The Risks of Leverage (and How to Survive)

Most futures traders lose, and leverage is usually why. Learn the honest risks, the margin-call spiral and the overnight move, and the discipline that keeps a trader in the game.

- ·Why most futures traders lose

- ·The margin-call spiral

- ·Treating margin as max loss, a trap

- ·Confusing notional with capital

- ·Respecting the leverage

- ·The survivor's mindset

Here is the sentence the rest of this course has been building toward, and it is not a comfortable one. Most people who trade leveraged futures lose money. Not some. Most. Study after study of retail derivatives traders, in India and elsewhere, finds that the large majority end a year poorer than they started, and a painful share of them lose heavily. This is not because they are stupid or lazy. Many are clever, hardworking people. They lose because of the single feature that drew them in: leverage. The same multiplier that makes a small move into a big gain makes a small move into a big loss, and it does so faster than most beginners can react. This chapter is the honest one. Its job is not to scare you away from futures but to show you exactly how leverage destroys accounts, and how the disciplined few survive.

If you remember nothing else, remember this. The instrument is not the danger. The leverage is the danger, and how you size and control it decides whether you last.

Why most futures traders lose

Leverage is seductive because it works on the way up. Recall the RELIANCE example that has run through this course. The stock trades around Rs 1,318, one lot is 500 shares, so a single future controls about Rs 6,59,000 of stock, yet you post a margin of only roughly Rs 1,00,000 to Rs 1,30,000. That is leverage of about five to six times. A modest five percent rise in RELIANCE, from 1318 to about 1384, is 66 points, which on 500 shares is Rs 33,000. Against a margin near Rs 1,10,000 that is a return close to thirty percent on your money from a five percent move in the stock. Intoxicating.

Now run it the other way, because the market is just as happy to. A five percent fall in RELIANCE is the same 66 points, the same Rs 33,000, but now it is a loss, and it is close to thirty percent of your margin gone from a five percent move against you. Leverage is perfectly even-handed. It multiplies losses exactly as much as gains. The reason most traders lose is not that the multiplier is unfair, it is that human beings size positions for the dream of the gain and are then unprepared for the identical loss, and a few of those losses, taken too large, wipe out many small wins.

Leverage multiplies losses exactly as much as gains. Most futures traders lose not because the odds are rigged but because they size for the upside and are destroyed by the equally large downside.

The gap and the risk while you sleep

A share you own outright can fall, but you can watch it and sell. A leveraged future carries a sharper version of an old danger: the overnight gap. Markets close, but the world does not. News breaks at night, a result disappoints, a global market crashes, and when trading reopens the price does not move smoothly from yesterday's close. It gaps, opening sharply away from where you last saw it, with no chance to trade in the gap.

For a leveraged position this is brutal. Your carefully placed stop loss, the level where you meant to get out, is simply skipped over. The price opens below it, you are filled far worse, and because you control Rs 6,59,000 with a margin near Rs 1,10,000, a gap that would be a manageable bruise on a cash holding can be a serious wound on the future. A single bad overnight gap can cost a large slice of your margin before you have even had your morning tea.

A stop loss does not protect you against an overnight gap. The market can leap straight past your exit while you sleep, and leverage turns that leap into a heavy loss. Never carry more overnight futures risk than you could survive seeing gap against you at the open.

