Liquidity, the Bid-Ask Spread and Slippage

The last traded price can mislead you. Learn the bid, the ask and the spread you actually trade against, what slippage and impact cost mean, and why a far-month or thin stock future can cost far more to enter and exit than the screen suggests.

- ·Why the LTP can mislead

- ·Bid, ask and the spread

- ·Slippage on entry and exit

- ·Impact cost in thin contracts

- ·Far-month and stock-future risk

- ·Trading only liquid contracts

There is a cost in trading that never shows up on your contract note, yet it quietly nibbles at every position you ever take. It is not brokerage, it is not tax, and it is not the price moving against you. It is the simple fact that the price you can buy at and the price you can sell at are never quite the same, and that getting in and out of a contract is itself an expense. Beginners obsess over picking the right direction and forget this hidden toll entirely. Skilled traders think about it before they place a single order. In this chapter we open up that hidden cost and learn to see it the way the market sees it, through liquidity, the bid-ask spread, market depth, and slippage.

Liquidity, how easily you can get in and out

Liquidity is the single most important word in this chapter. It means how easily you can enter or exit a position without your own order moving the price against you. A liquid contract has crowds of buyers and sellers standing ready at almost every price, so when you want to buy, a willing seller is right there, and when you want to sell, a willing buyer appears instantly, all at prices very close to where the contract was just trading.

A thin, or illiquid, contract is the opposite. Few people are trading it, the orders are sparse, and the moment you try to buy or sell any real size you find there is nobody waiting at the price you wanted. You either fail to fill or you fill at a much worse price because you have to reach far up or far down the ladder to find a counterparty.

Think of it as the difference between selling a popular flat in a busy city and selling a remote plot of land. The flat has many eager buyers, so you can sell quickly at a fair price. The plot might sit for months, and to sell it at all you may have to drop your asking price sharply. The flat is liquid. The plot is illiquid. Futures contracts sit all along this spectrum, and knowing where the one you are about to trade falls is a basic survival skill.

Liquidity is how easily you can enter or exit without moving the price. A liquid contract has many buyers and sellers ready at close prices, so you trade quickly and fairly. A thin contract punishes you the moment you try to get in or out.

The bid-ask spread, a toll on every round trip

Open any contract and you will see two prices at the front of the queue. The bid is the highest price anyone is currently willing to buy at. The ask, sometimes called the offer, is the lowest price anyone is currently willing to sell at. The gap between them is the bid-ask spread, and it is the clearest single measure of liquidity you will ever look at.

Here is why the spread is a real cost and not just a number. If you buy a future right now with a market order, you pay the ask, the higher price. If you turned around and sold it again immediately with another market order, you would receive the bid, the lower price. You would lose the spread without the price having moved at all. The spread is therefore the toll you pay every time you make a complete round trip into and out of a position.

Let us put rupees on it using RELIANCE. From an earlier chapter on contract specs, recall that the tick size, the smallest legal price step, is Rs 0.05, and that on a lot of 500 shares one tick is worth Rs 0.05 times 500, which is Rs 25. Now imagine the RELIANCE future shows a bid of Rs 1,319.95 and an ask of Rs 1,320.00. That is a spread of one tick, Rs 0.05. If you buy at the ask and instantly sell at the bid, you are down exactly one tick, which on a single lot is Rs 25, before the market has done anything. If the spread were two ticks, Rs 0.10, that same round trip costs you Rs 50 a lot. The wider the spread, the heavier the toll.

RELIANCE future, bid Rs 1,319.95, ask Rs 1,320.00. The spread is one tick of Rs 0.05. On a lot of 500 shares that is Rs 25. Buy at the ask and sell at the bid in the same breath and you have paid Rs 25 a lot for nothing but the privilege of crossing the spread. This is separate from brokerage and taxes, which a later chapter on costs covers in full.

A single Rs 25 sounds trivial against a contract worth about Rs 6,59,000. It is. The danger is not one crossing, it is repetition. A trader who jumps in and out ten times a day is paying that toll twenty times, and on a wider or thinner contract the toll is far larger. The spread is small for the patient and expensive for the restless.

