Position Limits, the F&O Ban and Quantity Freeze

The exchange caps how much of a contract anyone can hold. Learn the market-wide position limit, the client and member limits, what tips a stock into the F&O ban period and the rule that you can take no fresh positions while it lasts, and the quantity freeze that forces a large order to be sliced.

- ·Market-wide position limit (MWPL)

- ·Client and member limits

- ·What triggers the F&O ban

- ·No fresh positions in a ban

- ·Quantity freeze and order slicing

- ·Reading the ban list

Picture this. You open your trading screen one morning, decide a popular mid-cap stock looks ready to run, and try to buy a lot of its future. The order bounces straight back, rejected. Your account is fine, your margin is more than enough, and the market is wide open. So what just happened? The stock has entered something called the F&O ban, and while that ban is on, the exchange will not let anyone open a fresh position in it. You are not being singled out. Every trader in the country is looking at the same locked door.

This chapter is about the quiet rulebook sitting behind every futures contract you trade. Most of the time these rules never touch you, which is exactly why beginners forget they exist and then get caught out. There are three you must understand: the market-wide position limit, the F&O ban that follows from it, and the quantity freeze on the size of a single order. None of them is meant to punish you. All of them exist to keep the market from breaking.

Why these limits exist at all

A derivatives market only works while no single player can grow large enough to control a contract. Imagine one very deep-pocketed trader quietly building a position so big that they effectively own most of the open interest in a stock's futures. They could then squeeze everyone else, bending the price to suit themselves while smaller traders on the other side are forced to give in. That is called cornering a market, and it is exactly what position limits are designed to prevent.

There is a second, deeper reason. The clearing house stands behind every futures trade and guarantees it. If positions in one stock were allowed to balloon without limit, a sudden default by one giant player could ripple outward and threaten the whole settlement system. Capping how much can be open at once contains that risk. The limits are a circuit breaker for the market as a whole, not just a referee for individual traders.

Position limits exist for two reasons: to stop any single player from cornering a contract and squeezing everyone else, and to contain the systemic risk of one oversized position defaulting and dragging the clearing system with it.

