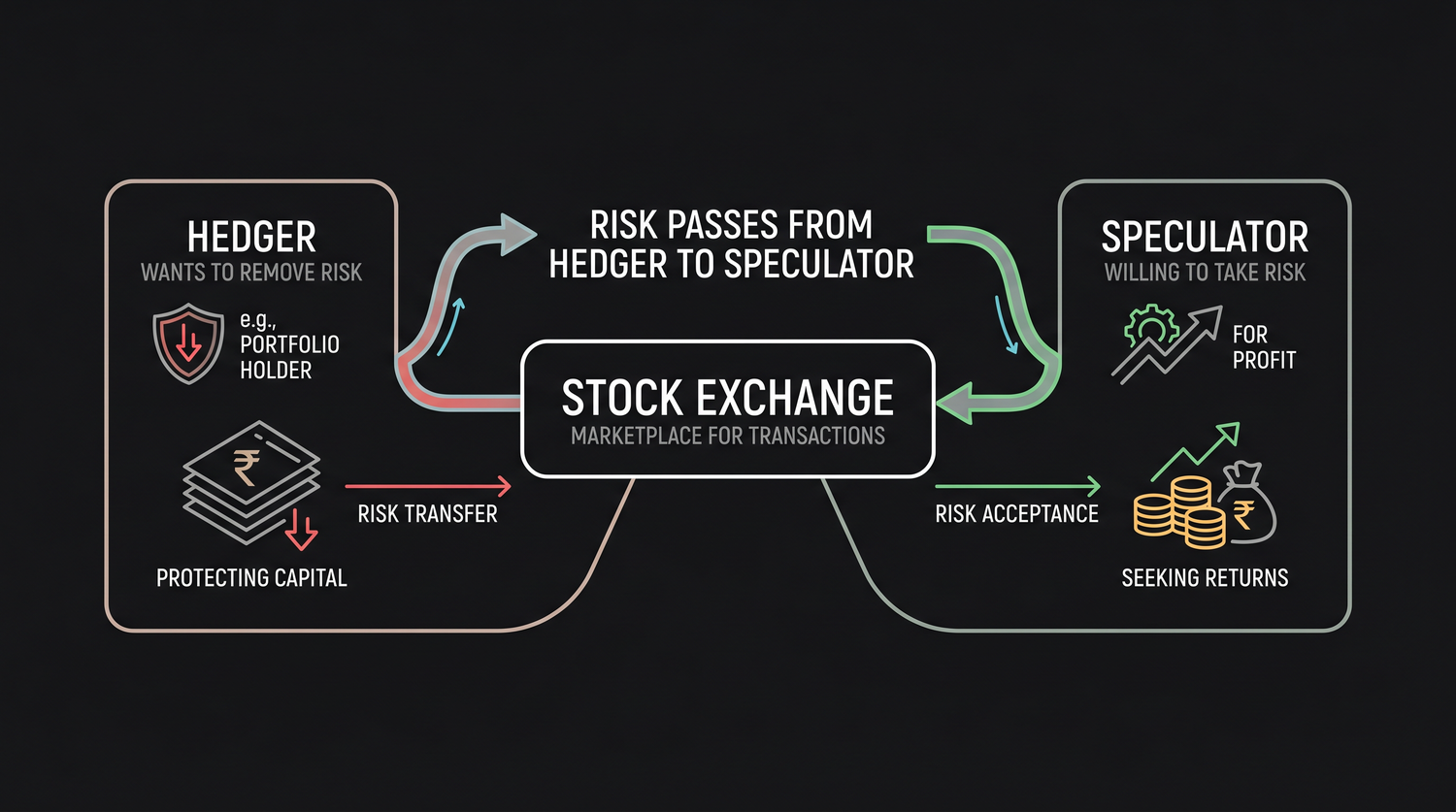

Why Futures Exist: Hedgers and Speculators

Futures were not invented for gambling. Meet the two crowds that meet in the futures market, the hedger who wants to remove risk and the speculator who is happy to take it on.

- ·The original purpose of futures

- ·Hedgers who offload risk

- ·Speculators who take it on

- ·How the two sides need each other

- ·Liquidity and price discovery

- ·A farmer-and-mill example

It is tempting to think futures markets were dreamed up as a casino for traders who like a thrill. They were not. Futures were born out of a very practical problem that ordinary producers and buyers faced long before screens and trading apps existed. A farmer who plants a crop in spring has no idea what price it will fetch at harvest. A mill that needs that crop has no idea what it will cost. Both of them are exposed to a swing they cannot control, and both would happily trade away that uncertainty for a known, fixed price. The futures market exists to let them do exactly that, and once you understand the two characters who meet there, the whole purpose of the market clicks into place.

The hedger wants to get rid of a risk

A hedger is someone who already carries a risk and wants it gone. The risk is not something they went looking for. It comes attached to their real business or their real portfolio, and it keeps them awake at night.

Picture a fund manager in Mumbai who holds a large basket of Indian shares for clients. The portfolio is healthy, but the manager reads the news and worries the market could fall sharply over the next month because of an upcoming event. Selling the entire portfolio would be expensive, slow, and would trigger tax and transaction costs. The manager does not want to sell. The manager wants protection, a way to soften the blow if the market drops, without dismantling everything that has been carefully built.