Market depth, the five-level ladder

The bid and ask are only the front of a much longer queue. Market depth is the full picture, usually shown as a ladder with five levels of buy orders on one side and five levels of sell orders on the other. Each level shows a price and the quantity, the number of contracts, resting at that price.

Reading the depth tells you not just where the best prices are, but how much size sits behind them. A deep, liquid contract shows large quantities stacked at every level, close together. A thin contract shows a few scattered orders with gaps between the prices and small quantities at each. The depth ladder is the x-ray that reveals whether a contract can absorb your order or will choke on it.

This matters most when your order is larger than the quantity available at the best price. Suppose only 200 shares are offered at the ask of Rs 1,320.00, but you want to buy a full lot of 500. Your order takes all 200 at Rs 1,320.00, then climbs to the next level to fill the remaining 300, perhaps at Rs 1,320.10 or higher. Your average buying price ends up worse than the price you saw when you clicked. That is the depth ladder teaching you a hard lesson the instant you ignore it.

Before you send a market order, glance at the depth ladder. If healthy size sits at the top few levels and the prices are tightly packed, the contract can take your order cleanly. If the levels are thin and spread far apart, slow down, use a limit order, or trade a smaller size.

Slippage and impact cost

When the price you actually get filled at is worse than the price you expected when you placed the order, the difference is called slippage. It is the natural consequence of crossing a book that is not deep enough to satisfy your order at one price. You aimed for Rs 1,320.00 and the market gave you an average of Rs 1,320.12. Those twelve paise of slippage, on a lot of 500, are Rs 60 that vanished into the thinness of the book.

Closely related is impact cost, the idea that the very act of placing a large order pushes the price away from you. A small order barely disturbs a deep market. A large order in a thin market eats through several levels of the ladder, and the deeper you reach for fills, the worse your average price becomes. Impact cost grows with the size you are trying to trade relative to the liquidity available. The same order that fills cleanly in the near-month NIFTY future could move the price noticeably in a small single-stock future.

The instrument that exposes you to slippage is the market order, which says fill me now at whatever price is available. It guarantees a fill but not a price. Its partner, the limit order, names the worst price you will accept and protects you from slippage, at the cost of possibly not filling at all. In a deeply liquid contract the spread is so tight that a market order is usually fine. In a thin contract a careless market order is how beginners hand free money to the market.

A market order in a thin book is the classic beginner trap. You think you are buying at the price on the screen, but your order chews through several depth levels and fills far worse. Never fire a market order into an illiquid contract without checking the depth first. When in doubt, use a limit order and accept that you might not fill.

The India rule, live in the near month

Now the practical part, the rule that keeps a beginner out of most spread and slippage trouble in the Indian market. Liquidity is not spread evenly across contracts. It is heavily concentrated, and you want to trade where it pools.

The near-month NIFTY and BANKNIFTY index futures are among the most liquid instruments in the country. Their spreads are routinely just a tick or two, their depth ladders are stacked with size, and you can enter and exit meaningful positions with barely any slippage. This is the deep end of the pool, and it is exactly where a beginner should swim.

