Settlement: Stock Delivery vs Index Cash

What happens at expiry depends on what you traded. Learn that stock futures are physically settled (an open position can become an actual delivery obligation, with short-delivery risk), while index futures settle in cash, and why a beginner should square off stock futures before expiry.

- ·Physical settlement of stock futures

- ·The delivery obligation at expiry

- ·Short delivery and its penalty

- ·Cash settlement of index futures

- ·The final settlement price

- ·Squaring off before expiry

Imagine you bought one lot of the RELIANCE future as a quick leveraged bet. You put up a margin of roughly a lakh, you were sure the stock would rise, and then life got busy and you simply forgot about the position. The last Tuesday of the month arrives, the contract expires, and a few days later your broker is asking you for the full value of 500 RELIANCE shares, about six and a half lakh in cash, because you are now obliged to actually take delivery of the stock. That is not a glitch. That is exactly how a single-stock future is designed to settle, and it is the single nastiest surprise that catches small traders who never read this far.

This chapter is about one sharp dividing line in the futures world. When a contract expires and is not closed beforehand, how does it actually finish? For a stock future like RELIANCE the answer is physical delivery of shares. For an index future like NIFTY or BANKNIFTY the answer is a plain cash difference. The two could not be more different in what they demand from you, and knowing which is which is the difference between a clean exit and an expensive accident.

Two ways a contract can finish

Every futures contract has a settlement method baked into it long before you ever trade it. You do not choose it. The exchange fixes it for the whole class of contract. There are only two methods, and the entire chapter rests on telling them apart.