The market-wide position limit

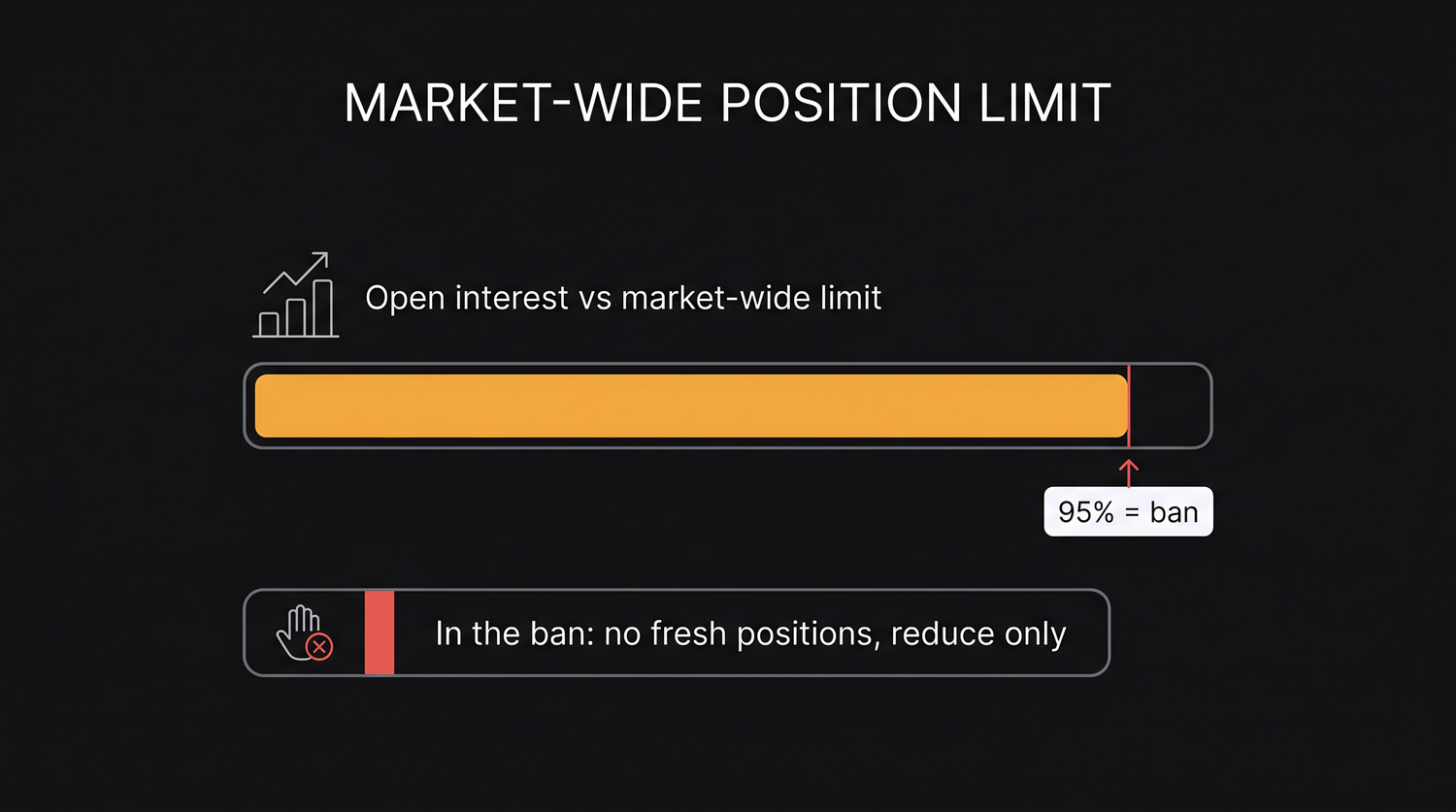

The headline cap is the market-wide position limit, almost always written as MWPL. It is the ceiling on the total number of open positions allowed across every participant in a single stock's derivatives, futures and options combined. Add up everything everyone is holding in that stock, and the sum is not allowed to run past the MWPL.

The cap is not a fixed number plucked from the air. It is tied to the stock's free-float, meaning the shares actually available for public trading, leaving out the blocks held by promoters and other locked-in holders. The MWPL is set as a percentage of that free-float, and the exact percentage is defined by the exchange under the regulator's framework. The thinking is sensible. A stock with a large, freely traded share base can safely support a bigger derivatives market than a small, tightly held one, so the cap scales with the genuine liquidity of the underlying.

Because it is a percentage of free-float, the MWPL is reviewed and revised over time as a company's share base changes. You do not need to calculate it yourself. The exchange publishes the limit for every stock along with its utilisation, and it issues alerts through the session once usage crosses set thresholds. The aggregate open interest itself is disseminated at the end of the day, so treat the intraday alerts, not a live percentage, as your warning that a stock is approaching the ban.

The exact percentages here are set by the exchange and the regulator and have been changed before, so treat the numbers in this chapter as the structure rather than permanent law. Before you rely on a specific figure, confirm the current limit against the NSE position-limits page and the latest market-wide position-limit circulars.

The F&O ban period

Here is where the MWPL stops being an abstract ceiling and starts affecting your screen. As the total open interest in a stock climbs toward its cap, the exchange watches the percentage of the MWPL being used. When that figure crosses a high threshold, around 95 percent of the limit, the stock is pushed into the F&O ban period.

The ban does not freeze the stock entirely. What it bans is fresh positions. While a stock is in the ban list, no trader may open a new long or new short in its futures or options. The only thing you are allowed to do is reduce or square off what you already hold. You can close, you cannot add. The whole market is being told, in effect, that this contract is dangerously full and nobody may pour any more in.

