliberate. Every future is standardised, meaning the exchange has already decided the quantity, the expiry, and the smallest price step before you ever place an order. At first this feels restrictive. In reality it is the very thing that makes the market liquid and fair, because everyone is trading an identical, well-defined product. In this chapter we read a contract the way a careful trader does, spec by spec, until nothing on the order screen is a surprise.

Lot size, the quantity is fixed for you

The lot size is the fixed number of units in one futures contract. You cannot buy half a lot or a custom amount. You trade in whole lots, and the exchange sets the lot for each underlying. For RELIANCE the lot is 500 shares, so one contract always represents exactly 500 shares of the stock, no more and no less.

From the lot size flows the most important number a beginner can learn to compute, the contract value. This is simply the lot size multiplied by the price of the underlying. With RELIANCE near Rs 1,318, one contract of 500 shares is worth about Rs 6,59,000. That is the real economic exposure you take on with a single lot, even though, as we will see in the margin chapter, you do not pay anywhere near that amount upfront. Knowing the contract value keeps you honest about how much money is genuinely at risk.

Different underlyings have very different lots, and the exchange sizes them so that one lot is a meaningful but not absurd amount of money. Here are the current lots for the most traded Indian contracts.

| Underlying | Lot size | Roughly controls per lot |

|---|---|---|

| NIFTY | 65 | a large slice of the index |

| BANKNIFTY | 30 | a large slice of the banking index |

| FINNIFTY | 60 | a slice of the financial services index |

| MIDCPNIFTY | 120 | a slice of the midcap index |

| RELIANCE | 500 | about Rs 6,59,000 of stock |

Lot size is fixed by the exchange and never optional. Contract value equals lot size times the underlying price. For one RELIANCE lot, 500 shares times about Rs 1,318 is roughly Rs 6,59,000 of real exposure.

Notice that the index lots are quoted in index units rather than rupees, because an index is not something you can hold in your hand. The rupee value of a NIFTY lot is the lot of 65 multiplied by the index level. The principle is identical to RELIANCE. Lot size times price gives you the exposure.

Expiry, the contract has a deadline

Unlike a share, which you can hold forever, every future comes with an expiry, the date the contract ceases to exist. After expiry the contract is settled and gone, and if you want to keep a position you must move to a later contract, a process we cover in a later chapter on rollover.

Indian futures come in two broad rhythms.

- Monthly contracts, which single-stock futures such as RELIANCE follow. On the NSE futures and options segment (the NFO), the monthly contract settles on the last Tuesday of the expiry month, so the RELIANCE contract in our examples expires on Tuesday 28 July 2026, about 32 days from our anchor date. There is a near month, the next month, and a far month available at any time.

- Weekly contracts, which the most active index (currently the NIFTY weekly) offers in addition to the monthly ones, giving traders a steady supply of short-dated expiries to trade around. These weekly index contracts also settle on a Tuesday.

Know your settlement day, because it has changed and it differs by exchange. NSE derivatives (the NFO segment), which covers NIFTY, BANKNIFTY and single-stock futures like RELIANCE, now settle on Tuesday. BSE derivatives (the BFO segment), such as the SENSEX, settle on Thursday. Every example in this course uses an NSE instrument, so our expiries land on a Tuesday.

For a beginner the practical advice is plain. Trade the near month. The near-month contract is where the bulk of the volume and the tightest prices live. Far-month contracts exist, but they are thinly traded, and a beginner who wanders into them often finds wide prices and trouble getting out. We will return to this when we discuss liquidity.

A future is not a buy-and-hold instrument. It expires. If you forget an open position into expiry it will be settled automatically, possibly into physical delivery for a stock such as RELIANCE, which is rarely what a small trader intends. Always know your expiry date.

Tick size, the smallest legal step

The tick size is the minimum amount by which the price of a contract can change. For most Indian stocks, including RELIANCE, the tick is Rs 0.05. This means the price can move from Rs 1,318.00 to Rs 1,318.05 to Rs 1,318.10, but never to an in-between value such as Rs 1,318.03. The exchange rounds the entire market to this grid so that prices are clean and orders can be matched without ambiguity.

The tick matters more than it first appears, because each tick is real money once you multiply by the lot. One tick of Rs 0.05 on a RELIANCE lot of 500 shares is Rs 0.05 times 500, which is Rs 25. So the smallest possible flicker in the RELIANCE future is worth Rs 25 to your position. A move of one full rupee, twenty ticks, is Rs 500. This is the same one-to-one relationship we will lean on again and again. Every Rs 1 the underlying moves is Rs 500 per RELIANCE lot.

RELIANCE futures tick up by Rs 0.05. On a lot of 500 shares that single tick is worth Rs 25, because 0.05 times 500 is 25. If the price climbs ten ticks, that is Rs 0.50, and your lot gains Rs 250. The tick looks tiny on the screen but it scales straight up with the lot size.

The symbol, reading the contract's name

Every contract has a precise machine-readable name, and learning to read it removes a lot of beginner confusion. On OpenAlgo the format for a future is the base symbol, then the expiry written as day, month and year, then the letters FUT. Our worked RELIANCE contract is therefore written RELIANCE28JUL26FUT.

Read it left to right.

- RELIANCE is the underlying, the base symbol.

- 28JUL26 is the expiry, the day, the three-letter month, and the two-digit year.

- FUT marks it as a futures contract, as opposed to an option, which would instead carry a strike price and the letters CE or PE.

Once you can decode the symbol, you can never accidentally trade the wrong month or confuse a future with an option, because the name itself tells you exactly what it is. This is standardisation working in your favour. The same RELIANCE future has the same name on every screen, for every trader, everywhere.

When you load a contract in OpenAlgo, read the full symbol aloud before placing an order. Confirm the base, the expiry month, and the FUT tag. This three-second habit prevents the classic beginner mistake of buying the far month, or an option, by accident.

Why standardisation builds a liquid market

Step back and notice what all this fixed structure achieves. Because the lot, the expiry, and the tick are identical for every participant, a buyer in one city and a seller in another are trading precisely the same instrument. There is no haggling over quantity or quality. The contract is a known quantity, literally. That sameness is what lets thousands of orders pool into one deep, liquid market where you can enter and exit quickly at fair prices.

Compare this with the baker and farmer from the first chapter, who had to negotiate every term of their private deal face to face. A private contract is flexible but illiquid. You cannot easily sell your half of a custom handshake to a stranger. A standardised exchange-traded future throws away that flexibility on purpose, and in return you gain a market where your position can be closed in seconds because the person on the other side is buying the exact same standardised thing.

Standardisation is the hidden engine of every liquid futures market. The exchange fixes the boring details, lot, expiry and tick, precisely so that the interesting detail, the price, is the only thing left for traders to argue about.

You now know how to read a contract before you ever risk a rupee. Check the lot to find your true exposure, check the expiry so the deadline never ambushes you, check the tick to know what each price step is worth, and read the symbol so you trade exactly the contract you intend. In the next chapter we confront the feature that makes futures both thrilling and dangerous, the fact that you control all of that Rs 6,59,000 of RELIANCE while posting only a slice of it as margin.