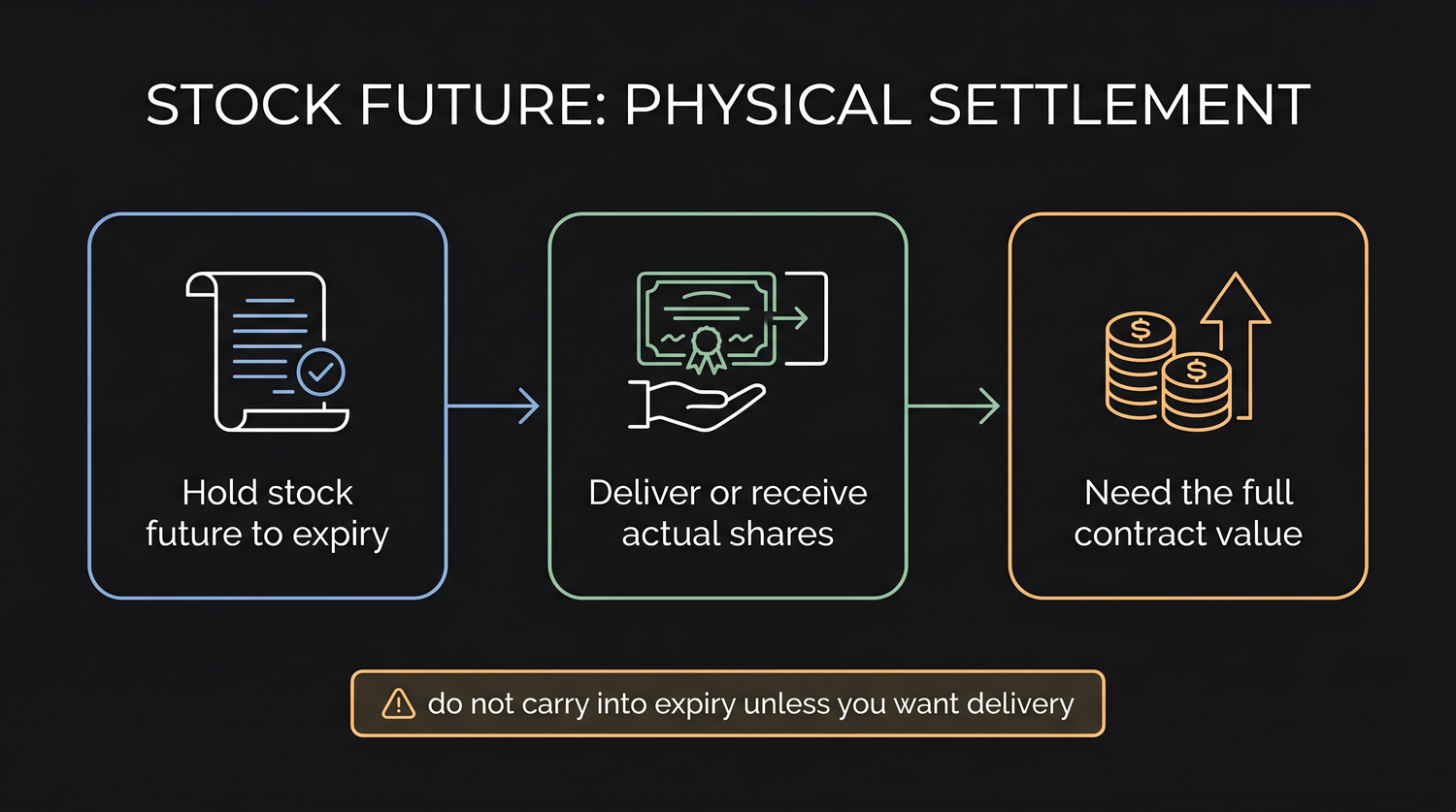

- Physical settlement means real assets change hands at expiry. The buyer pays the full contract value in cash and receives the underlying shares into their demat account. The seller delivers the actual shares and receives the full cash value. Nothing is netted to a difference. The deal completes for real.