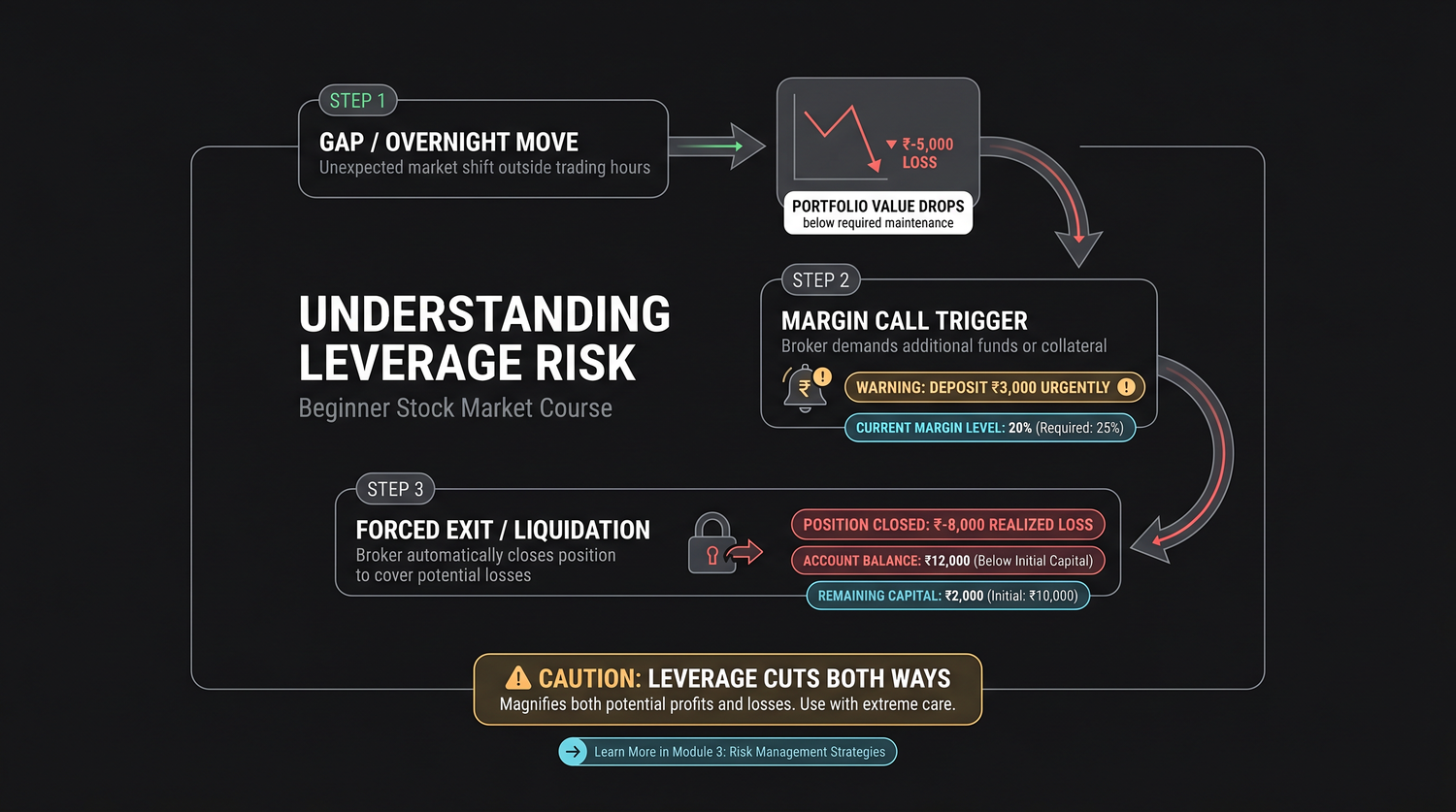

The margin-call spiral

This is where leverage turns from painful to ruinous, and it deserves a clear picture. When a loss eats into your margin, your account can fall below the minimum the exchange requires to hold the position. Your broker then issues a margin call, a demand to add more funds or reduce the position. If you cannot or do not act in time, the position is forcibly closed at the prevailing price, locking in the loss whether you like it or not.

The cruelty is in the sequence, and it feeds on itself.

- The market moves against your leveraged position, and the loss is magnified.

- Your margin drops below the required level, triggering a margin call.

- You must add money or cut the position, often at the worst possible moment.

- If you cannot, the position is force-closed at a bad price, crystallising the loss.