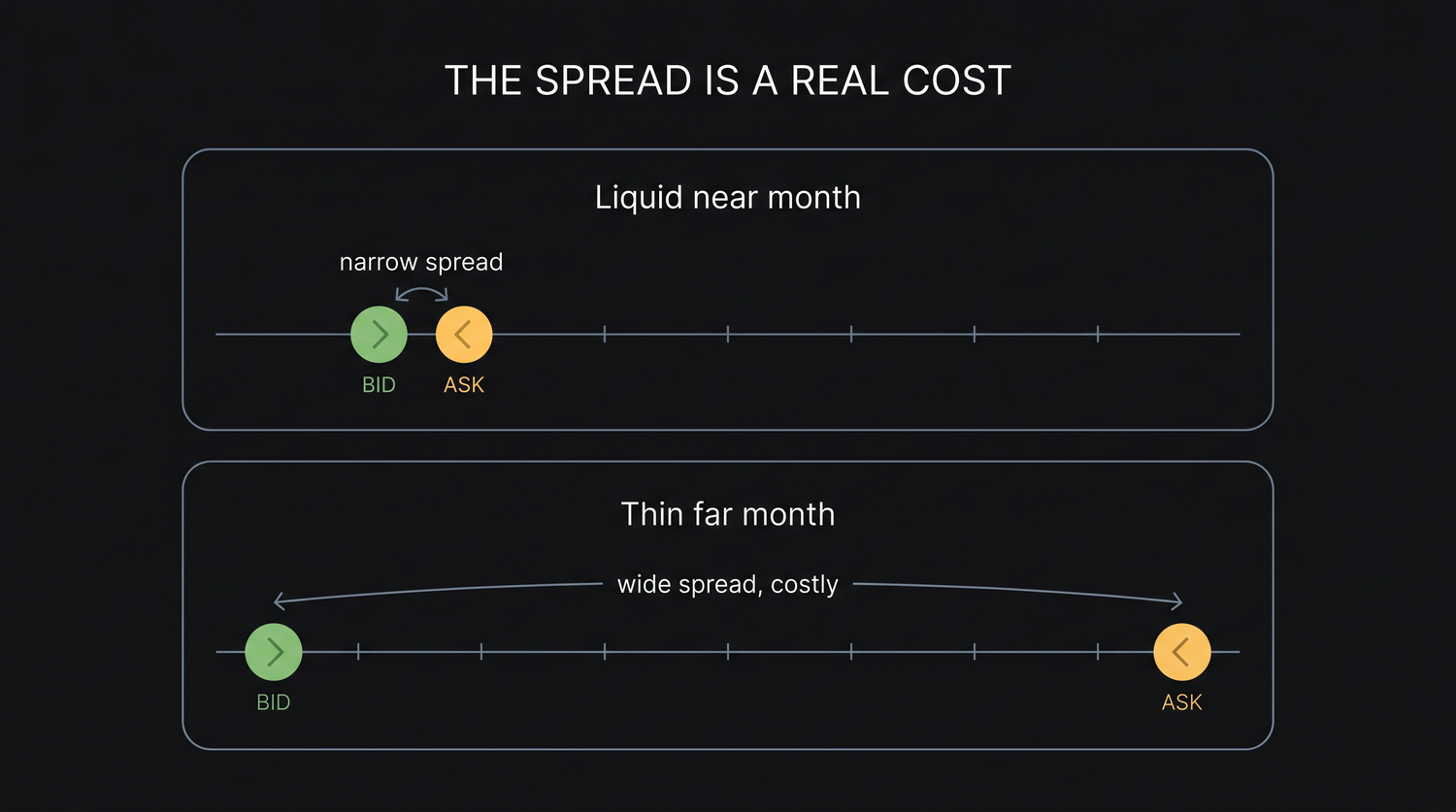

Wander away from it and the water gets dangerous fast. Far-month contracts, the ones expiring two or three months out, are thinly traded even on popular underlyings, with wide spreads and sparse depth. Small single-stock futures, the less famous names, can be thin and punishing too, with spreads of several ticks and almost nothing resting at each level. The same RELIANCE future that trades cleanly in the near month can be uncomfortably illiquid in a far month.

Liquidity in Indian futures concentrates in the near-month index contracts and the most active single-stock names. The near month carries the volume and the tightest prices. Far months and small stock futures are where spreads widen and slippage bites. A beginner who stays in the liquid near month avoids most of this cost without doing anything clever.

So the discipline is simple. Trade the near month. Favour the deeply liquid index futures while you are learning. And before you send any market order, take the two-second habit of reading the depth ladder to confirm there is real size waiting near the touch. Liquidity is the invisible floor under every trade you place. When it is solid you barely notice it. When it is missing, the spread and the slippage take a bite out of you on the way in and another on the way out, long before you have been right or wrong about the direction.