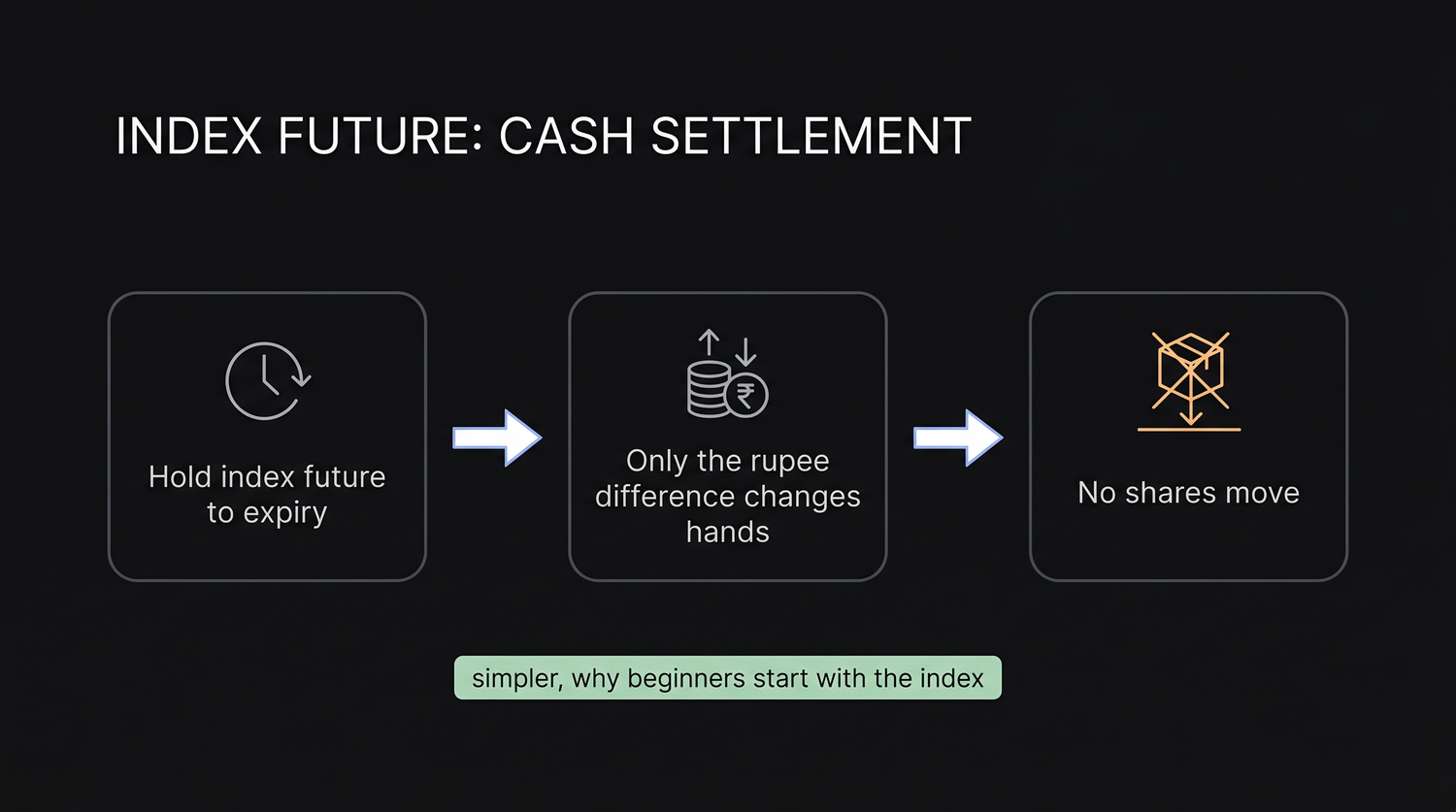

- Cash settlement means nobody delivers anything. At expiry only the rupee difference between your entry price and the final settlement price is credited or debited. No shares move, no full value is needed, the position just dissolves into a single profit or loss number.

In India the rule is clean and worth memorising. All single-stock futures settle physically. All index futures settle in cash. RELIANCE, being a single stock, is physically settled. NIFTY and BANKNIFTY, being indices, are cash settled. There is no in-between and there is no opting out once a contract reaches its final day.

A stock future settles by physical delivery of shares. An index future settles in cash, as a pure difference. The settlement method is fixed by the exchange for the whole contract class, not chosen by you.

Two different settlements happen here, and it is worth keeping them apart. Your daily mark-to-market profit or loss is a funds settlement, always paid in cash. The final settlement at expiry is the one that differs by product: an index future finishes purely in cash, while a single-stock future carried to expiry finishes by the physical delivery of securities, the shares moving between the two demat accounts. The generic NSE Clearing settlement-mechanism page describes that cash funds-settlement of profit and loss, which is a separate step from the share delivery, so do not read its cash wording as meaning a stock future avoids delivery. The authoritative confirmation that single-stock derivatives are physically settled is the NSE equity-derivatives contract specification and the NSE Clearing settlement schedule (its STT schedule lists them as physically settled stock derivatives). These rules are set by the exchange and the regulator and have changed before, so confirm the current treatment there before any expiry.

Single-stock futures: delivery is real

Let us be concrete with the numbers you already know. RELIANCE trades near Rs 1,318 and one lot is 500 shares, so one lot controls about Rs 6,59,000 of stock. To open that position you posted only a margin, perhaps Rs 1,00,000 to Rs 1,30,000, which is the whole appeal of futures. Leverage let a small amount of cash control a large amount of stock.

Here is the catch that leverage hides. If you hold that long RELIANCE future all the way into expiry, the contract does not quietly pay you a difference and walk away. It converts into an obligation to buy 500 actual RELIANCE shares at the contract price. You must now produce the full Rs 6,59,000 in cash, not the small margin, because you are genuinely purchasing the shares and they will land in your demat account.

The seller faces the mirror image. A trader who was short the RELIANCE future into expiry is now obliged to deliver 500 real RELIANCE shares. If those shares are not sitting in their demat account, the position cannot be settled cleanly. The exchange has to buy the shares on their behalf through an auction, and the costs and penalties of that fall on the seller. Short selling a stock future and forgetting about it is, if anything, even more dangerous than the long side.

Sit with what this means for a small trader. You wanted a leveraged directional bet, a few days of exposure to a stock you had a view on. You never intended to become a long-term shareholder, and you certainly did not set aside six and a half lakh to buy the stock outright. Yet by simply doing nothing and letting expiry arrive, you can be dragged into a full delivery you cannot comfortably fund. Being forced to find the full value, or being penalised for shares you cannot deliver, turns a small speculative position into a large and expensive problem.

A single RELIANCE lot is about Rs 6,59,000 of stock. If you carry the long future into expiry, that is the cash you must produce to take delivery, not the roughly one lakh margin you started with. Carry the short future in and you must hand over 500 real shares. Either way, doing nothing is a decision with a heavy bill attached.

The margin ramp that forces your hand

The exchange knows perfectly well that most futures traders never meant to deliver anything. To stop a flood of accidental deliveries and defaults, it does not wait quietly for expiry. It deliberately makes holding a stock future into the final days more and more expensive, so that you are pushed to make a conscious choice.

This is the physical-settlement margin spike. In the days leading up to expiry, the margin required to hold a deliverable stock future is ramped up in stages. As the final Tuesday approaches, the exchange progressively adds delivery margin on top of your normal margin, climbing toward the full settlement obligation for anyone still holding near the end. A position that felt comfortable a week earlier suddenly demands far more cash just to keep it open through expiry week.