- The loss shrinks your capital, so the next position is sized from a smaller base, and one more bad trade can finish the account.

Notice that the forced exit usually lands at the worst time, when the price has already run hard against you, often the very moment before a bounce. The spiral does not care about your conviction. It is mechanical. Once leverage and a margin shortfall take over, the decision to exit is made for you, at a price you did not choose.

A trader holds one RELIANCE long with a margin near Rs 1,10,000. Bad news gaps the stock down 8 percent overnight, a loss of about Rs 52,000, nearly half the margin. The account falls below the required level, a margin call lands, the trader cannot add funds fast enough, and the position is force-closed at the lows, just before a partial recovery the trader never gets to enjoy.

Position sizing: the one habit that decides survival

Now the survival side, because plenty of people do trade futures for years without blowing up. They share one habit above all: they risk only a small fraction of their capital on any single trade. The common rule of thumb is to risk no more than one to two percent of your trading capital on a trade, meaning the distance from your entry to your stop, multiplied by the lot, should cost you no more than that small slice if the stop is hit.

Work it through. Suppose your trading capital is Rs 5,00,000 and you cap risk at two percent, which is Rs 10,000 per trade. On a RELIANCE future of 500 shares, Rs 10,000 of risk is just 20 points of room, because 20 times 500 is Rs 10,000. So if your analysis says the stop belongs 20 points away, one lot fits your risk. If the chart says the sensible stop is 40 points away, then one lot would risk Rs 20,000, double your limit, so the disciplined choice is to not take a full lot, or to wait for a setup with a tighter stop. Position size is dictated by your risk limit and your stop distance, never by how confident you feel.

This is the quiet maths that separates survivors from casualties. The survivor sizes so that being wrong costs a small, recoverable amount. The casualty sizes for the reward, takes a position far too large for the account, and needs only one bad gap to be finished.

Decide your stop first, then size the position so that hitting the stop costs only a small fixed fraction of your capital, around one to two percent. Let the stop distance choose your size. Never let your confidence or the lure of a big win choose it for you.

Always trade with a stop

A stop loss is the price at which you have decided, in advance and calmly, to admit the trade is wrong and get out. With leverage, trading without a stop is not bravery, it is a slow way to hand over your account. A move that is merely uncomfortable on a cash holding can be account-threatening on a future, so you must know your exit before you enter, not invent one in the panic of a fast loss.

A stop is not perfect. As you saw, an overnight gap can leap past it. But on a normal intraday move it does exactly its job, capping the loss near where you planned and keeping any single trade from becoming the one that ends you. Combine a pre-decided stop with small position sizing and you have the two habits that, more than any indicator or system, keep a trader alive long enough to learn.

A stop loss will not save you from every gap, but it caps the ordinary losses that make up most trades. Entering a leveraged future with no planned exit is the fastest route to the margin-call spiral. Know your exit before you enter, every single time.

Respect the leverage, and a sober closing word

Step back and the whole picture is simple, even if it is not easy. Futures are a sharp tool. Used with respect they let you trade in both directions, hedge what you own, and put capital to work efficiently. Used without respect they are the quickest way the market has to take money from a beginner, and the lever that does it is leverage.

So hold these few truths close as you finish this course:

- Most leveraged futures traders lose, and oversized positions are usually the reason.

- Leverage multiplies losses exactly as much as gains, with no favouritism.

- An overnight gap can skip your stop, so never carry more risk than you can survive at the open.

- The margin-call spiral is mechanical and unforgiving once it starts, so stay far from its edge.

- Risk a small, fixed fraction of your capital per trade, let your stop choose your size, and always know your exit.

If you want to rehearse all of this without real money at stake, practise in sandbox trading, the analyzer mode in OpenAlgo, until the discipline is second nature. The traders who survive are rarely the boldest. They are the ones who treated leverage as the defining danger of the instrument, sized small enough to be wrong many times, and lived to trade another day. Be one of those.