The ban is not permanent. As traders close out and the total open interest falls, the percentage of the MWPL in use drops. Once it eases back below a lower threshold, around 80 percent, normal trading resumes and fresh positions are allowed again. The gap between the entry level near 95 percent and the exit level near 80 percent stops a stock from flickering in and out of the ban every few minutes. It has to clear a real margin of safety before it is let back out.

During an F&O ban you can only reduce or close an existing position in that stock. You cannot open a fresh long or short, and you cannot add to a position you already hold. Never assume you will be able to average into a banned name. If you wanted more, the door is shut until the ban lifts.

There is a knock-on effect worth understanding. Because nobody can open fresh positions in a banned stock, the only trades left are people closing out. That often produces sharp, one-sided unwinding in the future. Traders who are stuck and want out have to sell to other traders who also only want to close, so the price can swing hard on relatively little genuine two-way interest. A banned stock's future can therefore behave erratically, and that thin, closing-only crowd is exactly why a beginner should be extra careful around one.

Reading the daily ban list

The exchange publishes the F&O ban list every trading day. It names the stocks whose open interest has crossed the high threshold and which are therefore restricted to closing trades only. The list is updated around the start of the session, so you can check before you trade whether a stock you are eyeing is currently barred. Reading it takes seconds and saves you the nasty surprise of a rejected order or, worse, finding you are trapped in a name you cannot add to.

Make checking the F&O ban list part of your routine before you trade any single-stock future. If the name is on the list, treat it as a stock you may exit but not enter, and stand aside rather than fight a thin, closing-only market.

Client-level and member-level limits

The MWPL is the limit for the whole market. Underneath it sit two narrower caps that apply to you and to your broker.

- A client-level position limit caps how large any single client can grow in one stock's derivatives. It stops one trader from quietly building a position that, while still under the market-wide ceiling, is large enough to be disruptive on its own.

- A trading-member limit caps how much a single member, your broker as a whole, can hold across all of their clients in that contract. It spreads concentration risk so that no one member becomes a single point of failure.

You will rarely brush against these as a beginner trading a lot or two, because the numbers are large. But they are the reason a very big trader cannot simply keep adding without end, and they work alongside the MWPL to keep any one client or any one member from dominating a contract. The principle is the same at every level. No single point in the system is allowed to get too big.

