Margin and Leverage: The Double-Edged Sword

You do not pay the full contract value, only a margin. That is leverage, and it multiplies both gains and losses. Learn how margin works and why leverage is the single most important risk in futures.

- ·What margin is

- ·How leverage multiplies P&L

- ·Initial vs maintenance margin

- ·The margin call

- ·A worked leverage example

- ·Why leverage cuts both ways

Here is the fact that pulls most people toward futures, and the same fact that ruins many of them. To control one lot of RELIANCE, worth about Rs 6,59,000 of stock, you do not need Rs 6,59,000. You need only a fraction of it, perhaps a little over a lakh, set aside as a deposit. With roughly a sixth of the money you command the full position. That sounds like a gift, and used carefully it is a powerful tool. Used carelessly it is the fastest way a beginner has ever found to lose more than they meant to. This chapter explains the deposit, the magic multiplier it creates, and the honest cost of getting it wrong.

Margin, the deposit you actually post

When you trade a future, you do not pay the full contract value. You post a margin, a good-faith deposit that the exchange holds to cover potential losses on your position. The margin is a fraction of the contract value, and for index and large-stock futures it is often roughly 15 to 20 percent, though the exact figure changes with how volatile the underlying is. A jumpier stock demands a fatter margin.

Let us put real numbers on the RELIANCE contract. The contract value is about Rs 6,59,000, being 500 shares near Rs 1,318. A margin in the region of 15 to 20 percent of that works out to roughly Rs 1,00,000 to Rs 1,30,000. So with somewhere around Rs 1,10,000 of your own money tied up as margin, you control the full Rs 6,59,000 of RELIANCE exposure. You have not borrowed the rest in any visible loan. The structure of the contract simply lets a small deposit support a large position.

Margin is a deposit, not a payment. You post roughly Rs 1,00,000 to Rs 1,30,000 to control about Rs 6,59,000 of RELIANCE. The remaining exposure is carried by the contract itself, which is exactly why your gains and losses are calculated on the full value, not on the deposit.

Where the margin number comes from, SPAN plus exposure

You do not have to guess the figure. The exchange calculates the margin for every contract using a defined risk model, and it always arrives in two parts that travel together.

- SPAN margin is the core of it. SPAN is the exchange's risk system, and this margin is the amount it judges necessary to cover a worst-case one-day move in your position. It is the larger of the two parts, and it climbs when the underlying turns more volatile.

- Exposure margin is an extra buffer the exchange adds on top of SPAN, a second cushion against an unusually violent move. It is smaller than SPAN, but it is not optional.

Add the two together and you have the total margin required, the actual deposit that must sit free in your account before the trade will go through. For our one RELIANCE lot that total lands in the region of Rs 1,10,000 to Rs 1,30,000, the bulk of it SPAN with a thinner slice of exposure.

Because the exact number shifts every day with volatility, you should never estimate it by hand when real money is at stake. OpenAlgo includes a margin calculator for exactly this. You give it the contract, the side you want to take and the quantity, and it returns three numbers straight back: the SPAN margin, the exposure margin, and the total margin required. Checking it before you place an order means the deposit is never a surprise, and you can see at once whether the position fits the capital you actually have.

Make the margin calculator the step before every futures order. Enter the contract and quantity, read off the total margin required, and confirm it sits comfortably inside your free funds with room to spare for the daily losses we meet in the next chapter. A position you cannot fund through a rough patch is one you should size down before you ever place it.