The intent is honest and protective. The rising margin is the exchange tapping you on the shoulder and saying, decide now. Either commit the real money and the intent to deliver, or close the position and step aside. It deliberately removes the option of drifting carelessly into a delivery you cannot honour. For a beginner the practical effect is simple. If you find your margin requirement jumping sharply as expiry nears, that is the system telling you a stock future is about to become real, and it is your cue to act rather than wait.

The expiry-week margin ramp on stock futures is not a penalty or a glitch. It is the exchange forcing every holder to choose between funding a real delivery and closing out, so the market does not fill up with traders who cannot settle. Treat a rising margin near expiry as a deadline you are being warned about in advance.

Index futures: only the difference moves

Now cross to the other side of the divide, and feel how much lighter it is. An index is not a thing you can hold. You cannot take delivery of NIFTY, because NIFTY is a calculated number standing for a basket of fifty companies. There are no NIFTY shares to put into a demat account. So physical delivery is simply impossible, and index futures are settled entirely in cash.

Picture one NIFTY future. The lot is 65 and the index is near 24,000, so one lot represents about Rs 15,60,000 of exposure. If you carry that contract to expiry, nothing is delivered and no full value is called for. The exchange looks at your entry price and the final settlement price, takes the rupee difference, multiplies it by the lot of 65, and credits or debits that single amount to your account. If NIFTY settled 100 points above where you bought, you receive 100 times 65, which is Rs 6,500, and the contract is finished. If it settled 100 points lower, that same Rs 6,500 is debited. That is the whole event.

Notice everything that does not happen here. No shares appear in your demat account. You are never asked for the full Rs 15,60,000. There is no auction, no delivery penalty, no obligation beyond the difference you already understood as your profit or loss. Even if you completely forget an index position into expiry, the worst that happens is your normal profit or loss is settled in cash, exactly as if you had closed the trade yourself. The accidental delivery trap that haunts stock futures cannot exist here.

This is one more solid reason a beginner usually starts with the index rather than single stocks. Index futures are deeply liquid, they spare you single-company news shocks, and crucially they remove the entire physical-delivery hazard. There is far less that can go badly wrong by accident.

You can hold a NIFTY future to its very last second and the only thing that can happen is a cash credit or debit of your profit or loss. There is no version of an index future where you wake up owning, or owing, real shares. The instrument is incapable of delivery.

The final settlement price

Both methods, whether shares or cash change hands, are measured against one official number set on expiry day, so it is worth being precise about it. The final settlement price is taken from the underlying on expiry day, the last Tuesday of the cycle on the NSE, which for our running example is 28 July 2026. For an index future such as NIFTY it is the closing value of the index; for a single-stock future such as RELIANCE it is the exchange-defined closing price of the underlying share, a volume-weighted average over the closing window rather than one last tick.

For a cash-settled index future, that closing value is the price your profit or loss is calculated against. For a physically settled stock future, that closing price sets the value at which the shares change hands. As an earlier chapter on the expiry calendar noted, using a closing-window average rather than the last random tick makes the figure robust, so a few orders in the final seconds cannot yank it around. The number that closes out every contract, deliverable or cash, is a fair reflection of where the market genuinely finished.

The blunt rule to carry away

Strip away the detail and the guidance is short, and it is the kind of rule worth following without exception.

Do not carry a single-stock future into expiry unless you genuinely intend to give or take delivery. If you wanted a leveraged bet and nothing more, close the position or roll it to the next month well before the final days, while liquidity is good and the delivery margin has not yet bitten. Treat the last Tuesday of the month as a hard deadline stamped into the contract name from the day you enter, and act before it, not on it.

Index futures let you relax that vigilance, because the worst case is a cash settlement of the profit or loss you already understood. Stock futures do not. The same leverage that made the RELIANCE position attractive is precisely what makes an accidental delivery so painful, because the full value dwarfs the margin you put up. Know which side of the divide your contract sits on, and never let a deliverable stock future drift quietly into the final days. That one habit will spare you the most expensive surprise in all of futures trading.

Mark every stock-future expiry on your own calendar the moment you open the trade, and decide in advance whether you will close, roll, or genuinely take delivery. If you only ever wanted the leveraged bet, the answer is almost always to be out before the physical-settlement week, not in it.