The quantity freeze

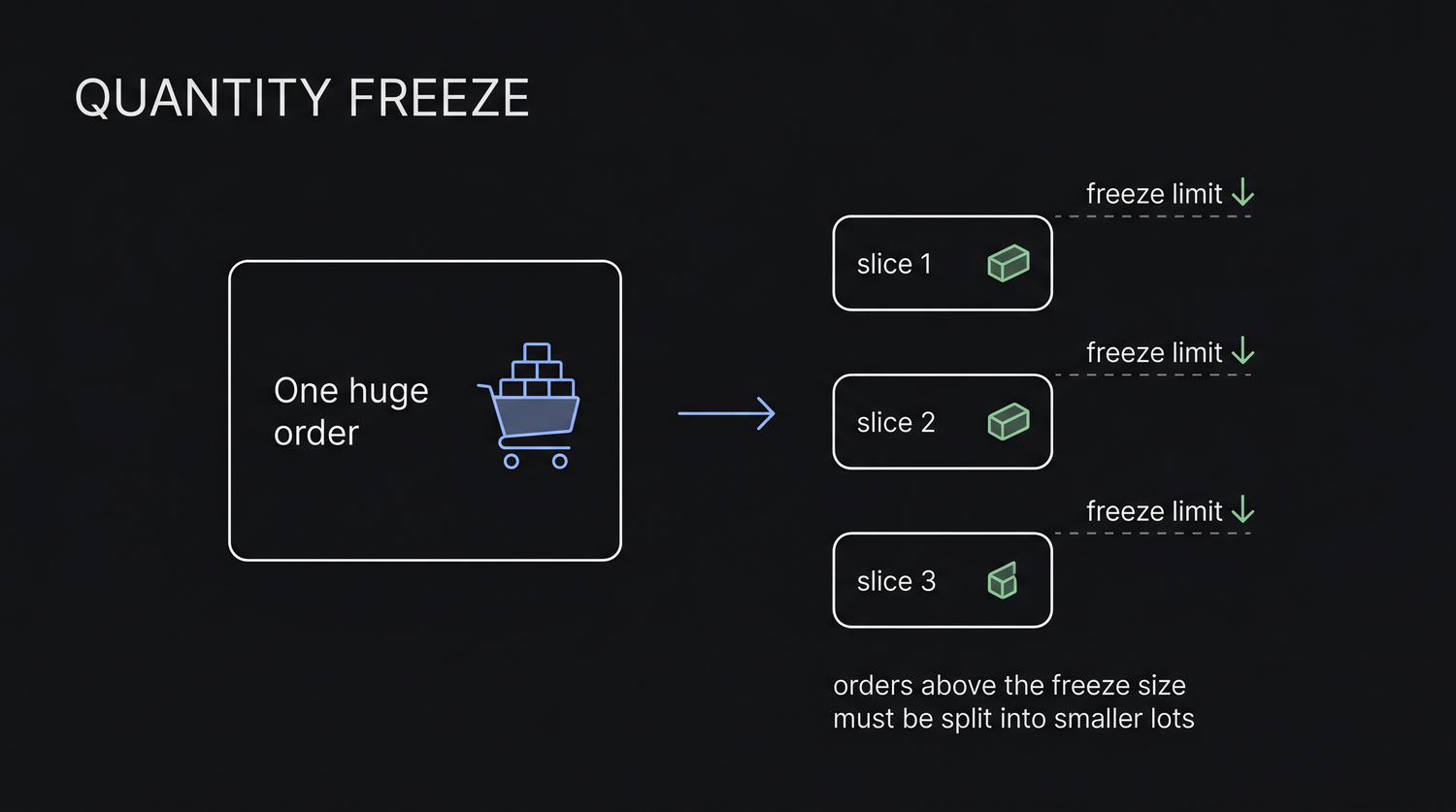

The last control is about the size of a single order, not your total position. Every contract has a quantity freeze limit, a maximum number of units the exchange will accept in one order. Send an order larger than that and it is simply rejected. To trade the same total size you must break it into several smaller orders, each below the freeze quantity.

Why bother? A single enormous order hitting the book can cause a sudden, violent move and can also be a fat-finger mistake, someone typing far more than they meant. The freeze acts as a speed bump. By forcing very large trades to be sliced into chunks, the exchange keeps one giant order from slamming the market in a single print and gives the order book a chance to absorb the size in pieces.

The freeze is expressed in the contract's own units. Recall that one RELIANCE future is a lot of 500 shares and one NIFTY future is a lot of 65. The freeze quantity is set well above a normal handful of lots, so an ordinary trader sending one or two lots of RELIANCE, or a few lots of NIFTY, never comes near it. It bites only on unusually large orders, where it quietly does its job of keeping execution orderly.

The quantity freeze is why large institutional orders arrive as a stream of smaller clips rather than one block. The exchange will not accept a single order above the limit, so big size is broken up by design, which is also part of why a deep, liquid contract can absorb large players without lurching.

The habit to carry away

These three controls share one purpose, keeping the market orderly and no single player too powerful, and for you they boil down to a short, practical routine.

Before you trade a single-stock future, check the F&O ban list. If the name is on it, you may only reduce or close, never open or add, so plan around that and do not assume you can build into it later. Keep in mind that a banned stock's future is a thin, closing-only market that can swing sharply, which is rarely where a beginner wants to be. When you size an order, keep it comfortably below the freeze quantity so it is accepted in one go, and split it if it is unusually large. And because the exact percentages and thresholds are fixed by the exchange and can change, verify the current figures against the NSE position-limits page rather than trusting a number you half-remember. Learn the structure once, check the specifics each time, and these rules become a quiet safety net rather than a surprise rejection.