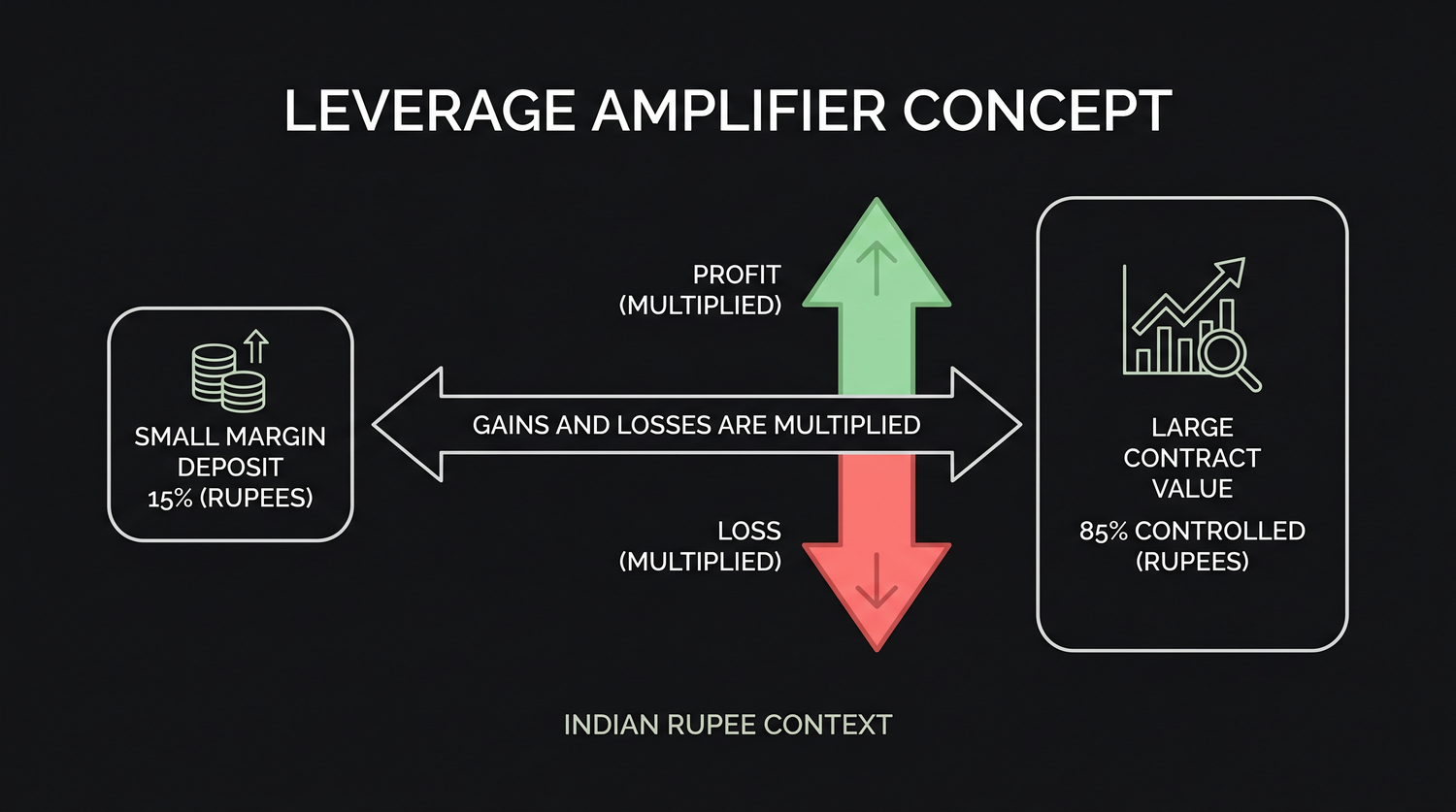

Leverage, the multiplier hiding in the deposit

That gap between the small deposit and the large exposure has a name, and it is the most important word in this entire course. It is leverage. Leverage is the ratio between the value you control and the money you put up. Controlling Rs 6,59,000 with about Rs 1,10,000 is close to six times leverage. Every rupee of your capital is doing the work of roughly six.

Leverage does something specific and unforgiving to your returns. It calculates your profit and loss on the full contract value while measuring it against your small margin. This is where a modest move in the stock becomes a dramatic move in your account.

Work it through. Suppose RELIANCE rises 5 percent, from about Rs 1,318 to about Rs 1,384, while you are long one future. The exposure is Rs 6,59,000, so a 5 percent gain on that is about Rs 33,000. But you only posted around Rs 1,10,000 of margin. A profit of Rs 33,000 on Rs 1,10,000 is roughly a 30 percent gain on your money. The stock moved 5 percent. Your capital moved about 30 percent. That six-times multiplier is leverage doing its work.

Now read that example again with one word changed, because the multiplier has no loyalty. Suppose RELIANCE falls 5 percent instead, to about Rs 1,252. The loss on the Rs 6,59,000 exposure is again about Rs 33,000, and against your Rs 1,10,000 margin that is roughly a 30 percent loss of your capital. The stock dipped a mild 5 percent. You lost almost a third of the money you committed. Leverage multiplies losses by exactly the same multiple it multiplies gains. It is genuinely double-edged, and the two edges are the same length.