This is the hedger's situation in a sentence. They own something, they fear a move against it, and they want to offset that fear. They are not trying to get rich on the futures trade. They are trying to stay calm. For a hedger, a futures position that loses a little when the market rises is perfectly acceptable, because in that happy case their real holdings are gaining anyway. The future is insurance, not a profit engine.

A hedger already carries a risk from their real holdings or business. They use futures to transfer that risk away, accepting a known cost in exchange for peace of mind, not to chase profit.

The speculator is willing to take that risk on

Now meet the other character. A speculator does not own the underlying business worry. They have no crop to protect and no portfolio that keeps them up at night. What they have is a view on where the price is going and a willingness to put capital behind that view. The speculator is happy to take on the very risk the hedger is desperate to shed, because risk is where the chance of profit lives.

A speculator who believes RELIANCE will rise over the coming month can buy a RELIANCE future at Rs 1,320 for the 28 July 2026 expiry. They are deliberately accepting price risk on 500 shares, about Rs 6,59,000 of exposure, in the hope of a gain. If they are right and the stock climbs, they profit. If they are wrong, they lose, and because futures are leveraged, that loss can be severe. We will be blunt about this throughout the course. Most speculators do not win over time, and leverage is usually the reason.

Speculation is not a flaw in the market, it is a necessary role, but it is genuinely risky. A speculator takes on price risk on purpose, and the majority of leveraged speculators lose money over the long run. Respect that from the very start.

The two sides need each other

Here is the elegant part. The hedger wants to pass a risk away. The speculator wants to take a risk on. They are a perfect match, and the futures contract is the handshake between them. When the worried fund manager sells index futures to protect a portfolio, somebody has to be on the other side buying those futures. Often that somebody is a speculator betting the market will hold up or rise. The risk does not vanish. It simply moves from the shoulders of the person who did not want it to the shoulders of the person who chose it.

This transfer is the deep reason futures exist. It is not that one side is clever and the other is foolish. They simply want opposite things, and the market lets them swap. Think of it like insurance. You pay an insurer to take on the risk of your house burning down. You are the hedger, glad to be rid of the worry. The insurer is the speculator, accepting many such risks because, priced correctly, the business is profitable over time. Neither party is being tricked. Both get what they came for.

It helps to lay the two roles side by side, because the same RELIANCE contract can serve either one depending entirely on the trader's motive.

| Question | The hedger | The speculator |

|---|---|---|

| Do they already own the risk? | Yes, from real holdings | No, they seek it out |

| What do they want? | To remove uncertainty | A chance at profit |

| What is the future to them? | Insurance against a move | A bet on a move |

| Are they happy to lose a little? | Yes, if their holdings gain | No, a loss is a loss |

| Typical Indian example | A fund protecting a portfolio | A trader backing a view on RELIANCE |

The two columns are opposites, and that is precisely why a deal can happen. If both traders wanted the same thing, there would be nobody to take the other side. The market clears because their goals point in different directions.

A fund manager fears a one-month dip and sells NIFTY futures to protect a portfolio. A trader who expects the market to climb buys those same futures. If the market falls, the manager's futures gain and cushion the portfolio loss, while the trader takes the hit. If the market rises, the trader profits and the manager gives back a little of their gain as the cost of the insurance. Each side knew the deal going in.

Liquidity and price discovery, the quiet gifts

When hedgers and speculators show up in large numbers, two valuable things appear almost as a side effect, and both make the market better for everyone, including beginners.

The first is liquidity. Liquidity means you can buy or sell quickly without moving the price much, because there are always plenty of willing traders on the other side. A market full of only hedgers would be lopsided and thin, with everyone wanting to sell protection at the same nervous moment. Speculators fill the gaps and stand ready to trade, so orders get matched smoothly. For you, liquidity shows up as tight prices and the comfort of knowing you can square off a position when you need to.

The second gift is price discovery. Because so many informed participants are constantly buying and selling based on everything they know and expect, the futures price becomes a continuously updated, collective best guess about the future. When you look at where the RELIANCE future is trading, you are reading the combined opinion of thousands of hedgers and speculators about where the stock is heading. That single number carries an enormous amount of information, and it is freely available to anyone watching the market.

The futures price is often where new information shows up first. Because futures are quick to trade and leveraged, traders frequently act on news there before the cash market fully reacts, which is why analysts watch index futures so closely.

Where you fit in

As you learn, you will likely begin life as a small speculator, taking a view and accepting risk for the chance of a gain. There is nothing wrong with that, provided you are honest about the odds and ruthless about controlling your losses. Later in the course you will see how the same instrument can be used the hedger's way, to protect something you already own rather than to gamble on direction. The remarkable thing about futures is that the very same RELIANCE contract can be a tool of caution in one trader's hands and a tool of aggression in another's. The contract does not care. Your intent and your risk control are what decide whether the instrument serves you or sinks you.

Before you risk real money, practise both roles in sandbox trading (analyzer mode in OpenAlgo). Place a speculative long in RELIANCE futures, then try a protective short against a holding, and watch how differently the two feel even though the contract is identical.

The takeaway is simple and worth carrying into every chapter that follows. Futures are not a game invented for gamblers. They are a marketplace where one person's unwanted risk becomes another person's chosen opportunity. The hedger sleeps better. The speculator gets a shot at profit. And the rest of us get liquid markets and honest prices as the reward for letting these two strangers meet. In the next chapter we open the contract itself and read its specifications line by line, so you know exactly what you are agreeing to before you ever click buy.