Leverage is symmetric and it does not care which way the price goes. The same roughly six-times multiplier that turns a 5 percent rise into a 30 percent gain turns a 5 percent fall into a 30 percent loss. A move that looks small on the stock chart can be enormous on your margin.

Here is the same idea in a compact table, showing one RELIANCE lot with about Rs 1,10,000 of margin against the full Rs 6,59,000 exposure.

| Move in RELIANCE | Change in exposure value | Effect on your margin |

|---|---|---|

| up 2 percent | about Rs 13,000 gain | about 12 percent gain |

| up 5 percent | about Rs 33,000 gain | about 30 percent gain |

| down 2 percent | about Rs 13,000 loss | about 12 percent loss |

| down 5 percent | about Rs 33,000 loss | about 30 percent loss |

| down 17 percent | about Rs 1,10,000 loss | your entire margin gone |

That last row deserves a long pause. A fall of around 17 percent in RELIANCE, which is a bad but entirely possible month for any stock, would wipe out your whole deposit. The stock is still worth most of its value. Your account is at zero. This is the reality of leverage stated without flattery.

Initial margin and maintenance margin

There are two margin figures a trader must know, and they do different jobs.

- Initial margin is the amount you must post to open the position in the first place. It is the roughly Rs 1,00,000 to Rs 1,30,000 we have been using for one RELIANCE lot. No initial margin, no trade.

- Maintenance margin is the lower threshold your account must stay above while the position is open. As your position loses money day by day, your usable margin shrinks. The maintenance level is the line the exchange will not let you fall below.

The reason there are two levels is that futures are settled every single day, a process called mark-to-market that gets its own chapter next. Each day's loss is actually debited from your margin account, so the cash backing your position really does fall as the trade goes against you. The maintenance margin is the safety floor that keeps enough deposit in place to cover the exchange against your default.

Initial margin gets you in the door. Maintenance margin keeps you in the room. Because losses are settled daily and pulled straight from your deposit, your margin balance is a living number that falls in real time as a trade moves against you.

The margin call

When daily losses drag your margin balance below the maintenance level, you receive a margin call. A margin call is a demand to top up your account back to the required level, usually quickly. It is the market's way of saying your deposit is no longer big enough to back the risk you are carrying.

You have two choices when the call arrives, and only two. You can add fresh funds to restore the margin, or you can reduce or close the position so that less margin is required. If you do neither in time, your broker is entitled to close the position for you, at whatever price the market offers, to protect itself and the exchange. That forced exit often lands at the worst possible moment, locking in a loss right when the market is most violent against you.

A margin call is not a polite reminder, it is a deadline. Ignore it and your position can be closed for you at a bad price, turning a paper loss into a permanent one. Many blown accounts trace back to a single ignored margin call during a sharp move.

Respecting the double-edged sword

None of this means leverage is evil. It is a tool, and a remarkable one, that lets a trader with modest capital take a meaningful position. The danger is never the tool itself. The danger is using more of it than you can survive. A trader who treats one RELIANCE lot as if it were a Rs 1,10,000 bet is fooling themselves. It is a Rs 6,59,000 position, and it will move like one.

The honest framing, the one that keeps traders alive long enough to get good, is to size your position by the full exposure and the loss you could take, never by the small margin that gets you in. We devote a whole later chapter to surviving leverage, but the seed is planted here.

Before risking real capital, open a leveraged position in sandbox trading (analyzer mode in OpenAlgo) and watch your margin move as the price swings. Seeing a 5 percent stock move become a 30 percent swing on your deposit, with no money at stake, teaches the lesson far more cheaply than the market will.

The takeaway is one sentence you should carry into every future you ever trade. Margin is what you post, leverage is what you control, and the multiplier rewards you and punishes you in exactly equal measure. Honour that symmetry and futures become a serious instrument in your hands. Forget it, and the same instrument will remind you, on a day of its choosing, that you were always risking the full Rs 6,59,000 and not the comfortable deposit you imagined. In the next chapter we see precisely how those daily gains and losses hit your account, through the mechanism called mark-to-market.